Your credit score is one of the biggest factors lenders examine when you apply for a mortgage. The minimum credit score for a mortgage varies depending on the loan type you choose, and understanding these requirements can save you time and money.

At Kearns Mortgage Team, we help borrowers navigate these requirements every day. Whether you’re starting your homeownership journey or refinancing, knowing where you stand financially makes all the difference.

What Credit Score Do You Actually Need?

Conventional loans used to demand a 620 minimum, but as of November 2025, Fannie Mae and Freddie Mac eliminated that baseline requirement entirely. This shift means lenders now set their own floors, and those floors vary dramatically. Some lenders work with scores in the high 600s, while others won’t touch anything below 680. Without a universal minimum, your actual qualification depends on what each individual lender decides. Shopping around isn’t optional anymore-it’s essential. A score of 650 might get rejected at one lender and approved at another.

FHA Loans Open Doors at Lower Scores

FHA loans offer flexibility that conventional mortgages cannot match. You can qualify with a 500 credit score if you put 10% down, or with a 580 score if you make a 3.5% down payment. However, many lenders add overlays on top of FHA guidelines, meaning they require 580 or 640 even when the program technically allows lower scores. This gap between official minimums and what lenders actually demand frustrates borrowers constantly. A real example from Homebuyer.com showed a borrower with a 610 score who faced denial by a credit union with a 640 overlay, then received approval from another lender following actual FHA rules. The lesson is clear: don’t assume you’re ineligible just because one lender says no.

VA and USDA Loans Have No Official Minimums

VA loans carry no federally mandated minimum credit score whatsoever, yet most lenders still require around 620 anyway. USDA loans similarly have no official floor, though lenders typically prefer 640 or higher for streamlined processing. Veterans and rural borrowers often possess more negotiating power than they realize, but only if they shop multiple lenders. One lender’s 620 requirement might be another’s 580 or even lower. The federal guidelines leave room, but individual lender overlays consume that room fast. Your job involves testing your eligibility across several lenders rather than accepting the first answer you receive.

Lender Overlays Change Everything

Overlays represent extra qualification standards that lenders add on top of official mortgage guidelines, effectively raising the minimum requirements to qualify. These overlays vary significantly by lender, which means the same loan application can face denial at one institution and approval at another. Credit score overlays rank among the most common and impactful; they frequently determine whether a borrower qualifies. DTI overlays restrict debt-to-income ratio more than the program allows, while job history overlays require continuous employment at some lenders but permit gaps at others. Collections overlays also differ-some lenders ignore small collections, while others require payoff before approval.

Understanding that overlays exist and vary by lender transforms how you approach your mortgage search. Instead of viewing one rejection as final, you recognize it as that particular lender’s risk tolerance, not your actual eligibility.

