Your credit score is one of the biggest factors lenders examine when you apply for a mortgage. At Kearns Mortgage Team, we help borrowers understand what credit score is needed to buy a house and how to position themselves for approval.

The difference between a good score and a poor one can mean thousands of dollars in interest over the life of your loan. This guide breaks down the credit score requirements across different loan types and shows you exactly how to strengthen your financial profile.

What Score Do You Actually Need?

Credit scores range from 300 to 850, and lenders have carved out distinct categories that directly affect your mortgage eligibility. A score of 620 to 669 falls into the fair range and opens the door to some loan types, though typically with higher interest rates and stricter conditions. Good credit sits between 670 and 739, where conventional lenders work with you more readily and rates improve noticeably. Very good credit, from 740 to 799, is where most lenders offer their most competitive terms. Exceptional credit above 800 signals financial discipline, though it doesn’t significantly improve your rate anymore. The real threshold that matters for mortgage shopping is 700. At this score, according to Curinos data from January 2025, a 30-year conventional loan averaged 7.42 percent. Drop to 620, and that same loan climbs to 7.89 percent. Jump to 760, and you’re looking at roughly 7.15 percent. On a 350,000-dollar mortgage, that difference between 620 and 760 amounts to about 156 dollars monthly, or nearly 56,000 dollars over 30 years.

The Numbers Behind Each Bracket

Lenders don’t view all fair-credit borrowers the same way. A 640 score gets you 7.72 percent, while 680 earns 7.55 percent, and 700 lands you 7.42 percent. These aren’t arbitrary jumps-they reflect how risk models price the likelihood of default. At 740, you hit 7.26 percent, and the curve starts flattening. This means pushing from 700 to 740 saves you more money than pushing from 740 to 800. If you’re sitting at 680 and can improve to 700 before applying, that ten-point bump could lower your monthly payment by roughly 20 dollars. That’s worth the effort. Fannie Mae eliminated minimum credit score requirements for conforming conventional loans as of November 2025, shifting focus to overall credit risk and ability to repay. However, most lenders still internally require around 620 for conventional loans, and 660 or higher for better terms.

How Down Payment and Reserves Change the Game

Your credit score doesn’t operate in isolation. Lenders also weigh your down payment size and savings reserves against your score. A larger down payment compensates for a weaker score because it reduces the lender’s risk. If you’re at 600 with 25 percent down, some lenders will work with you; at 600 with 3 percent down, you’ll hit a wall. Reserves-the liquid savings you have after closing-matter too. If you have six months of mortgage payments saved, lenders view you as more stable even with a fair credit score. This is why an FHA loan with 3.5 percent down works at 580, while a conventional loan at the same score demands 10 percent down or more. The combination of score, down payment, and reserves tells the real story of your creditworthiness.

The Role of Debt-to-Income Ratio

Your DTI, or debt-to-income ratio, influences approval odds significantly. Lenders typically prefer housing costs around 28 percent of gross income and total debt payments under 36 percent. A higher score gives you more flexibility here, but a lower score with excellent DTI can still work. This means you might qualify even with fair credit if your income covers your debts comfortably. Understanding how lenders evaluate these factors together-not just your score alone-helps you position yourself for approval. With this foundation in place, the next step is to see how different loan types actually use credit scores to determine who qualifies and what rates they offer.

