Getting pre-approved for a VA loan gives you serious buying power in today’s competitive housing market. Veterans and active military members can secure financing with zero down payment and no private mortgage insurance.

We at Kearns Mortgage Team see how understanding how to get pre approved for a VA loan transforms the home buying experience. The process involves specific steps that differ from conventional loans.

Who Qualifies for VA Loan Pre-Approval

Military Service Standards That Matter

Veterans need at least 24 continuous months or the full period of at least 181 days during peacetime to qualify. Service members who served after August 2, 1990 must complete 24 months of active duty or 90 days under specific circumstances like hardship discharge.

National Guard and Reserve members qualify with 90 days of active duty for non-training purposes or six years in the Selected Reserve. The Department of Veterans Affairs requires a Certificate of Eligibility that proves your service record meets these standards.

You can obtain your COE online through the eBenefits portal, through your lender, or with Form 26-1880. This document becomes your gateway to zero down payment financing.

Credit Score Requirements Lenders Apply

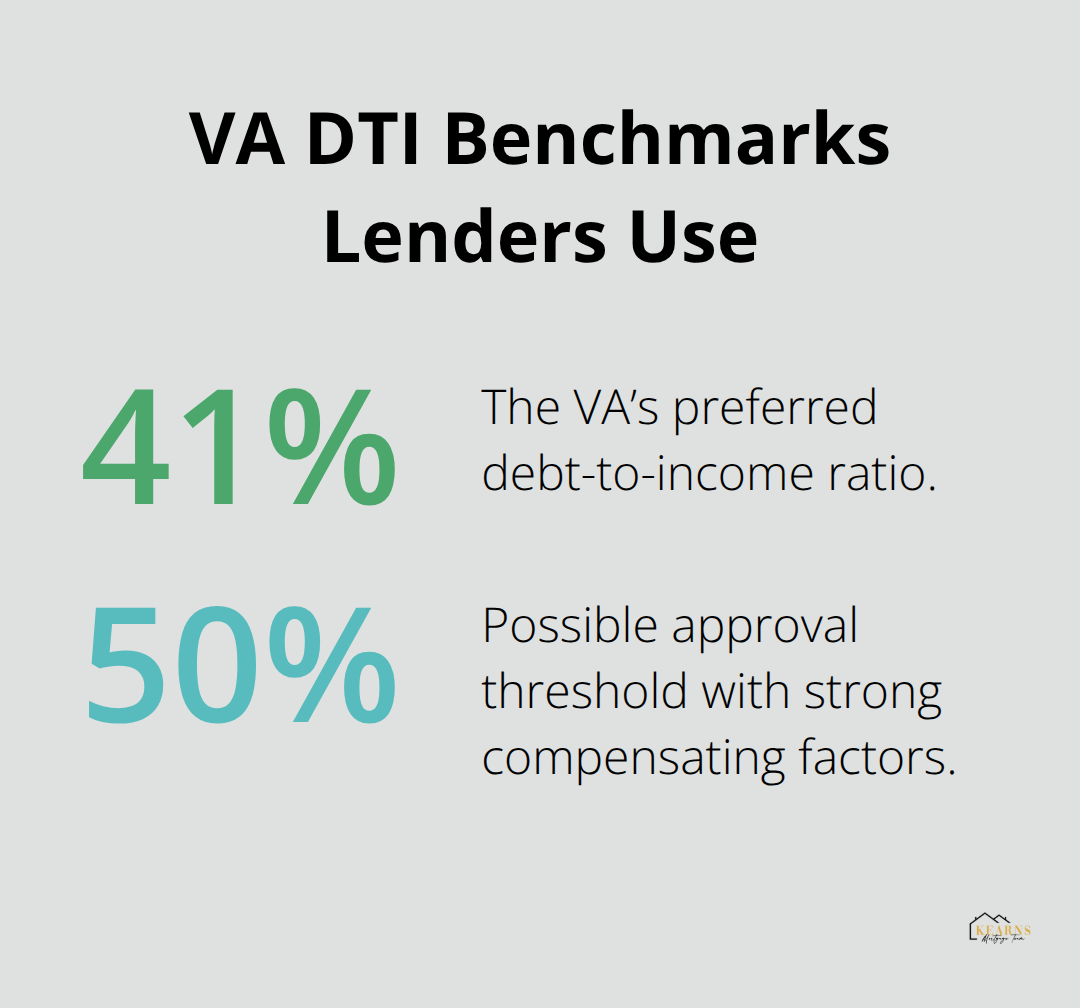

Most VA-approved lenders require a minimum 620 FICO score, though some accept scores as low as 580 with stronger compensating factors. The VA prefers debt-to-income ratios below 41%, but experienced lenders often approve borrowers up to 50% when other financial factors look strong.