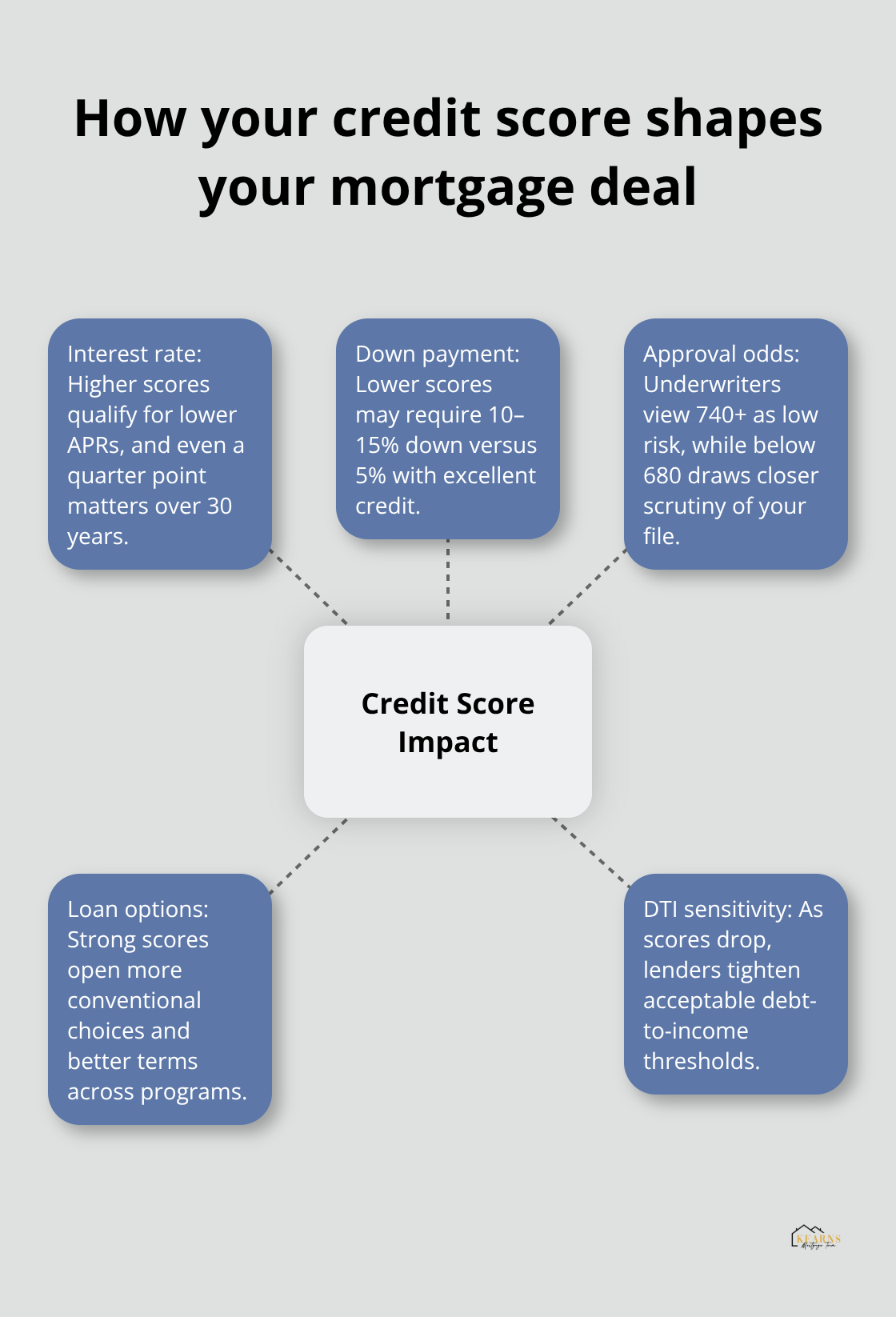

How Your Credit Score Shapes Your Mortgage Deal

Your credit score doesn’t just determine whether you qualify for a mortgage. It directly controls the interest rate you pay, the down payment you need, and your odds of approval. These three factors compound over time, turning a 50-point difference in your score into tens of thousands of dollars in lifetime costs. Understanding exactly how lenders use your score to price your loan gives you leverage to improve your situation before you apply.

The Real Cost of Lower Credit Scores

Interest rates vary significantly based on credit score ranges. According to data from December 2025, a borrower with a 760-850 score on a $300,000 30-year mortgage faced an APR around 7.242%, while someone with a 660-679 score paid 7.609%. That 0.367% difference translates to meaningful monthly savings for higher-scoring borrowers. Move to a $350,000 loan and the spread widens further. A 700 credit score carried a 7.449% rate, while a lower score pushed payments higher, adding significant annual costs. These numbers show real market rates, not theoretical ones. The practical takeaway is ruthless: every 20 to 40 points in your score range costs you $1,000 to $3,000 annually in extra interest. You cannot afford to ignore your score before you apply.

Down Payments Shift With Your Score

Lenders use your credit score to determine how much skin you must have in the game. A borrower with excellent credit puts 5% down on a conventional loan, while someone with a 620 score might need 10-15% or faces denial altogether. This directly impacts your purchasing power and closing timeline. The median credit score for new mortgage borrowers in recent quarters reflects strong approval standards, meaning half of approved borrowers scored above typical thresholds. That statistic should concern you if your score sits below 700. You fight upstream against the typical borrower profile that lenders have grown comfortable with.

