Florida’s real estate market is shifting fast, and the question of whether it’s a good time to buy a house in Florida doesn’t have a one-size-fits-all answer. Your decision depends on where you stand financially, what you’re looking for in a home, and how you weigh the current market conditions.

We at Kearns Mortgage Team help buyers navigate these decisions every day. This guide breaks down what’s actually happening in Florida’s market right now and what it means for your homeownership goals.

Florida Housing Market Conditions in 2026

Single-Family Homes vs. Condos: Two Different Markets

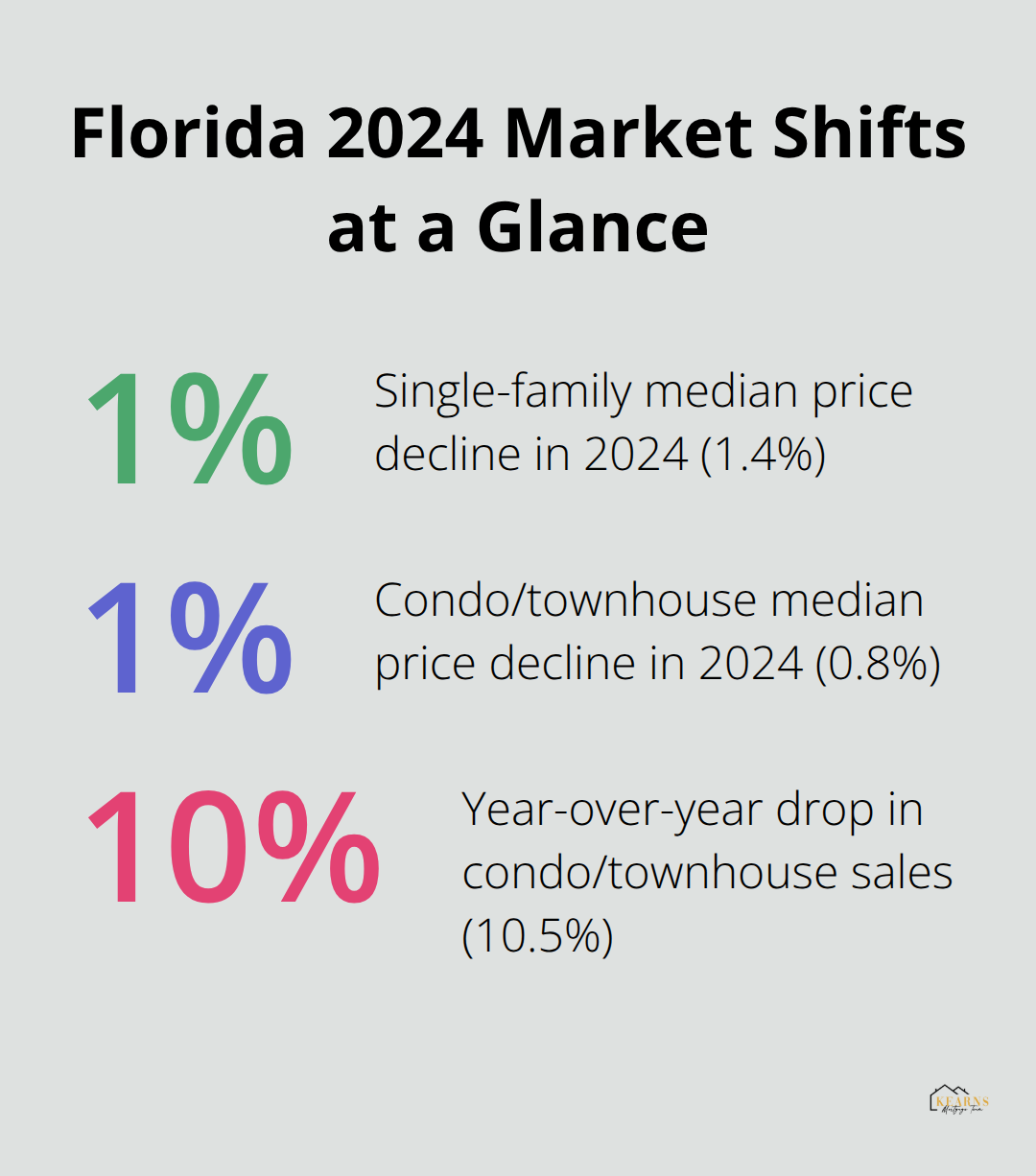

Single-family home prices in Florida ended 2024 at a median of $413,990, down 1.4% from the previous year, according to Florida Realtors data. The condo and townhouse market tells a different story-those properties dropped to $320,000, down 0.8%, with sales falling 10.5% year-over-year.