Veterans with credit challenges can still qualify through programs like the Lighthouse Program, which has helped over 30,000 veterans improve their credit scores to secure loans.

Income Documentation Standards

Your income must be stable and verifiable through two years of W-2s, recent pay stubs, and tax returns. Self-employed borrowers need additional documentation including profit and loss statements and two years of tax returns.

Veterans who receive disability compensation should provide their award letters since this income often strengthens applications (and doesn’t count toward debt-to-income calculations in many cases).

Property and Occupancy Rules

The property must serve as your primary residence and meet VA minimum property requirements for safety and habitability. Properties in disrepair or investment purchases won’t qualify for VA financing.

The VA appraisal process checks both value and condition, which means fixer-uppers typically don’t pass inspection standards. Once you understand these qualification basics, the next step involves gathering your financial documents and choosing the right lender to guide you through the application process.

How Do You Navigate the VA Loan Pre-Approval Process

Start With Your Financial Paperwork

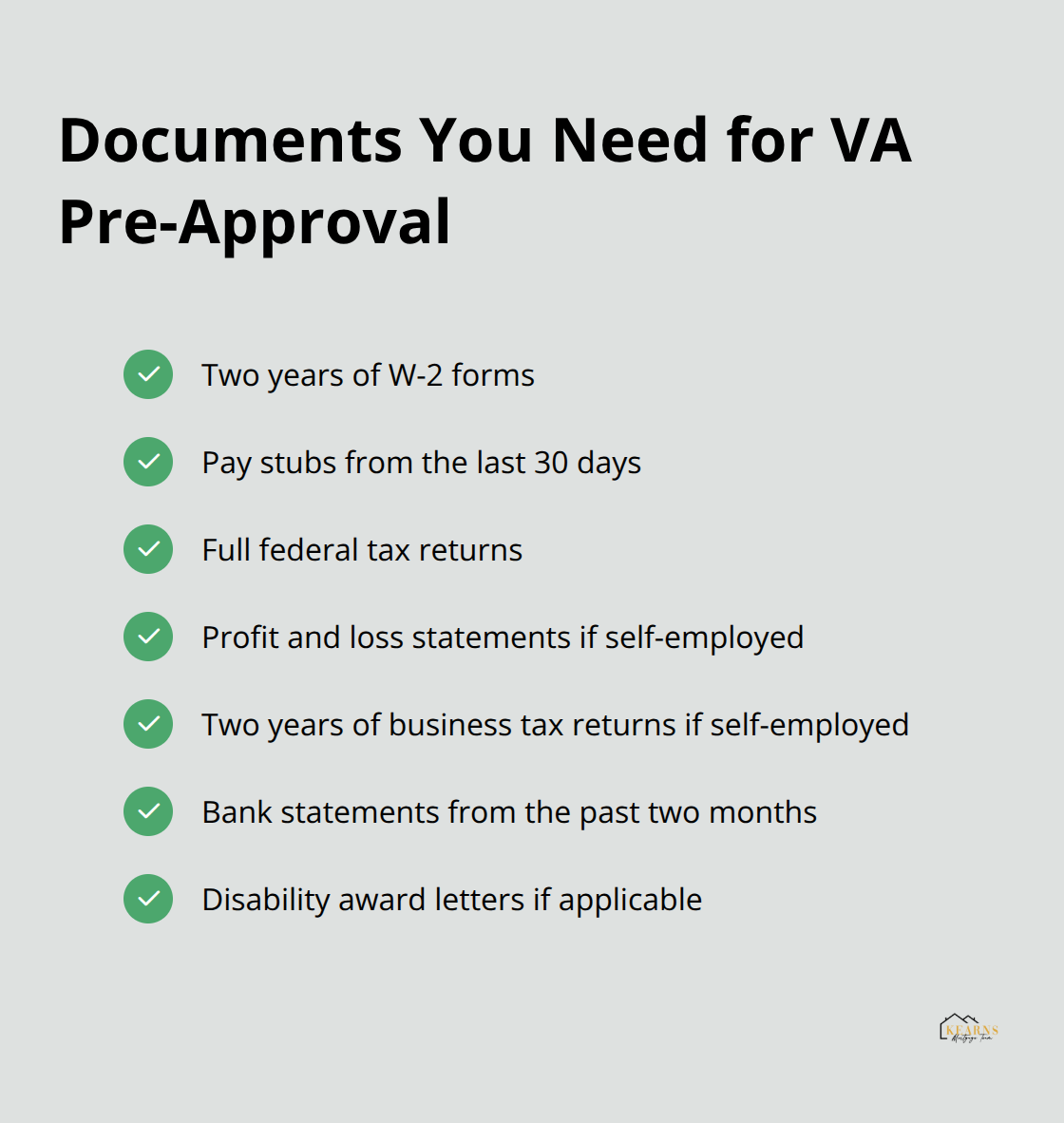

Collect your documents before you contact any lender. You need two years of W-2 forms, recent pay stubs from the last 30 days, and complete tax returns. Self-employed veterans must provide profit and loss statements plus business tax returns for two years. Bank statements from the past two months show your cash reserves and spending patterns.

Veterans who receive disability benefits should include their award letters since this income strengthens your application and often doesn’t count against debt ratios. The Consumer Financial Protection Bureau reports that borrowers with complete documentation close loans 15 days faster than those with missing paperwork.

Select Your Lender and Submit Your Application

Not all lenders handle VA loans equally well. Veterans United processed more VA loans than any other lender according to October 2024 Department of Veterans Affairs statistics, but smaller lenders often provide more personalized service. Compare at least three lenders and ask about their average processing times, funding fees, and origination charges.

