Buying your first home in Florida is exciting, but navigating the available assistance can feel overwhelming. We at Kearns Mortgage Team know that first-time home buyer programs in Florida exist to help you, yet many buyers don’t know where to start.

This guide walks you through the state and federal programs designed specifically for Florida buyers like you. You’ll learn eligibility requirements, down payment assistance options, and exactly how to apply.

Florida’s First-Time Home Buyer Programs You Need to Know

State Programs That Make the Biggest Impact

Florida offers multiple pathways to homeownership, and understanding which programs match your situation matters far more than knowing every option exists. The Florida Housing Finance Corporation administers the most substantial state-level assistance through its Homebuyer Loan Programs, which pair a 30-year fixed-rate first mortgage with down payment help via second mortgages. The Hometown Heroes program specifically targets healthcare workers, school staff, first responders, public safety employees, child care workers, and military personnel employed full-time by Florida-based employers. This program provides up to 5% of your total loan amount for down payment and closing costs, with a maximum of $35,000 and a minimum of $10,000, structured as a 0% interest deferred second mortgage.

City-Level Assistance Varies Significantly

Beyond state programs, many Florida cities run their own assistance initiatives. West Palm Beach offers up to $100,000, Boca Raton up to $175,000, and Clearwater up to $75,000 for income-qualified first-time buyers. These city programs vary widely in structure, so the amount available in Miami may differ significantly from what’s available in Gainesville or Jacksonville. Your location directly influences which assistance options you can access, making it essential to research programs specific to your target city.

Three Core Eligibility Requirements

Your eligibility hinges on three core requirements: you cannot have owned a primary residence in the past three years, you must meet county-specific income limits that vary by location, and you need a minimum credit score of 640. Florida Housing programs require completion of an approved homebuyer education course before closing, though veterans are exempt from this requirement. The income limits matter significantly because they determine both qualification and the mortgage insurance you’ll pay. Borrowers with household income at or below 80% of the area median income receive reduced mortgage insurance premiums, while those above that threshold pay standard rates.

How Down Payment Assistance Structures Affect Your Monthly Budget

Most programs require the property to be your primary residence in Florida, and you must occupy it within 60 days of closing. When comparing down payment assistance options, focus on whether the second mortgage has monthly payments or is deferred entirely. A deferred second mortgage keeps your monthly obligations lower, which directly affects your debt-to-income ratio and monthly payment affordability. State-level down payment assistance programs offer 0% interest with no monthly payments, while others like the Florida Homeownership Loan Program charge 3% with a 30-year amortizing schedule, creating different cash flow impacts over time.

The structure you select influences not just your immediate affordability but also your long-term financial flexibility. Understanding these differences positions you to make an informed choice that aligns with your financial situation and homeownership timeline.

Programs That Actually Deliver Results

Florida Housing Finance Corporation: Your Primary State Resource

Florida Housing Finance Corporation administers the most effective first-time buyer assistance in the state through two parallel tracks: the BOND program and The Bond Alternative (TBA). The BOND program uses household income to determine eligibility, while TBA relies on credit qualifying income or automated underwriting systems, giving you flexibility depending on your financial situation. Both programs pair a 30-year fixed-rate first mortgage with second mortgage options for down payment help. If you qualify as a healthcare worker, first responder, teacher, or military member earning under your county’s income limit, the Hometown Heroes program delivers real money-and it eliminates the 1% origination fee entirely, saving you thousands at closing.

How Second Mortgage Structures Impact Your Monthly Budget

The second mortgage structures matter tremendously because they directly affect your monthly obligations and debt-to-income ratio. The 0% interest deferred options mean no monthly payment obligations until you sell or refinance, which lowers your debt-to-income ratio and monthly housing costs significantly. Conversely, the 3% amortizing second mortgage through the Florida Homeownership Loan Program creates monthly payments but tops out at $12,500, with the remaining balance deferred upon sale. The forgiveness provisions on certain second mortgages erase 20% of the balance annually over five years when paired with specific first mortgage products, meaning your assistance shrinks your actual repayment obligation substantially.

City-Level Programs Often Exceed State Assistance

City-level programs operate independently and frequently deliver larger assistance amounts than state programs. West Palm Beach provides up to $100,000, Boca Raton up to $175,000, and Clearwater up to $75,000 for income-qualified buyers within city limits. These programs require you to purchase within the specific city boundary, so a home just outside city limits may not qualify despite being geographically close. Your household income must fall below county-specific limits that vary dramatically-a qualifying income in Jacksonville differs substantially from limits in Miami or Gainesville.