Loan Options Expand at Higher Scores

Higher credit scores also expand your loan options significantly. FHA loans theoretically accept 580 scores with 3.5% down, but many lenders layer on 640 overlays, effectively eliminating that flexibility. A conventional borrower with a 750 score faces zero such restrictions. The approval odds shift dramatically too. Lenders treat 740-plus scores as low-risk, 700-739 as acceptable, 680-699 as marginal, and anything below 680 as requiring serious scrutiny of your other financials.

Your Debt-to-Income Ratio Matters More When Your Score Drops

Your debt-to-income ratio becomes far more important when your score falls below 700. Try to keep that ratio below 36%, though lenders may accept higher DTIs with larger down payments if your score compensates. Below 680, you fight on multiple fronts simultaneously. Your income stability, employment history, and cash reserves all receive heightened attention. Lenders want proof that you can handle the mortgage payment even if your credit history suggests past struggles. This is where your actual financial behavior-not just your score-determines approval. The next section explores how you can strengthen your credit profile and position yourself for the best possible terms.

Boost Your Score Before You Apply

Payment History: Your Strongest Lever

Payment history accounts for 35% of your credit score, making on-time payments your most powerful tool for improvement. Late payments linger on your report for up to seven years, but their impact weakens after two years if you maintain perfect payment behavior afterward. If you have missed payments, start now with every bill due going forward. Set up automatic payments for at least the minimum amount on every account, then pay extra toward high-balance cards. This single habit compounds faster than any other credit-building strategy.

Credit Utilization and Account Management

Attack your credit utilization immediately. Try to keep balances at 30% or less of your total credit limits across all cards. If you carry a $5,000 limit on a card and owe $3,000, you sit at 60% utilization, which damages your score substantially. Pay that balance down to $1,500 and watch your score jump within 30 to 45 days as the bureaus update your information. Do not close old credit cards after paying them off, since closing accounts raises your overall utilization ratio and reduces the average age of your credit history, both negative moves.

Instead, keep those accounts open and use them occasionally for small purchases you pay off immediately.

Hard Inquiries and Credit Report Errors

Hard inquiries from new credit applications ding your score, so avoid opening new accounts in the six months before you apply for a mortgage. If you must rate-shop for a mortgage, complete all inquiries within a 30-day window; the credit bureaus treat multiple mortgage inquiries as a single search when they occur close together. Check your credit reports from Experian, Equifax, and TransUnion for free at AnnualCreditReport.com and dispute any errors you find immediately. Errors happen frequently and can artificially suppress your score by 50 to 100 points.

Collections Accounts Require Strategic Action

Collections accounts require strategy. Paying off a collection may help your score under newer FICO models, but it can sometimes hurt under older models that mortgage lenders still use. Contact the collection agency and request a pay-for-delete agreement in writing before you pay anything. Expect modest improvements within 30 to 60 days as accounts update, but meaningful jumps typically take 90 to 180 days of consistent positive behavior.

Timeline and Next Steps Based on Your Current Score

If your score currently sits below 640, focus on payment history and utilization for 90 days before applying. If you sit between 640 and 700, you can apply to multiple lenders now while working to improve further, since some lenders accept these scores and overlays vary significantly. Higher scores above 700 unlock substantially better rates and terms, so the effort to climb from 680 to 720 returns thousands of dollars in savings over your loan term.

Final Thoughts

Your credit score shapes your entire mortgage experience, from whether you qualify to how much you pay over 30 years. The minimum credit score for a mortgage no longer follows a single rule-it depends on your loan type, the lender you choose, and the overlays that lender applies. One rejection doesn’t mean you’re ineligible, since different lenders set different standards and shopping around often reveals approval paths that seemed closed before.

Improving your score before you apply returns real money in tangible savings. Every 20 to 40 points can save you thousands annually in interest costs, so focus on payment history first, then attack your credit utilization, and avoid new credit inquiries during your mortgage search. If your score sits below 640, spend 90 days strengthening it before applying; if you’re between 640 and 700, apply to multiple lenders now while continuing to improve.

Ask your lender specific questions about their overlays and requirements rather than accepting generic answers about minimum credit scores. We at Kearns Mortgage Team offer free consultations and personalized guidance tailored to your financial situation, whether you’re exploring conventional, FHA, VA, USDA, or other loan options. What specific credit improvements could you tackle this month to strengthen your mortgage application?