Real estate investors constantly search for strategies that maximize returns while building sustainable wealth. The BRRRR method real estate approach has emerged as one of the most effective ways to scale property portfolios quickly.

We at Kearns Mortgage Team see investors use this five-step process to transform single properties into multiple income streams. This strategy can help you build significant wealth when executed properly.

How Does the BRRRR Method Actually Work

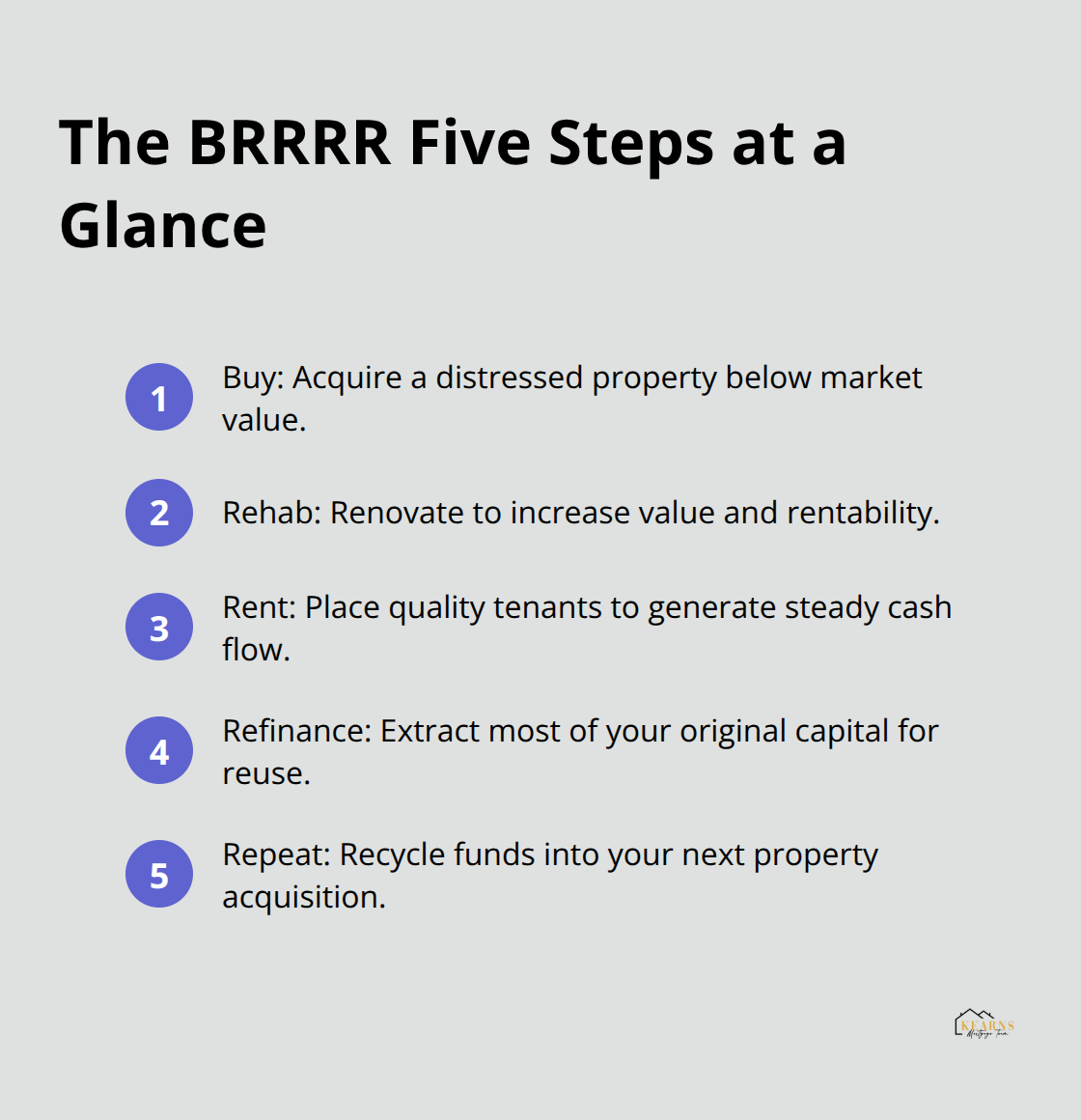

The Five-Step BRRRR Framework

BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. This systematic approach allows investors to recycle their capital repeatedly instead of tying it up in properties.

You purchase distressed properties below market value, typically at 70% or less of the after-repair value according to real estate investment standards. After you renovate these properties to increase their worth, you rent them out to generate monthly cash flow. The refinance step extracts most or all of your original investment capital, which you then use to purchase the next property.

Why BRRRR Beats Traditional Buy-and-Hold

Traditional real estate investment requires substantial capital for each property purchase, which limits portfolio growth. With rental demand continuing to rise across most markets, the BRRRR strategy proves particularly effective now. Smart investors who use this method can acquire multiple properties within 12-18 months instead of waiting years to save for each down payment. The key advantage lies in how you leverage other people’s money through refinance while you maintain ownership and cash flow from each property.