This split matters because Florida operates as two distinct markets rather than one. If you target single-family homes, you enter a segment that holds its value and maintains a seller’s advantage. If condos appeal to you, inventory has jumped significantly, offering you more negotiating power and potentially lower entry costs. Single-family inventory sits at just 4.7 months of supply, while condo-townhouse inventory reached above 9 months. That gap means condo buyers access substantially more options and face less urgency to overpay.

Mortgage Rates and Your Purchasing Power

Mortgage rates stayed elevated throughout 2024, and that kept buyer demand cautious even as inventory rose. Higher rates compress your purchasing power directly-a $50,000 difference in home price might translate to only a few hundred dollars monthly saved, but the cumulative effect across Florida’s market has been noticeable. What matters now is that rates have stabilized rather than climbed further. If you’ve waited for rates to drop dramatically, that outcome remains unlikely in the near term, but the stability creates an opportunity. Rates won’t surprise you with sudden jumps, so you can lock in pricing with confidence. The mortgage environment rewards buyers who act decisively once they’ve found the right property and secured preapproval. Getting a clear picture of what monthly payment aligns with your budget before you start house hunting eliminates wasted time on properties outside your financial reality and strengthens your offer when competition appears.

Inventory and Market Pace: Your Advantage

Single-family homes move faster than condos, but that doesn’t mean they’re disappearing. Stabilized prices mean sellers aren’t desperately cutting deals, yet buyers aren’t facing the frenzy of 2021 and 2022. Days on market have normalized across most of Florida, giving you time to evaluate properties thoughtfully rather than submit offers within hours. This breathing room proves valuable. You can schedule inspections, review comparable sales, and negotiate repairs without feeling pressured. Condo buyers hold even more advantage-the inventory means sellers compete for your attention. If you remain flexible on property type, exploring condo options unlocks genuine negotiating power that single-family buyers simply don’t possess in this market.

Understanding where Florida’s market stands today sets the foundation for evaluating whether now aligns with your personal circumstances. The conditions favor certain buyers more than others, and the next section examines which factors work in your favor.

Factors Favoring Home Purchases in Florida

Population Growth Sustains Long-Term Demand

Florida added roughly 430,000 residents in 2023 alone, and that migration pattern shows no signs of reversing. The U.S. Census Bureau data confirms Florida remains one of the fastest-growing states, which translates directly into sustained housing demand. Unlike markets dependent on local job creation, Florida’s appeal spans retirees, remote workers, and families relocating from high-tax states. This structural demand floor means your home won’t sit vacant or depreciate from lack of interest. More importantly, that demand supports property values over time. When you buy today, you purchase into a market where demographic tailwinds work in your favor for decades.

