If you’re a veteran considering a VA loan, you’ve likely heard about the VA loan funding fee. This one-time charge can seem confusing, but understanding it is essential to your borrowing decision.

At Kearns Mortgage Team, we break down how this fee works, who pays it, and whether you might qualify for an exemption. Let’s walk through the details so you can move forward with confidence.

Understanding the VA Funding Fee

The VA funding fee is a one-time charge paid to the Department of Veterans Affairs to support and protect the VA loan program against defaults. Think of it as the cost of accessing a loan program that requires no down payment and no monthly mortgage insurance. Most veterans pay this fee, though roughly one-third of VA borrowers qualify for exemptions. The fee calculation uses your total loan amount, not the home’s purchase price-this distinction matters because it directly affects how much you’ll owe. If you buy a $200,000 home with a $10,000 down payment, your loan amount becomes $190,000, and the funding fee applies to that $190,000 figure, not the full purchase price.

What You’ll Actually Pay

Your funding fee percentage depends on three factors: whether this is your first VA loan or a subsequent use, how much you put down, and what type of loan you obtain. For first-time home purchases with no down payment, the rate is 2.15% of your loan amount. A 5% or more down payment drops this to 1.5%. A 10% or more down payment reduces it further to 1.25%. On a $300,000 loan with no down payment and first-time use, you pay $6,450 in funding fees.

For subsequent VA loans, the rates increase without a down payment-3.3% instead of 2.15%-but a 5% down payment brings you back to 1.5%. Refinance loans follow their own structure: an Interest Rate Reduction Refinance Loan (IRRRL) carries a 0.5% fee regardless of prior use, while cash-out refinances run 2.15% for first use and 3.3% for subsequent use.

How You Can Pay the Fee

You have three legitimate ways to handle this fee. You can finance it directly into your loan, which spreads the cost across your 30-year mortgage but increases your total interest paid. You can pay it upfront at closing with cash.

Or you can ask the seller to cover it as part of their closing cost concessions (though the VA limits seller contributions to 4% of the home’s reasonable value). Most borrowers choose to finance it because it preserves cash at closing. The lender collects the fee and forwards it to the VA; it operates as a separate transaction from your mortgage itself. Your Certificate of Eligibility indicates whether you owe the fee, and the lender will confirm the exact dollar amount before closing based on your specific loan details and down payment.

The Fee’s Impact on Your Loan

Financing the funding fee into your loan increases your monthly payment and the total interest you pay over the loan term. A $6,450 fee financed over 30 years at a typical interest rate adds roughly $40 to your monthly payment (depending on your rate). However, this approach preserves your cash reserves at closing, which many borrowers find valuable. Paying the fee upfront eliminates this long-term interest cost but requires more cash on hand when you close. Understanding this trade-off helps you decide which payment method aligns with your financial situation.

The funding fee structure rewards borrowers who put money down, and the rates vary significantly based on loan type and usage history. Your next step involves determining whether you qualify for an exemption-a possibility that could eliminate this fee entirely.

How the VA Funding Fee Gets Collected and Paid

When and How Your Lender Collects the Fee

Your lender collects the funding fee at closing and remits it directly to the Department of Veterans Affairs on your behalf. You never interact with the VA directly on this transaction. The exact dollar amount appears on your Closing Disclosure at least three business days before closing, giving you time to review the numbers and ask questions. This advance notice prevents surprises when you sit down to sign documents.

Three Ways to Handle Payment

You have three legitimate options for paying the fee. Financing it into your loan adds the amount to your loan principal immediately, meaning your first monthly payment reflects the higher borrowed amount. Paying it upfront with cash removes it from your monthly obligations entirely but requires more liquidity at closing. The third option involves asking the seller to cover it as a closing cost concession, which reduces your out-of-pocket expenses but limits how much sellers can contribute according to VA guidelines-the seller can agree to pay all of the buyer’s loan-related closing costs without those counting toward the VA’s 4% seller concession limit.