Who Should Use This Investment Strategy

BRRRR works best for investors with access to initial capital of $50,000 to $100,000 and strong credit scores above 680. You need experience to manage contractors and understand renovation costs, as budget overruns can destroy profitability. This strategy suits investors comfortable with active property management and those who can handle multiple moving parts simultaneously. New investors should avoid BRRRR until they understand local rental markets and have completed at least two traditional real estate transactions.

Common Requirements for Success

The method demands time, energy, and risk tolerance that passive investors typically lack. You must maintain contingency budgets (about 20% for unexpected expenses) to accommodate unforeseen issues during rehabilitation. Most successful BRRRR investors also build networks of reliable contractors, real estate agents, and lenders who understand investment properties. Market conditions significantly impact this strategy, so you need to operate in favorable environments with strong rental demand and property appreciation potential.

Now that you understand how BRRRR works and who can benefit from it, let’s examine each step in detail to help you implement this strategy successfully.

How Do You Execute Each BRRRR Step Successfully

Find and Purchase Below-Market Properties

The foundation of profitable BRRRR investment starts with property acquisition at 70% or less of after-repair value. Successful investors focus on distressed properties through foreclosure auctions, wholesalers, and direct mail campaigns to motivated sellers. Hard money lenders typically provide 90% of the purchase price and 100% of construction costs, which allows you to close within 7-14 days compared to 30-45 days with conventional loans. Cash purchases give you the strongest position when you negotiate, especially when you compete against other investors in hot markets.

Execute Strategic Renovation and Value Creation

Smart renovations target high-impact improvements that tenants value most: updated kitchens, refinished hardwood floors, and modern bathrooms typically provide the best return on investment. Budget 20% above your initial renovation estimate for unexpected issues like plumbing problems or electrical upgrades that inspections might miss (these surprises happen more often than investors expect). Focus on functional improvements over luxury finishes since rental properties need durability more than high-end aesthetics. Complete renovations within 60-90 days to minimize costs and start rental income generation quickly.

Maximize Cash Flow Through Strategic Rental Management

Set rental rates 5-10% below market value to attract quality tenants quickly and reduce vacancy periods that eat into profits. Screen tenants thoroughly with credit checks, employment verification, and previous landlord references since good tenants protect your investment better than slightly higher rents. Long-term leases provide more stability than month-to-month arrangements, and first month’s rent plus security deposit requirements help filter out financially unstable applicants.

Properties must generate positive cash flow based on proper cash flow analysis to maintain sustainability through market fluctuations (this calculation acts as your safety margin).

The refinance step transforms your improved property into fresh capital for your next investment opportunity.