Tax Advantages Compound Over Time

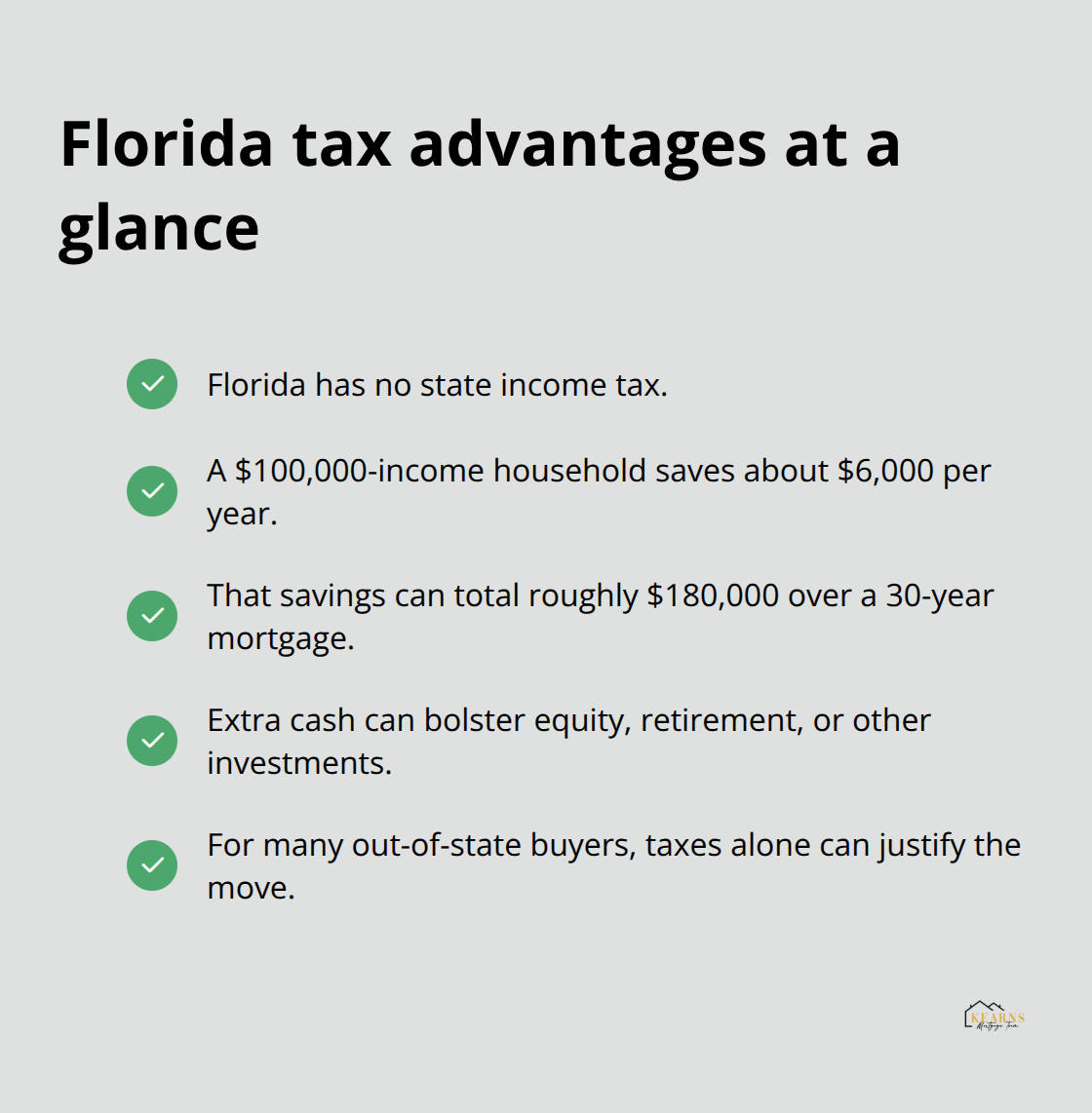

No state income tax amplifies Florida’s financial advantage significantly. A household earning $100,000 annually saves roughly $6,000 per year compared to states like New York or California. That tax savings compounds substantially. Over a 30-year mortgage, you recover an extra $180,000 in spendable income simply by living in Florida rather than a high-income-tax state. That money flows directly into your home equity, retirement accounts, or other investments.

For out-of-state buyers, this tax advantage often justifies the move financially before you even factor in housing affordability.

Affordability Relative to Other Major Markets

Florida’s median home price of approximately $415,000 sits well below California’s $839,000 and New York’s $529,400. You get more square footage, more land, and modern construction standards for substantially less capital. This pricing advantage persists even as Florida attracts significant migration pressure, making entry costs reasonable compared to coastal alternatives.

Diverse Neighborhoods Match Different Lifestyles

Florida’s neighborhoods span dramatically different lifestyles, and that diversity means you aren’t forced into a single market archetype. You can pursue beachfront living in Miami, golf-course communities in the Villages, waterfront properties in Tampa, or inland neighborhoods with lower hurricane exposure and lower insurance costs. That flexibility matters strategically. If you prioritize hurricane resilience and lower premiums, inland locations deliver measurably cheaper insurance without sacrificing access to amenities or employment centers. Coastal properties command premium pricing and face higher insurance burden, but they attract international buyers and maintain stronger appreciation. Retirees find established communities with healthcare infrastructure and social networks already in place. Families discover suburbs with strong schools and space for growing households.