Credit Score Requirements by Loan Type

Conventional Loans: The Higher-Score Path

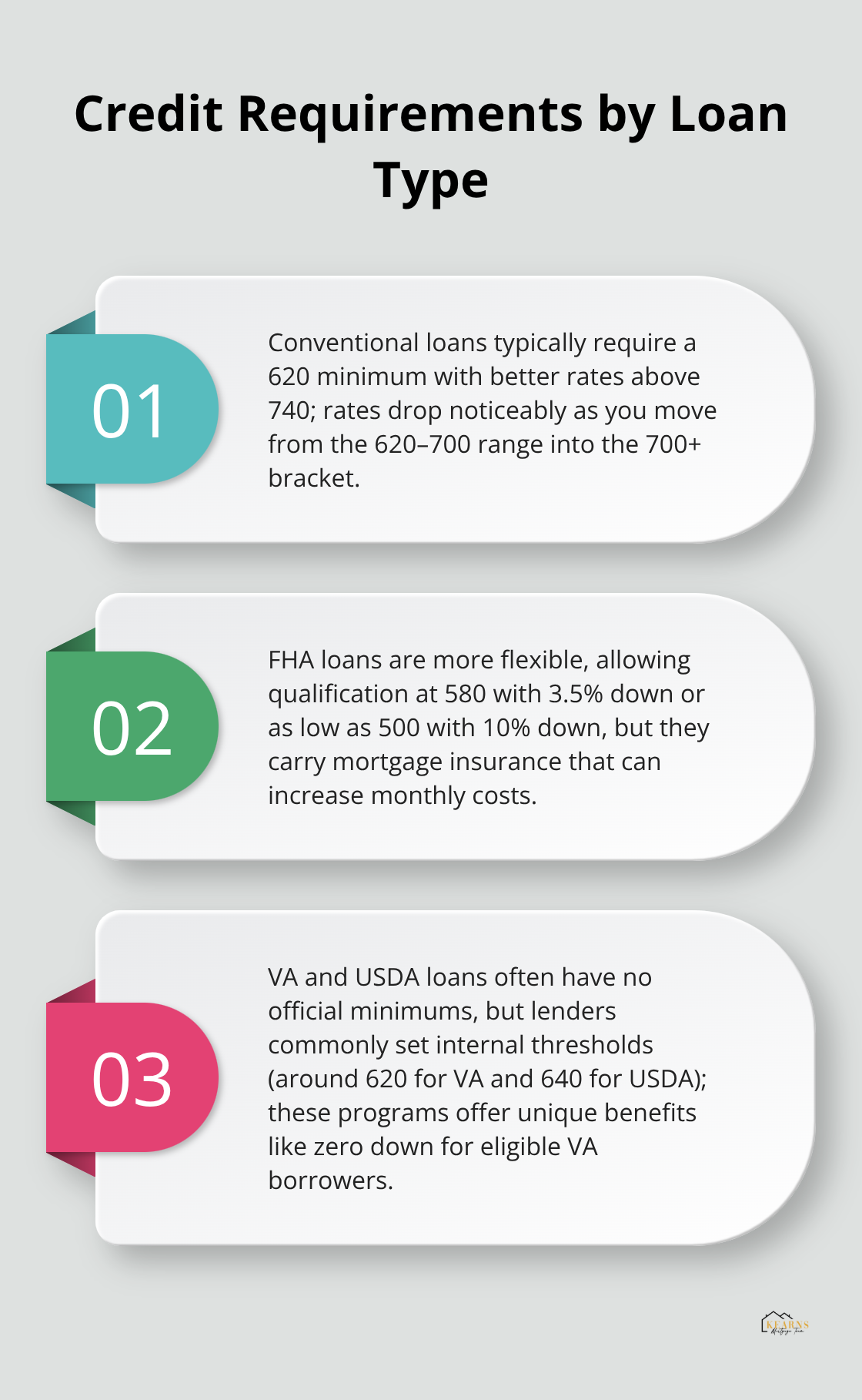

Conventional loans sit at the stricter end of the spectrum. Most lenders internally require a 620 minimum, though Fannie Mae eliminated the official floor in November 2025, shifting focus to overall credit risk assessment. The reality is that 620 gets you in the door, but your rate suffers. At 620, you pay 7.89 percent on a 30-year fixed loan according to Curinos data. Jump to 660, and you drop to 7.72 percent. The sweet spot for conventional loans sits at 740 and above, where rates hover around 7.26 percent or lower.

Shopping conventional means pushing higher than the minimum because the monthly savings compound quickly. A 10-point improvement from 680 to 690 cuts roughly 10 to 15 dollars monthly on a 350,000-dollar loan. Over 30 years, that totals 3,600 to 5,400 dollars in your pocket.

FHA Loans: Credit Flexibility for Lower Scores

FHA loans open homeownership to borrowers conventional lenders reject outright. You can qualify with a 580 score and put down just 3.5 percent, or go as low as 500 with 10 percent down according to HUD guidelines. This flexibility makes FHA attractive when your credit needs work.