The Math Behind Each Payment Method

Your choice between these three methods should align with your cash position and long-term financial goals. Financing a $6,450 fee over 30 years at a 6.5 percent interest rate adds approximately $40 to your monthly payment, but it preserves your emergency fund and down payment savings. Conversely, paying it upfront eliminates roughly $7,800 in total interest charges over the life of the loan on that same $6,450 fee, making it the mathematically superior choice if you have the cash available. Most veterans finance the fee because they want flexibility with their reserves, but the smartest move depends entirely on whether you have sufficient funds without depleting your safety net.

Confirming Your Fee Before Closing

The lender confirms your specific fee amount and payment method during the loan application process, so you know the exact figure well before closing. VA funding fees range from 0.5% to 3.3%, depending on the loan type, whether you’ve used a VA loan before, and whether you have a down payment. This transparency allows you to make an informed decision about which payment strategy works best for your situation. Your Certificate of Eligibility indicates whether you owe the fee at all-a detail that becomes critical if you qualify for an exemption that could eliminate this cost entirely.

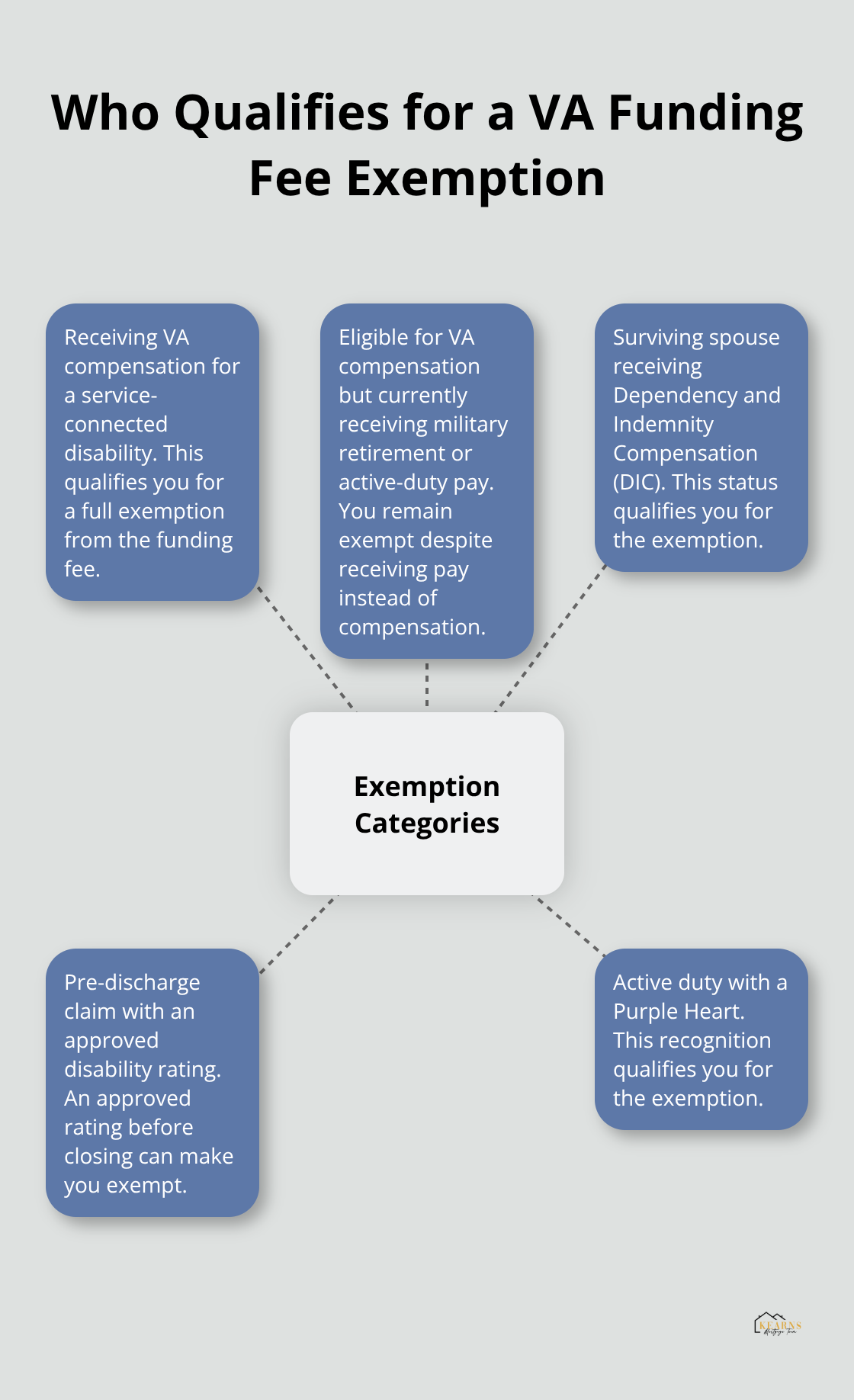

Who Qualifies for a VA Funding Fee Exemption

Exemption Categories That Save You Thousands

About one-third of all VA loan borrowers never pay a funding fee because they qualify for an exemption. The Department of Veterans Affairs grants exemptions to specific groups, and determining whether you fall into one of these categories could save you thousands of dollars. You qualify for an exemption if you receive VA compensation for a service-connected disability, if you are eligible for VA compensation but currently receive military retirement or active-duty pay instead, if you are a surviving spouse receiving Dependency and Indemnity Compensation (DIC), if you have a pre-discharge claim with an approved disability rating, or if you serve on active duty and have received a Purple Heart.

The VA’s definition of service-connected disability does not require a specific rating percentage. Even veterans with a 0% disability rating from the VA qualify for an exemption if the VA has formally recognized the service connection. This distinction matters because some veterans assume they need a higher rating to qualify, which prevents them from asking about their eligibility.

How Your Certificate of Eligibility Reveals Your Status

Your Certificate of Eligibility reveals whether the VA recognizes you as exempt. When you apply for a VA loan, the lender checks your eligibility status against VA records, but the process is not always automatic. The lender will confirm your specific exemption status during the loan application process, so you know your exact fee obligation well before closing.

