Your home holds significant value that you can tap into for major expenses, renovations, or debt consolidation. The home equity loan vs HELOC decision affects your monthly payments, interest costs, and financial flexibility for years to come.

We at Kearns Mortgage Team help homeowners navigate these two popular borrowing options daily. Both allow you to access your home’s equity, but they work very differently in practice.

How Do Home Equity Loans and HELOCs Actually Work?

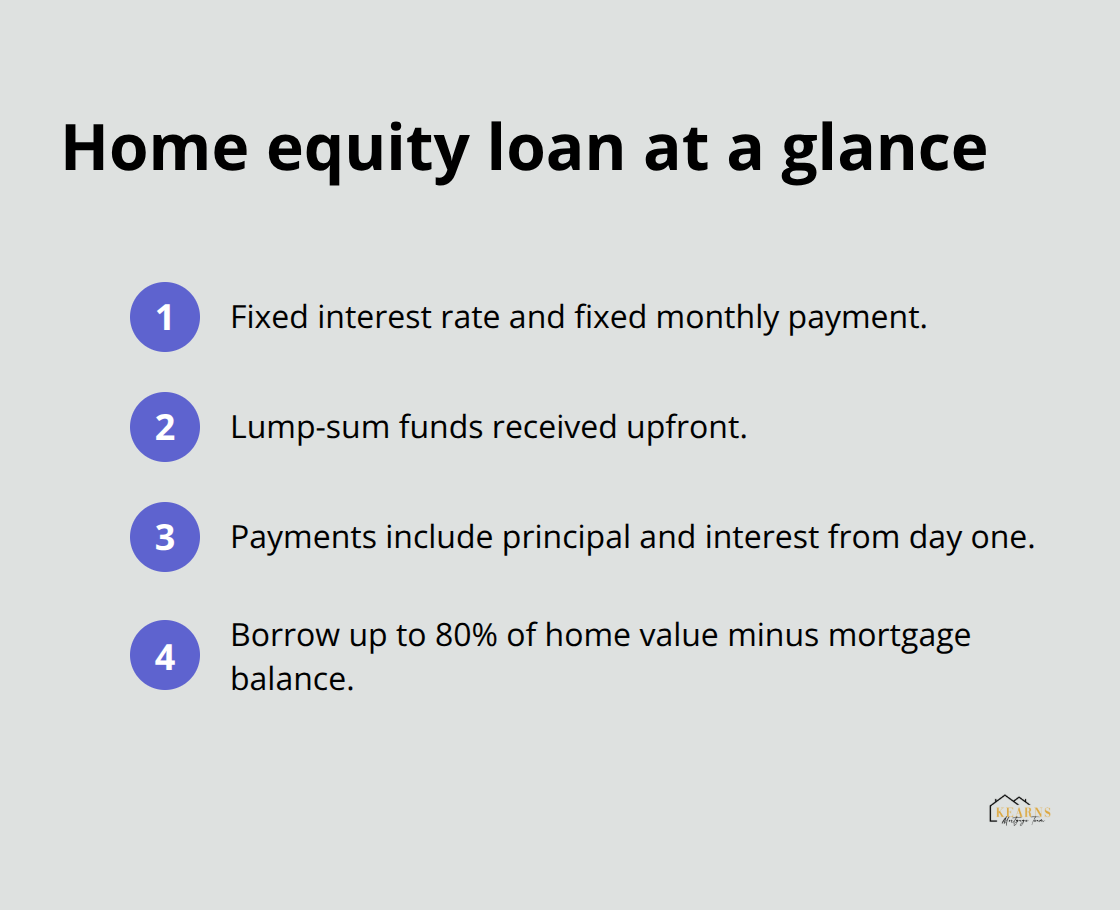

Home Equity Loans Deliver Fixed Payments

A home equity loan provides a lump sum payment against your home’s equity with a fixed interest rate. You receive the entire amount upfront and start monthly payments immediately that include both principal and interest. Current home equity loan rates average 8.01% for 15-year terms according to recent market data.

The payment stays the same throughout the loan term, which makes budget planning straightforward. Most lenders allow you to borrow up to 80% of your home’s value minus your existing mortgage balance. If your home is worth $400,000 and you owe $200,000, you could potentially access up to $120,000 through a home equity loan.