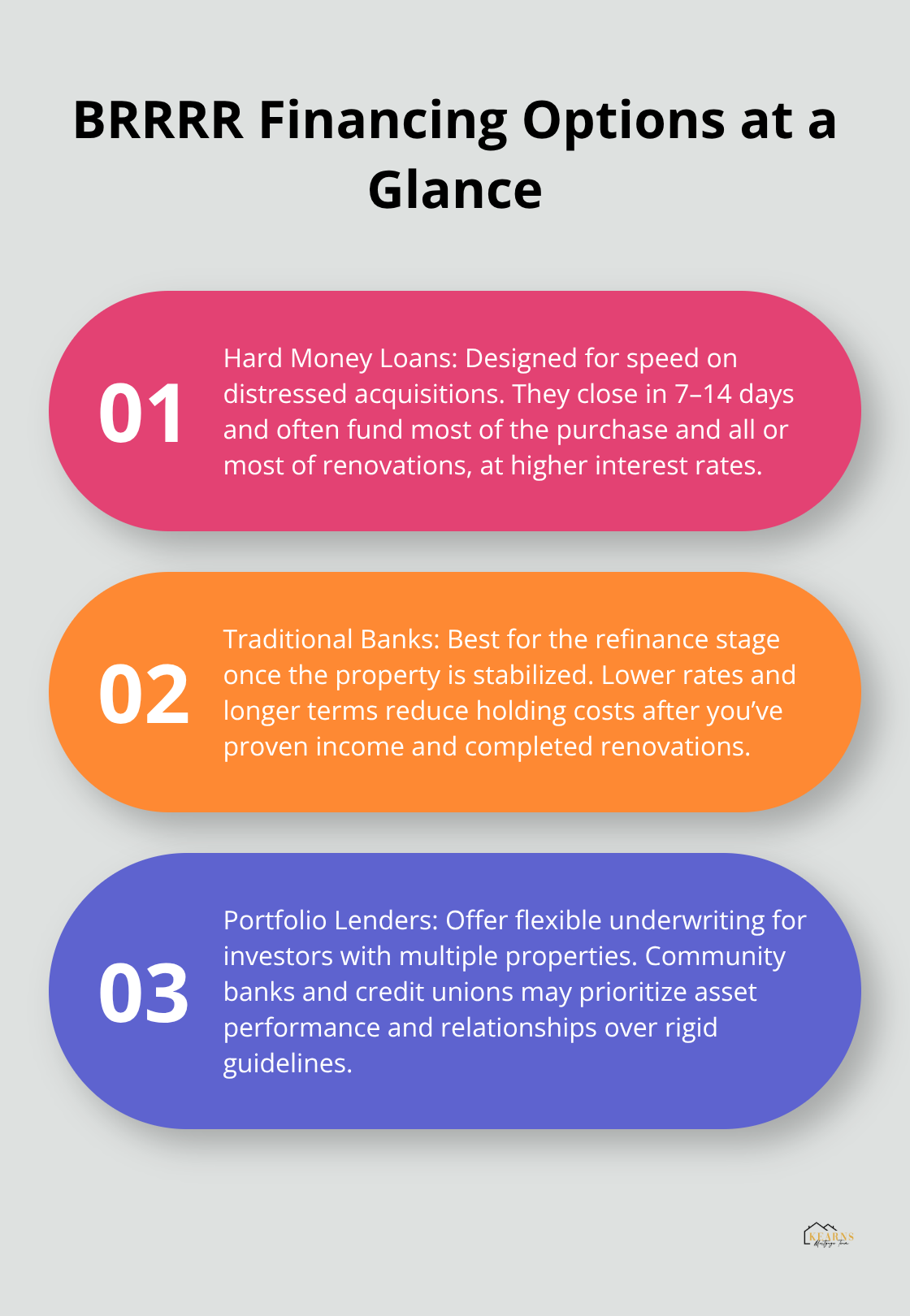

Which Financing Option Works Best for BRRRR Investors

Hard Money Loans Provide Speed Over Cost

Hard money loans dominate the BRRRR acquisition phase because speed beats cost when you compete for distressed properties. These loans close within 7-14 days at interest rates between 10-15% annually, compared to conventional loans that take 30-45 days at 6-8% rates. Hard money lenders typically fund 90% of purchase price and 100% of renovation costs, which means you can control a $200,000 property with just $20,000 down. Private money lenders often provide even better terms at 8-12% interest when you build relationships with local investors who have cash to deploy.

Traditional Banks Excel at Refinance Stage

Traditional bank financing works for the refinance step but fails during acquisition when sellers demand quick closings and cash-equivalent offers. Banks offer lower interest rates and longer terms once you complete renovations and establish rental income. Most conventional lenders require seasoned investment properties and proven cash flow before they approve refinance applications.

The lower rates from traditional banks (typically 2-4% below hard money rates) make them ideal for long-term holds after you extract your initial capital.

Cash-Out Refinance Requirements You Must Meet

Most banks require 6-12 months of seasoning before you can refinance based on improved property value, though some portfolio lenders waive this requirement for experienced investors. Your debt-to-income ratio must stay below 45% across all properties, and each property needs positive cash flow of at least $200 monthly after all expenses. Appraisers focus heavily on comparable sales within one mile and six months, so you need strong neighborhood comps to support your after-repair value claims. Banks typically allow 75-80% loan-to-value on investment property refinances (which means your total investment should not exceed 60% of final property value to extract most capital).

Portfolio Lenders Offer Maximum Flexibility

Portfolio lenders who keep loans on their books offer more flexibility than banks that sell mortgages to government agencies like Fannie Mae or Freddie Mac. Credit unions and community banks often provide better terms for local investors with multiple properties, especially when you maintain business accounts and build personal relationships with loan officers. Asset-based lenders evaluate deals primarily on property cash flow and value rather than personal income, which helps investors who own multiple properties but show limited W-2 income. Interview at least three different lenders before you start your first BRRRR project to understand their specific requirements, interest rates, and timeline expectations since each lender structures deals differently.

Final Thoughts

The BRRRR method real estate strategy creates sustainable wealth when investors recycle capital across multiple properties instead of limiting themselves to one investment at a time. Investors who execute this approach correctly build portfolios worth millions within five to seven years while they generate substantial monthly cash flow. The compound effect occurs when each refinanced property funds the next acquisition, which creates exponential growth that traditional buy-and-hold strategies cannot match.

Most investors fail because they underestimate renovation costs, skip proper market research, or choose properties in declining neighborhoods. Others rush the refinance step before they establish adequate rental history or attempt BRRRR in markets with weak rental demand. The biggest mistake involves the use of personal credit cards or high-interest loans for renovations instead of proper hard money financing (which destroys profit margins quickly).

This strategy works best for investors with strong credit, adequate capital reserves, and time to manage active investments. We at Kearns Mortgage Team help investors secure the financing they need for successful BRRRR implementation. What specific market conditions in your area would make the BRRRR method most profitable for your investment timeline?