If your disability compensation was awarded after you previously took out a VA loan and paid the funding fee, you may qualify for a refund on that earlier fee. The VA processes refunds when compensation is granted retroactively to a date before your loan closing. Contact the VA regional loan center at 877-827-3702 (TTY: 711) during business hours, Monday through Friday, 8:00 a.m. to 6:00 p.m. ET, to explore refund eligibility.

Taking Action on Your Exemption

Do not assume your exemption status is already documented in the system. Proactively confirm your eligibility with your lender before closing. If you are unsure whether your military service qualifies you for a disability rating or exemption, the VA’s own website provides detailed guidance on service-connected conditions.

Many veterans leave money on the table simply because they never ask whether they qualify. This represents one of the easiest ways to reduce your loan costs with zero additional effort on your part. Your lender can help you verify your status and identify any exemptions you may have overlooked.

Final Thoughts

The VA loan funding fee represents a manageable cost for accessing one of the most favorable mortgage programs available to veterans. Your actual expense depends on your loan type, down payment size, whether you’ve used VA benefits before, and whether you qualify for an exemption. A first-time purchase with no down payment costs 2.15% of your loan amount, while putting 5% or more down reduces this to 1.5%, and if you qualify for an exemption due to service-connected disability or surviving spouse benefits, you eliminate this fee entirely-a benefit worth thousands of dollars that roughly one-third of VA borrowers receive.

The funding fee’s impact on your overall loan cost depends on how you pay it. Financing it into your loan preserves cash at closing but increases your monthly payment and total interest paid over 30 years, while paying it upfront with cash eliminates long-term interest charges but requires more liquidity when you close. Neither approach is universally correct; the right choice aligns with your financial situation and priorities.

Before moving forward, confirm three details with your lender: your exact VA loan funding fee amount, whether you qualify for an exemption, and which payment method works best for your circumstances. Many veterans overlook exemptions simply because they never ask, leaving thousands of dollars unclaimed. At Kearns Mortgage Team, we help you navigate these details and identify every opportunity to reduce your costs-what aspect of your VA loan journey feels most uncertain right now?