HELOCs Function Like Credit Cards Against Your Home

A HELOC operates as a revolving line of credit with variable interest rates. You receive approval for a credit limit but only pay interest on the amount you actually withdraw.

The draw period typically lasts 10 years, during which you can borrow, repay, and borrow again while you make interest-only payments. After the draw period ends, you enter a repayment phase that lasts up to 20 years where you pay both principal and interest.

Variable Rates Create Payment Uncertainty

The variable rate means your payments can increase or decrease based on Federal Reserve decisions. This flexibility makes HELOCs ideal for phased renovations or uncertain needs, but the payment changes require careful financial planning (especially when rates rise unexpectedly).

Both options require good credit scores (typically 640 or higher) and stable income for approval. The choice between fixed predictability and flexible access depends on your specific financial situation and project timeline.

What Will These Options Actually Cost You?

Interest Rate Reality Check

Home equity loans currently average 7.99% for 15-year terms according to Bankrate data, while HELOCs jump as the Fed delivers expected quarter-point cuts. Home equity loan rates have fallen to their lowest levels since 2023. The fixed rate advantage of home equity loans becomes clear when you consider payment predictability over time.

Your HELOC payment can spike dramatically when the Federal Reserve raises rates, potentially adding hundreds to your monthly payment. A $50,000 HELOC at current rates costs significant monthly interest-only payments, but jumps substantially if rates climb higher. Home equity loans protect you from this volatility with locked-in payments that never change.

Closing Costs Add Real Expense

Both options typically charge 2% to 5% in closing costs, including appraisal fees around $500, origination fees up to $1,000, and title insurance costs. HELOCs often include annual fees of $50 to $100 plus transaction fees for each withdrawal. A $75,000 loan could cost $2,250 in upfront fees.

Payment Structure Creates the Biggest Difference

The repayment structure creates the biggest cost difference between these options. Home equity loans start principal and interest payments immediately over 15 to 30 years. HELOCs allow interest-only payments during the draw period, then require full principal and interest payments that can double your monthly obligation.

Smart borrowers pay principal during the draw period to avoid payment shock later. Draw periods can be as short as three or five years, while the HELOC repayment period lasts up to 20 years. This strategy helps prevent the financial surprise that catches many homeowners off guard when their HELOC transitions from interest-only to full payments.

These cost considerations directly impact which option works best for different financial situations and project types.

Which Option Fits Your Financial Situation

Home Equity Loans Work Best for Defined Expenses

Home equity loans excel when you need a specific amount for a defined purpose with payment certainty. Major home renovations that cost $75,000, debt consolidation projects, or large one-time purchases benefit from the lump-sum structure and fixed payments. A predictable monthly payment of $698 on a $75,000 home equity loan at 7.99% over 15 years helps you budget accurately without rate increase worries.

HELOCs Excel for Flexible Needs

HELOCs shine when your needs are uncertain or spread over time. Kitchen renovations that happen in phases, emergency funds for unexpected expenses, or investment opportunities that arise unpredictably benefit from the draw-as-needed structure. The ability to borrow $20,000 initially, repay $10,000, then access that $10,000 again provides financial flexibility that home equity loans cannot match.