Understanding Program Variations and Requirements

Most city programs require the standard 640 minimum credit score and the three-year non-ownership test, but some offer grants while others structure assistance as second mortgages or deferred loans. Property Assessed Clean Energy financing exists as a supplementary tool, not a primary down payment source, allowing you to finance energy efficiency improvements through property tax assessments. This approach preserves your limited down payment funds for the actual home purchase while addressing energy upgrades separately, though PACE financing requires careful evaluation since it creates an additional lien on your property that transfers with ownership.

The specific program you select depends on your occupation, location, income level, and timeline. Your next step involves identifying which programs match your profile and understanding the application requirements that separate qualified applicants from those who miss deadlines or overlook documentation.

Getting Your Application Started

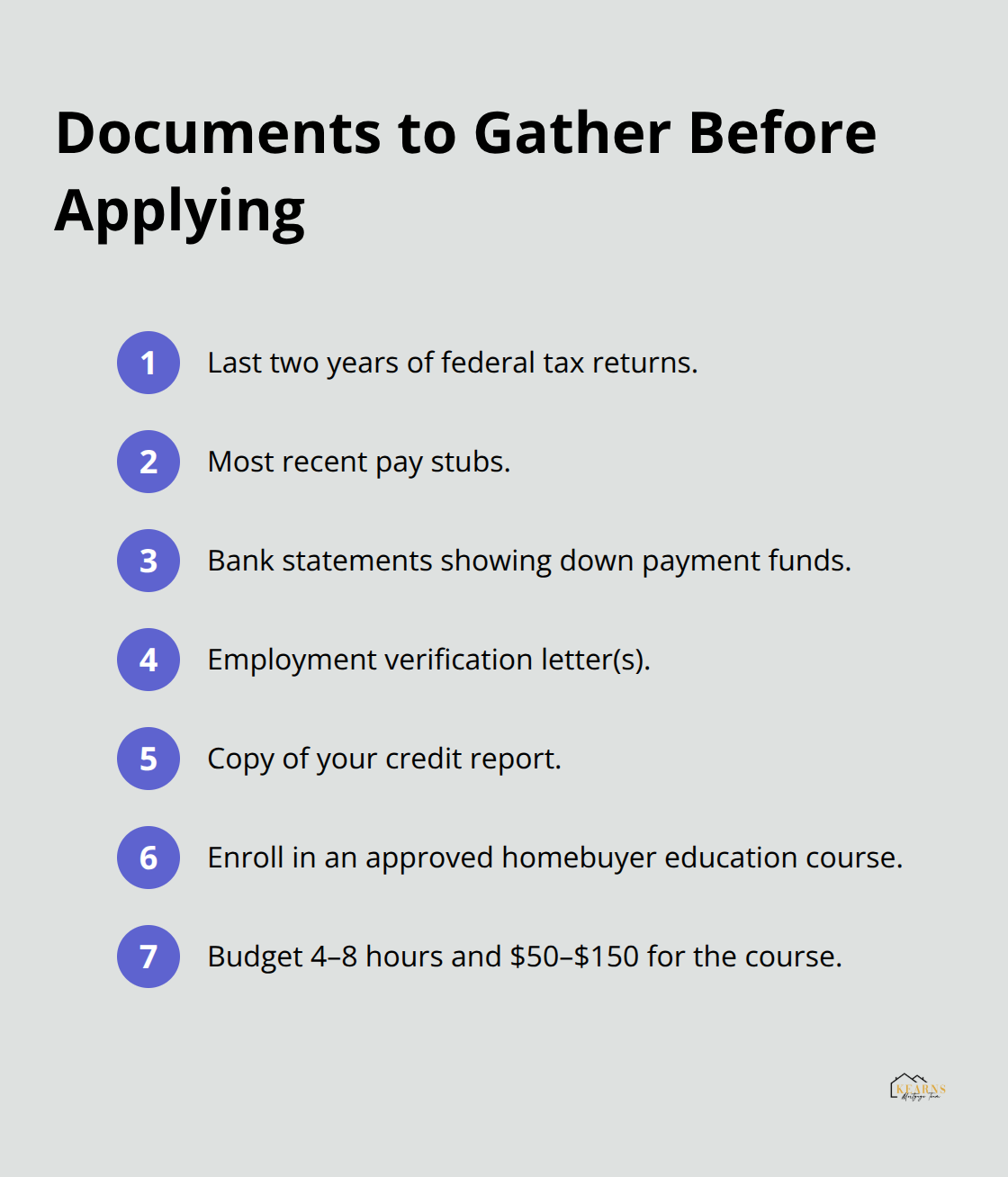

Applying for first-time homebuyer assistance in Florida requires you to gather specific documents before you contact a lender, and having everything prepared upfront accelerates your timeline significantly. You’ll need recent tax returns (typically the last two years), current pay stubs, bank statements showing your down payment savings, employment verification letters, and a copy of your credit report.