However, FHA comes with mortgage insurance premiums that stick around longer than conventional PMI, so the monthly payment can still be substantial. The trade-off between easier qualification and higher ongoing costs matters when you calculate your true affordability.

VA and USDA Loans: Specialized Programs

VA loans typically have no published minimum score, but most lenders set their own threshold around 620 depending on your down payment and other factors. USDA loans follow a similar pattern-no official USDA minimum, but participating lenders commonly require 640 or higher. The key difference is that VA loans often require zero down payment and USDA loans serve rural borrowers with income limits, making them powerful tools if you qualify.

Non-QM Loans: Income Over Credit Score

Non-QM loans exist for self-employed borrowers and those with non-traditional income, and credit score requirements vary widely by loan type. Your score matters less here than your ability to document income through bank statements or tax returns. This loan type shifts the focus away from credit history and toward your actual financial capacity to repay.

The best loan choice depends on your specific financial picture, not just your credit score. Understanding which loan type aligns with your situation helps you move forward with confidence toward the next critical step: strengthening your credit profile before you apply.

Strengthen Your Credit Before You Apply

Check your credit report at AnnualCreditReport.com to access free reports from Experian, Equifax, and TransUnion. Many borrowers discover errors on their reports that unnecessarily drag down their scores. Dispute any inaccuracies immediately because lenders pull tri-merge reports and may use the middle score or the lower score if you have a co-borrower. A single reporting mistake can cost you hundreds of dollars monthly.