Strategic Selection Reduces Competition

This segmentation means you aren’t competing against all Florida buyers simultaneously. Your specific neighborhood likely faces less competition than the overall market suggests. The condo market particularly benefits from this principle. With inventory above 9 months of supply, you can afford to be selective. You can negotiate repairs, request seller concessions, or walk away without penalty. In single-family segments, that same flexibility applies if you’re willing to look beyond the most popular coastal corridors. Strategic location selection combined with Florida’s demographic momentum creates a genuine window. You’re buying into growth without the urgency that characterized 2021 and 2022.

Yet these advantages exist alongside substantial headwinds that demand your attention before you commit to a purchase.

Factors Working Against Buying Now

Insurance Costs Drain Your Monthly Budget

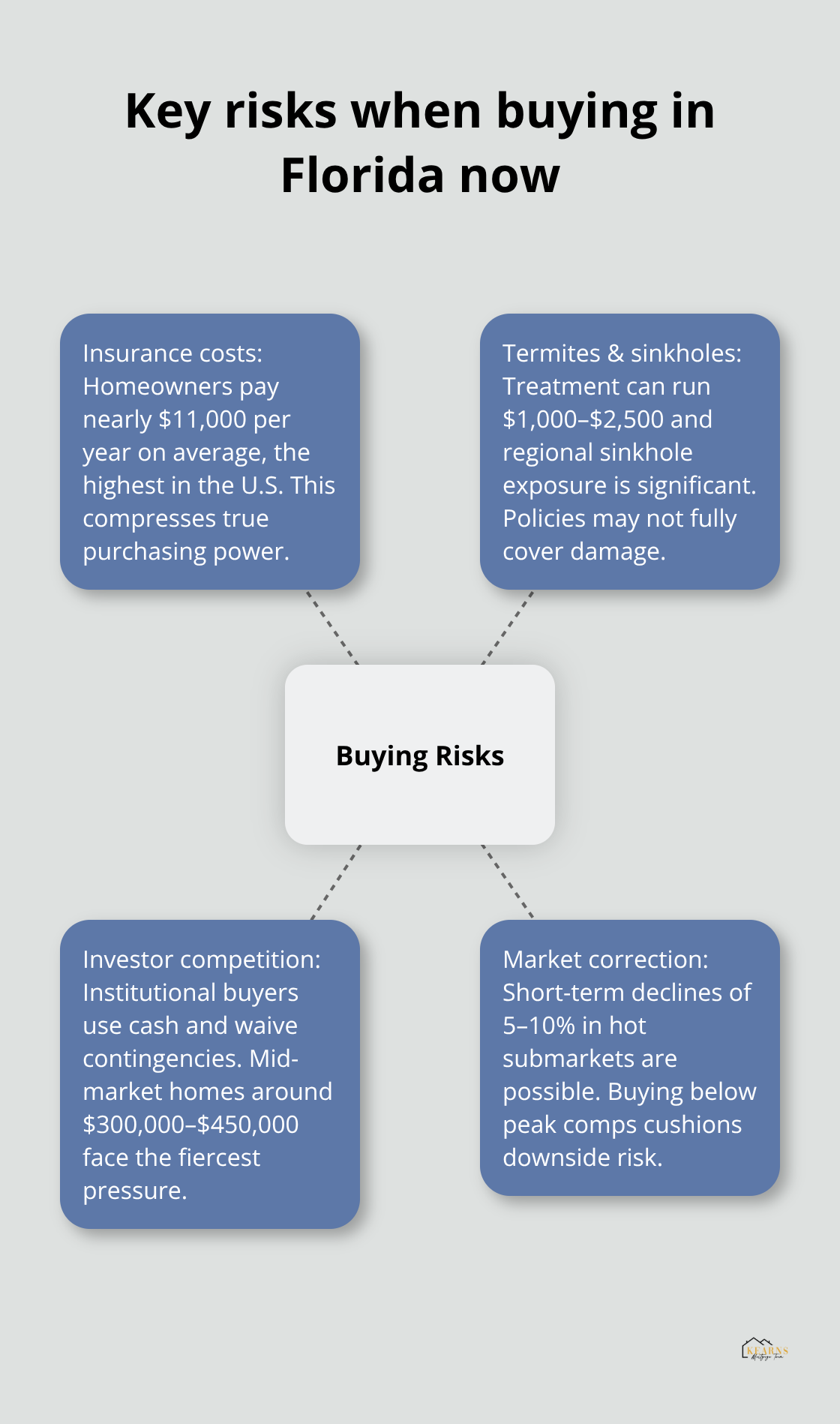

Insurance premiums represent the hidden expense that catches most Florida buyers off guard. The Insurance Information Institute reports that Florida homeowners pay nearly $11,000 annually for coverage-the highest average in the nation. That $11,000 yearly bill translates to roughly $330,000 over a 30-year mortgage when you factor in compounding increases. The Florida Office of Insurance Regulation documented $4.775 billion in property damages from Hurricanes Helene and Milton in 2024 alone, which directly drives carrier costs upward. These numbers aren’t theoretical. They hit your bank account every month and compress your true purchasing power significantly below what your mortgage payment alone suggests.

Termites and Sinkholes Add Unexpected Expenses

Termites infest Florida with particular intensity. The University of Florida confirms that termite species operate across the state, with treatment costs ranging from $1,000 to $2,500 depending on infestation severity. Roughly half of south Florida homes could face subterranean termite infestations by 2040 according to University of Florida projections. Sinkholes present a third climate-related risk. Florida has more sinkholes than any other state due to limestone bedrock, with central and northern areas particularly vulnerable. Your homeowners policy may not fully cover sinkhole damage, so you need to review coverage specifics with your insurer before closing. These three cost categories-insurance, termite treatment, and sinkhole risk-represent concrete, recurring, or emergency expenses that compress your true purchasing power.

Investor Competition Limits Your Negotiating Power

