If you’re a veteran looking to buy a home in Florida, VA loan requirements Florida might seem complicated at first glance. We at Kearns Mortgage Team know that understanding your eligibility, benefits, and the myths surrounding VA loans can make your homebuying journey much smoother.

This guide breaks down everything you need to know to move forward with confidence.

Who Qualifies for a VA Loan in Florida

Your service history determines whether you can access VA loan benefits, and the requirements are more forgiving than most people think. Service members need at least 90 consecutive days of active duty to qualify, while veterans’ minimums depend on when they served. If you served during the Gulf War era through today, you need 24 continuous months or 90 days under certain qualifying exceptions like hardship or medical discharge. National Guard members qualify with either 90 days of non-training Title 10 activation or 6 creditable years of service with ongoing commitment or honorable discharge. Reserve members follow similar rules: 90 days of non-training active duty or 6 creditable years in the Selected Reserve, with continued service or honorable discharge required.

Discharge Status and Eligibility Exceptions

The Department of Veterans Affairs recognizes discharge exceptions, meaning you might still qualify even if you didn’t meet standard service length. If you faced hardship, received early discharge, or have a service-connected disability, you could be eligible. Dishonorable discharges, bad conduct discharges, and other-than-honorable separations typically block eligibility, though you can pursue a discharge upgrade through the VA Character of Discharge review process. This pathway exists specifically for veterans whose discharge status doesn’t reflect their actual service record.

Obtaining Your Certificate of Eligibility

Your Certificate of Eligibility, or COE, proves your eligibility to lenders and shows your entitlement amount, which determines how much you can borrow without a down payment. You can request one online through the VA’s system and check your status immediately after applying. Some lenders will submit the COE application on your behalf, which saves you a step. Basic entitlement covers loans up to $144,000 with no money down, while bonus entitlement kicks in for larger loans and equals 25 percent of your county’s loan limit. Florida follows Federal Housing Finance Agency conforming limits, so your maximum borrowing power depends on whether you’re buying in Miami-Dade County, rural North Florida, or somewhere in between. If you’ve already used entitlement on a previous VA loan, your remaining entitlement determines your current buying power. Surviving spouses can obtain a COE if they’re eligible for Dependency and Indemnity Compensation or if the service member is missing in action.