Focus on Credit Utilization

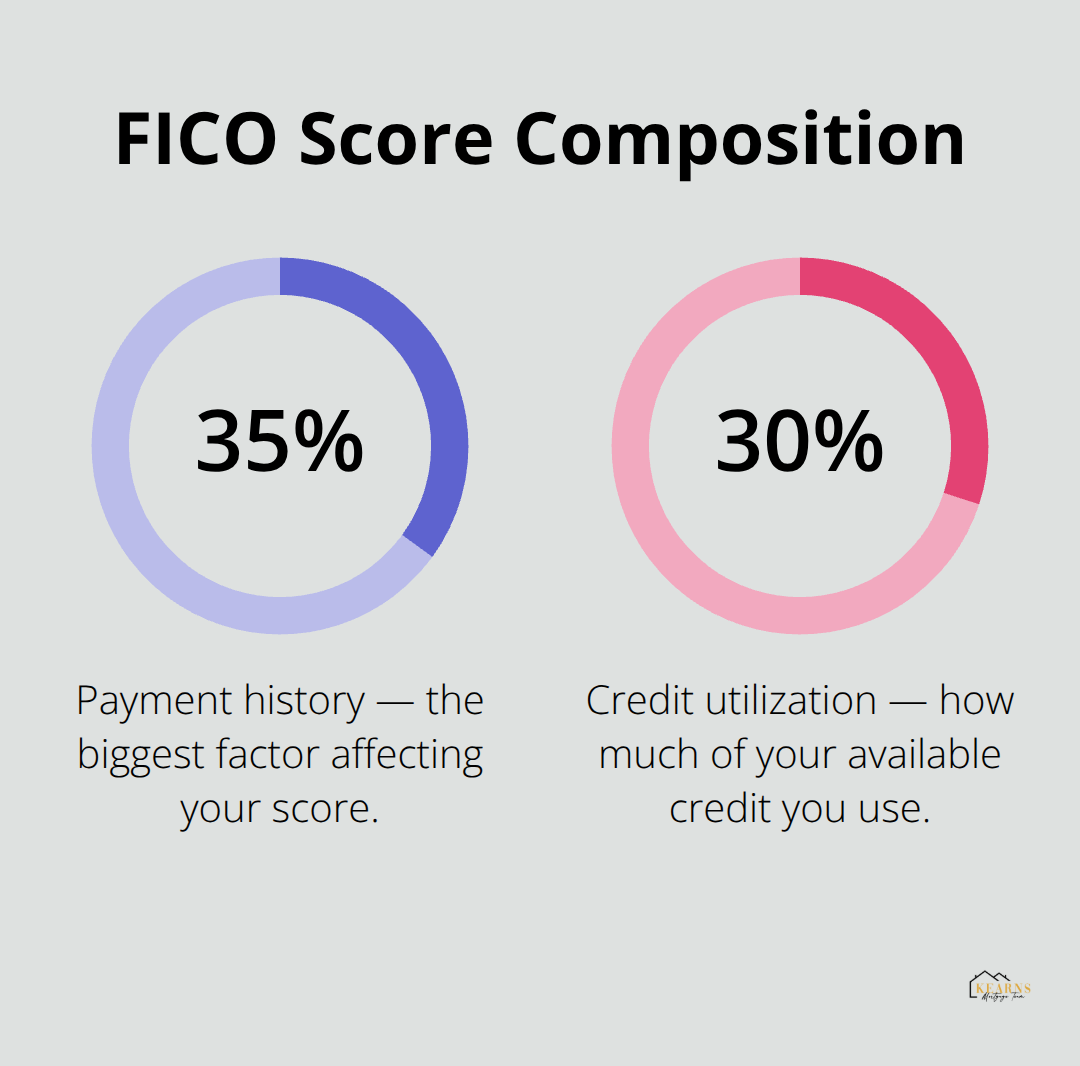

Credit utilization accounts for 30 percent of your score according to FICO methodology. If you carry balances on multiple credit cards, pay them down aggressively. Try to keep total utilization under 30 percent of your available limits. A borrower with $10,000 in available credit should carry no more than $3,000 in balances across all cards. This single move often produces a score boost within 30 to 45 days because utilization updates monthly on your credit report.

Do not close old accounts after paying them down. Closing cards reduces your available credit and shrinks your credit history length, both of which hurt your score. Instead, keep accounts open and unused to maximize available credit.

Establish Perfect Payment History

Payment history makes up 35 percent of your score, making it the most critical factor. Set up automatic payments for all debts so you never miss a due date. A single 30-day late payment can drop your score 100 points or more, and late payments remain on your report for seven years. If you have accounts that are currently late, bring them current immediately before applying for a mortgage. After that, maintain perfect payment history for at least three to six months leading up to your application.

Avoid New Credit Applications

Avoid opening new credit accounts or applying for new loans in the months before you apply for a mortgage because new inquiries and new accounts lower your score and increase your debt-to-income ratio. When you shop for mortgage rates, submit applications within a 15 to 45-day window so multiple inquiries count as a single inquiry.

Plan Your Timeline Realistically

Consider the timeline realistically when targeting a score improvement. If your score is 660 and you want to reach 700, plan for two to four months of disciplined debt paydown and perfect payments. A 40-point improvement is achievable but requires focus. If you’re starting at 620, the work takes longer, but the payoff justifies the delay. Waiting six months to apply with a 680 score beats rushing to apply at 640 and paying 7.89 percent instead of 7.55 percent on your loan (the difference amounts to roughly $30 monthly on a $350,000 mortgage).

Final Thoughts

Your credit score matters, but it’s only one piece of the puzzle when determining what credit score is needed to buy a house. We at Kearns Mortgage Team have worked with borrowers across the entire credit spectrum, and the right strategy depends on your unique situation. A 620 score opens doors to conventional loans, while 580 qualifies you for FHA programs-the real question is whether you’re positioned to get the best possible terms for your financial goals.

Start by pulling your credit reports from AnnualCreditReport.com and fix any errors immediately. Focus on the two actions that move the needle fastest: pay down credit card balances to lower your utilization and set up automatic payments to protect your payment history. If you’re currently at 660 and can reach 700 before applying, that effort saves you thousands over your loan term.

The mortgage landscape has shifted, and lenders now evaluate your full financial picture instead of fixating on a single number (Fannie Mae eliminated minimum credit score requirements, and loan programs exist for nearly every situation). Connect with Kearns Mortgage Team to understand exactly what you qualify for today and what steps strengthen your position tomorrow. What’s holding you back from taking the first step toward homeownership-your credit score, your down payment savings, or uncertainty about which loan type fits your life?