Most lenders charge a 1% origination fee, though some waive this completely. Submit your application with your Certificate of Eligibility and complete financial package. The preapproval process takes 3-10 business days with responsive lenders.

Understand Your Pre-Approval Letter Details

Your pre-approval letter specifies your maximum loan amount, interest rate lock period (typically 30-60 days), and any conditions you must meet. The letter remains valid for 90 days, which gives you time to shop for homes confidently. Check the debt-to-income ratio calculation and verify all income sources appear correctly.

Some letters include contingencies like employment verification or additional asset documentation. This letter positions you as a serious buyer when you make offers, especially in competitive markets where sellers prefer pre-approved buyers. However, even with a strong pre-approval letter in hand, veterans often face specific challenges that can complicate the process.

What Obstacles Block VA Loan Pre-Approval

Credit Score Roadblocks Hit Veterans Hard

Veterans with credit scores below 620 face immediate rejection from most lenders, but this doesn’t end your homeownership dreams. The Veterans United Lighthouse Program provides personalized guidance to improve credit scores, helping veterans and their families achieve the dream of owning a home.

Pay down credit card balances below 30% utilization and dispute any errors on your credit reports through all three bureaus. Veterans with past bankruptcies must wait two years from discharge for Chapter 7 or one year for Chapter 13 with satisfactory payment history. Medical collections under $500 often get ignored by VA lenders, but larger medical debts need payment plans or settlements before approval.

Income Documentation Creates Major Delays

Self-employed veterans face the toughest income verification challenges because lenders need two years of complete tax returns plus current profit and loss statements. Veterans who recently transitioned to civilian employment often struggle with the two-year employment history requirement, but military income counts toward this timeline.

Disability compensation strengthens applications since this income typically doesn’t count against debt-to-income ratios (but you must provide current award letters). Commission-based workers need two years of tax returns that show consistent patterns. Lenders reject applications when veterans can’t produce complete W-2s or when recent job changes show income instability.