Florida Residency and Occupancy Rules

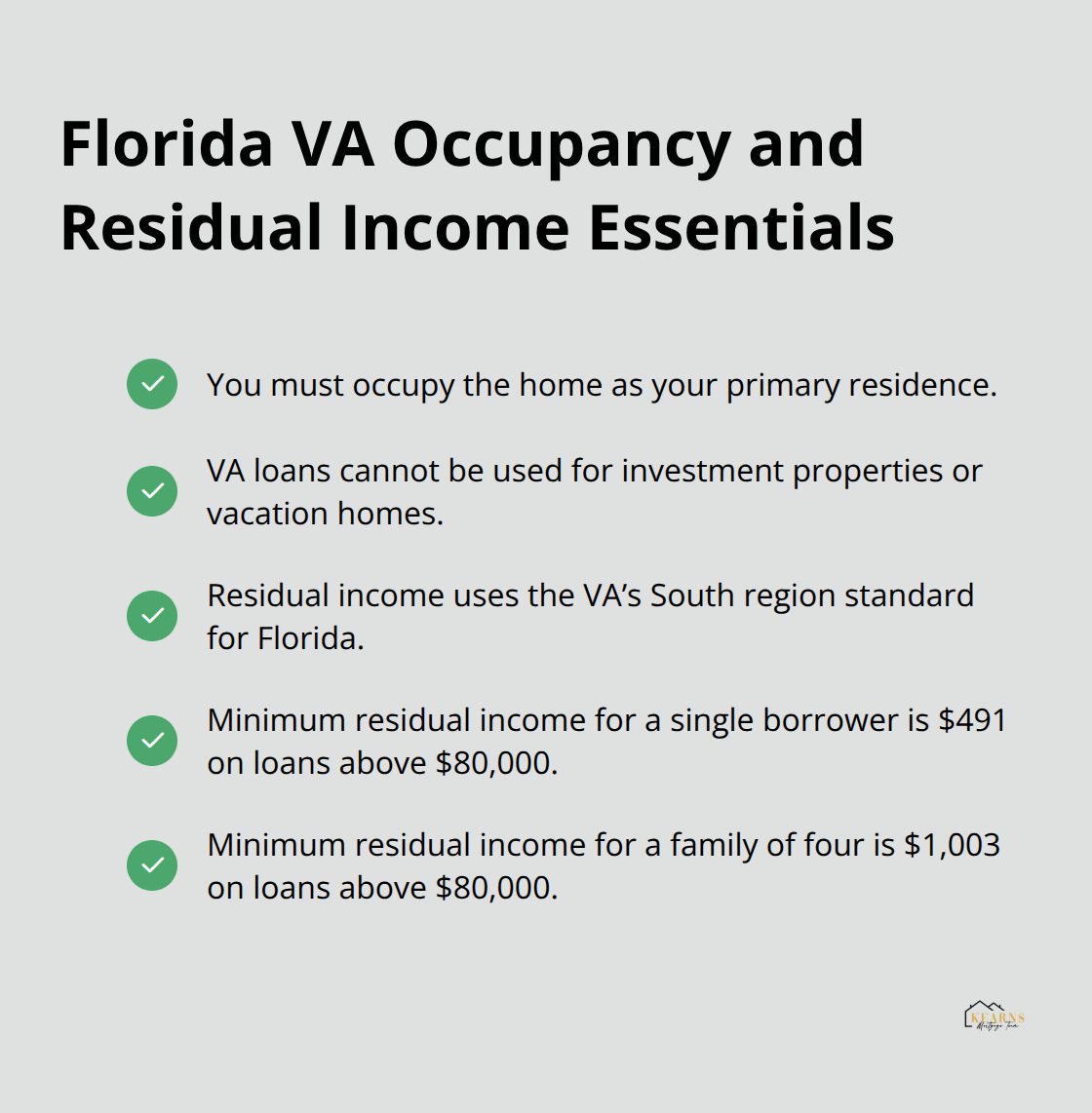

Florida imposes no special residency requirements for VA loans beyond what the VA itself demands. The VA requires that you occupy the property as your primary residence, which means you cannot use a VA loan for investment properties or vacation homes. This occupancy requirement exists nationwide and applies equally in Florida. What matters more for Florida buyers is understanding your residual income requirement-the discretionary money left after you pay major monthly obligations. Florida falls in the VA’s South region, and residual income minimums vary by family size and loan amount. For loans above $80,000, a single person needs $491 in monthly residual income, while a family of four needs $1,003.

These numbers determine whether lenders will approve your loan despite strong credit and income.

Residual Income and Debt-to-Income Calculations

If your debt-to-income ratio exceeds 41 percent, your required residual income jumps to about 20 percent higher than the baseline. This means a Florida buyer with a $1,003 baseline might need $1,204 in actual residual income. Planning your home purchase around this requirement prevents surprises during underwriting and keeps your monthly payments genuinely affordable. Understanding these two metrics-residual income and debt-to-income ratio-gives you a realistic picture of what lenders will approve before you start your Florida home search.