Florida Housing programs require you to complete an approved homebuyer education course before closing, so enroll in one immediately rather than waiting until later in the process. The course typically takes four to eight hours and costs between $50 and $150, depending on the provider. Veterans are exempt from this requirement, but if you’re a healthcare worker, teacher, first responder, or military member pursuing the Hometown Heroes program, this step is non-negotiable. Start this course early because some lenders won’t move forward with pre-approval until you’ve completed it and have your certificate in hand.

Your credit score matters because Florida Housing requires a minimum FICO of 640 for most programs, though manufactured housing and manual underwriting require 660. If your credit score falls below 640, pay all bills on time for at least three to six months before applying, as lenders weight recent payment history heavily. Pre-approval differs from pre-qualification because it involves a full verification of your finances and credit, giving you a concrete borrowing amount and demonstrating to sellers that you’re a serious buyer. The pre-approval process typically takes three to five business days once you’ve submitted all documentation. Get pre-approved before you start house hunting because it clarifies your actual purchasing power and prevents you from falling in love with homes outside your budget.

Finding the Right Lender Matters More Than You Think

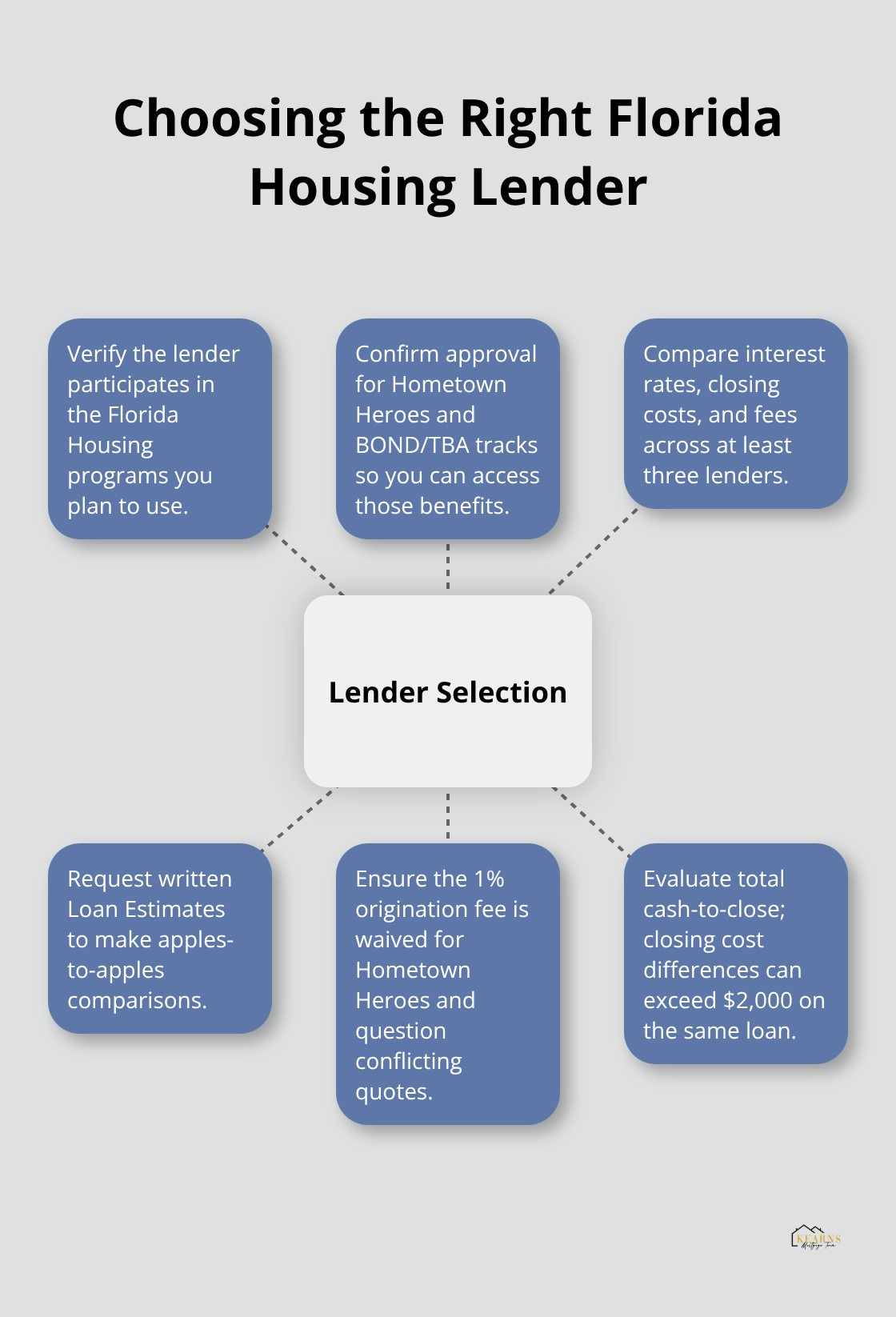

Not every mortgage lender participates in Florida Housing programs, and this limitation directly affects your access to down payment assistance. Florida Housing maintains a Lender and Real Estate Agent Locator on its website where you can find participating lenders in your area. When you contact lenders, ask specifically whether they’re approved for the Hometown Heroes program and the BOND or Bond Alternative tracks, because some lenders specialize in conventional loans only and can’t offer state assistance. Compare at least three lenders on interest rates, closing costs, and origination fees. The Hometown Heroes program eliminates the 1% origination fee entirely, so if a lender quotes you an origination fee for this program, they’re either misinformed or not genuinely participating.

Request loan estimates from each lender in writing so you can compare the actual costs side by side. The difference in closing costs between lenders can easily exceed $2,000 on the same loan amount, making this comparison essential.

Timeline and What to Expect

From initial application to closing typically takes 30 to 45 days if you have all documentation prepared, though it can stretch to 60 days if underwriting requests additional information or if your financial situation is complex. The underwriting process involves verification of employment, income, and assets, which means your lender will contact your employer and bank directly. If you’re self-employed or have commission-based income, expect additional scrutiny and requests for profit-and-loss statements or business tax returns. Once underwriting approves your loan, the lender orders a property appraisal and title search, which typically takes seven to ten business days. Appraisals sometimes come in lower than the purchase price, which can derail your deal or require renegotiation, so budget for this possibility. Clear title is essential because any liens or claims against the property will surface during the title search and must be resolved before closing.