Property Appraisal Issues Cause Pre-Approval Reversals

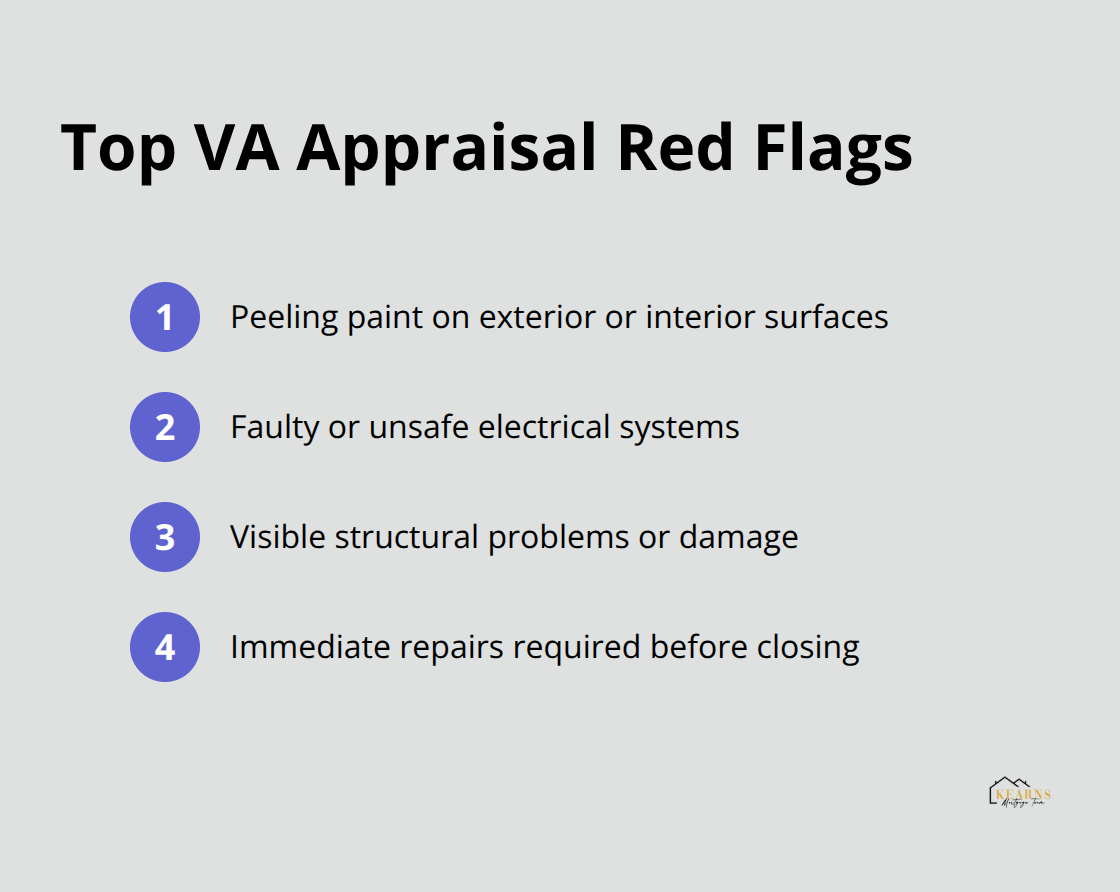

Property appraisal problems cause the most pre-approval reversals because VA appraisals determine the property’s value and make sure it meets basic livability standards. Properties with peeling paint, faulty electrical systems, or structural problems automatically fail VA inspections. The VA requires immediate repairs before closing, which sellers often refuse in competitive markets.

Veterans lose purchase contracts when appraisals come in below purchase prices because VA loans limit how much buyers can pay above appraised value. Properties that need significant repairs rarely pass VA inspection standards (making fixer-uppers poor choices for VA financing).

Final Thoughts

VA loan pre-approval positions you as a serious buyer with verified financial power. You access zero down payment options, no private mortgage insurance requirements, and competitive interest rates that conventional borrowers cannot match. Pre-approval letters give you confidence when you make offers and help sellers recognize your financial capability.

After you receive pre-approval, shop for homes within your approved price range and connect with real estate agents who have experience with VA transactions. Your pre-approval remains valid for 90 days, which provides adequate time to find the right property. Keep your financial situation stable during this period by avoiding new debt or major purchases that could affect your final loan approval.

Veterans who master how to get pre approved for a VA loan navigate complex documentation and lender requirements that can overwhelm even experienced borrowers. We at Kearns Mortgage Team guide veterans through every step of the VA loan process with personalized mortgage solutions. What specific aspect of your military service or financial situation do you think might present the biggest challenge in your VA loan pre-approval journey?