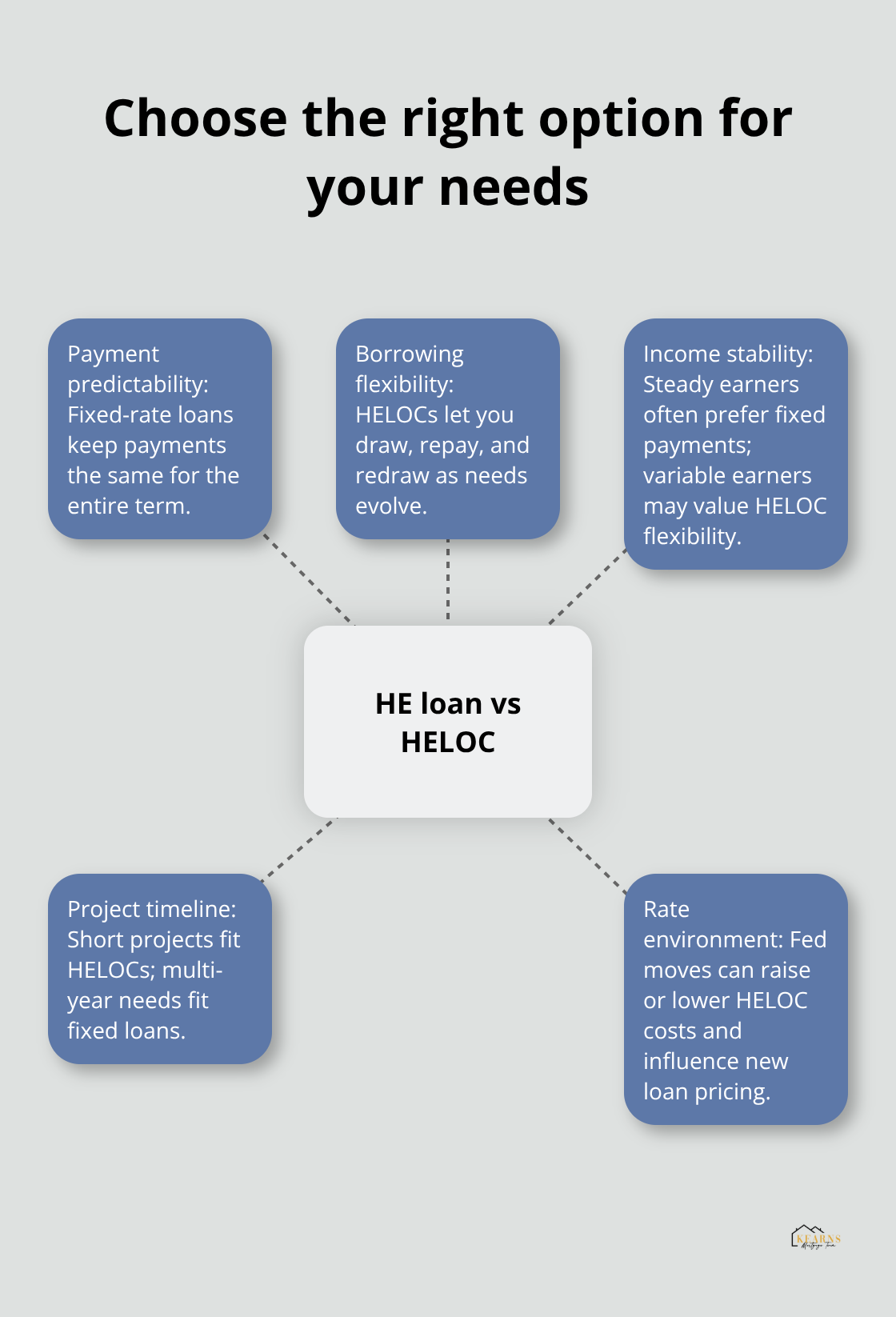

Income Stability Determines the Smart Choice

Borrowers with steady, predictable income should lean toward home equity loans to avoid payment volatility. Variable-income earners like commissioned salespeople or seasonal workers often prefer HELOCs because they can adjust borrowing based on cash flow. Federal Reserve’s interest rate decisions influence what you pay for variable-rate HELOCs and new home equity loans, creating opportunities when rates remain manageable.

Project Timeline Drives the Decision

Short-term projects under two years favor HELOCs because you pay interest only on funds actually used. Long-term needs that span several years work better with home equity loans because the fixed structure prevents payment increases that could strain your budget later.

With tappable equity hitting record highs of $11.5 trillion and three of five mortgage holders having at least $100,000 to borrow against, homeowners have substantial borrowing power, but the structure you choose affects your financial flexibility for decades. Consider exploring loan options that match your unique financial situation.

Final Thoughts

The home equity loan vs HELOC choice depends on your specific financial needs and comfort with payment changes. Home equity loans deliver fixed payments and lump-sum funds that work well for defined expenses like major renovations or debt consolidation. HELOCs provide flexible access to funds with variable rates that benefit homeowners with uncertain timing or phased projects.

Your income stability plays a major role in this decision. Steady earners should favor the predictability of home equity loans, while those with variable income often prefer HELOC flexibility. Project timeline matters too – short-term needs under two years work well with HELOCs, while longer commitments benefit from fixed-rate protection (especially when rates fluctuate).

Both options require good credit and stable income for approval. Consider your risk tolerance for payment changes, total borrowing needs, and repayment preferences when you make this choice. Ready to explore your home equity options? Kearns Mortgage Team can help you choose the right path for your situation.

What matters most to you – payment predictability or borrowing flexibility?