Working With Housing Counselors Saves You Money

Florida Housing and many city programs require or strongly recommend you to work with a HUD-approved housing counselor before closing. These counselors review your specific financial situation and the program you’ve selected, identifying potential issues before they become problems. Counselors cost nothing to $250 depending on the provider, and some nonprofits offer free services. A good counselor explains the second mortgage terms, helps you understand your monthly obligations (including property taxes and insurance), and ensures you’re not overextending yourself. If a lender pushes you toward a program that doesn’t match your financial situation, a housing counselor provides objective guidance and can recommend alternatives. The counseling session typically takes one to two hours and covers budgeting, credit management, and the specifics of your loan structure.

Final Thoughts

Florida’s first-time home buyer programs in Florida offer genuine pathways to homeownership that reduce your upfront costs and monthly obligations significantly. The state programs through Florida Housing Finance Corporation, city-level assistance ranging from $17,400 to $175,000, and specialized initiatives like Hometown Heroes create multiple entry points depending on your occupation, location, and financial situation. The key difference between programs lies in their second mortgage structures, income limits, and occupancy requirements, not in whether assistance exists for your circumstances.

Determining which program fits your situation requires honest assessment of three factors: your employment status and location, your household income relative to county limits, and your timeline for purchasing. If you work as a healthcare provider, educator, first responder, or military member in Florida, the Hometown Heroes program eliminates origination fees and provides up to $35,000 in assistance with zero interest and deferred payments. If you purchase within a specific city, research that city’s program first because local assistance often exceeds state-level help.

The application process moves fastest when you prepare documentation upfront, complete your homebuyer education course immediately, and work with a lender who actively participates in the programs you’ve identified. Housing counselors provide objective guidance at minimal or no cost, helping you avoid programs that overextend your budget or create unnecessary complications. Contact us at Kearns Mortgage Team for a free consultation to understand which first-time home buyer programs match your profile and how to move forward confidently.