Investor competition and out-of-state capital have fundamentally changed Florida’s negotiating dynamics. Institutional buyers and investment firms now purchase substantial portions of available inventory, particularly in emerging submarkets where values appear underpriced relative to coastal properties. This competition means you face buyers with access to all-cash offers, no inspection contingencies, and willingness to waive appraisal gaps. Your conventional mortgage offer, while reasonable, carries conditions that investors avoid. The practical implication: try neighborhoods where single-family homes command prices above $500,000 or below $250,000, where investor economics become less attractive. Mid-market properties between $300,000 and $450,000 face the fiercest competition from institutional capital.

Market Correction Risk Threatens Short-Term Equity

Market correction risk remains genuine. While Florida’s demographic momentum provides long-term support, short-term price declines of 5–10% in overheated submarkets wouldn’t shock experienced observers. If you buy at peak pricing in a hot neighborhood, you could face negative equity within 18 months if the broader market corrects. The safest strategy involves purchasing properties priced conservatively relative to comparable sales, not at the absolute top of market range. This approach protects you against correction risk while positioning you for appreciation when demand rebounds.

Final Thoughts

The answer to whether it’s a good time to buy a house in Florida depends entirely on your financial position, timeline, and risk tolerance. Florida’s market presents genuine opportunities alongside real headwinds that demand honest assessment. If you’re financially stable with solid credit, a meaningful down payment, and plans to stay in Florida for at least five years, the demographic tailwinds and tax advantages create a compelling case for action.

However, if you’re stretched financially or uncomfortable with elevated insurance costs, sinkhole risk, and termite exposure, waiting makes sense. The $11,000 annual insurance bill isn’t negotiable, and it compounds dramatically over a 30-year mortgage. Market correction risk remains real in overheated neighborhoods, so buying at peak pricing in hot submarkets exposes you to short-term equity loss.

Move forward with your purchase when three conditions align: you’ve secured preapproval and understand your true monthly payment (including insurance and property taxes), you’ve identified neighborhoods where prices reflect realistic comparable sales rather than speculative peaks, and you’re prepared to stay in the property long enough for appreciation to offset transaction costs and climate-related expenses. Contact Kearns Mortgage Team for a free consultation to understand your true purchasing power before you begin house hunting.