VA Loans Beat Conventional Options for Florida Buyers

Zero Down Payment Saves Thousands Upfront

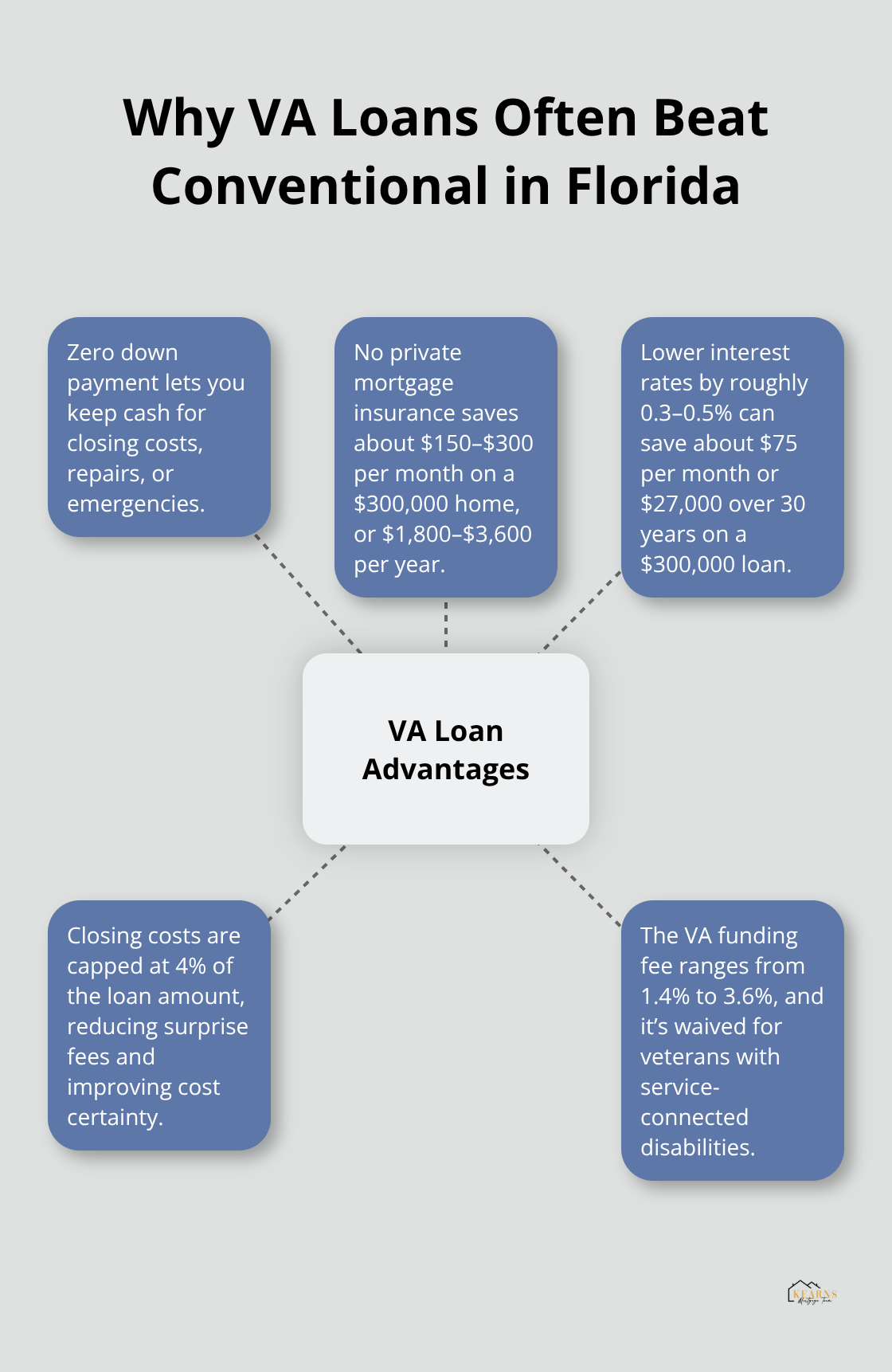

The financial advantage of a VA loan starts before you even close on your home. Unlike conventional loans that require 3 to 20 percent down, VA loans allow you to purchase with zero down payment, meaning you keep tens of thousands of dollars in your pocket for closing costs, repairs, or emergencies. The VA guarantees a portion of your loan, which removes the lender’s risk and eliminates private mortgage insurance entirely. This saves Florida buyers roughly $150 to $300 monthly on a $300,000 home compared to conventional financing-that’s $1,800 to $3,600 annually that stays in your bank account instead of padding an insurance company’s profits.

When you add this savings across a 30-year mortgage, the difference reaches $54,000 to $108,000 in pure cash savings. The VA funding fee, a one-time charge that covers program costs, runs between 1.4 and 3.6 percent depending on your down payment and whether it’s your first VA loan. Veterans with service-connected disabilities receive a complete waiver of this fee, eliminating the upfront cost entirely. Even without a waiver, the funding fee costs significantly less than the years of mortgage insurance premiums conventional buyers pay.

Interest Rates and Closing Cost Protections

VA loan interest rates consistently run 0.3 to 0.5 percent lower than conventional mortgages. On a $300,000 loan, that quarter-point difference translates to roughly $75 monthly savings, or $27,000 over 30 years. The VA also caps closing costs at 4 percent of the loan amount, protecting you from surprise fees that conventional buyers often encounter during underwriting. This protection means you know your true costs before you sign documents.

Assumable Loans and Lifetime Entitlement Reuse

Your VA loan remains assumable throughout its life, meaning if you sell your home to another eligible veteran, they can take over your loan at your original interest rate. This feature becomes invaluable if rates spike, as it makes your home more marketable and protects your buyer from refinancing at higher costs. The lifetime benefit aspect of VA loans means your entitlement can be reused after you sell a home and the loan is paid off, or restored if a qualified transferee assumes your loan. Many Florida veterans use this benefit multiple times throughout their lives, purchasing investment properties or upgrading to larger homes without losing their VA loan advantage. This flexibility distinguishes VA loans from FHA or conventional options, where you’re locked into one borrowing scenario.

Understanding these advantages positions you to make an informed decision about your Florida home purchase. The next section addresses common misconceptions that prevent many eligible veterans from claiming these benefits.

Common Misconceptions About VA Loans in Florida

Your Entitlement Isn’t a One-Time Benefit

Most Florida veterans believe they can only use a VA loan once, or that they must exhaust their full entitlement on a single property purchase. Neither assumption is true, and this misconception costs veterans real money. Your entitlement is reusable after you sell a home, meaning you can buy multiple properties throughout your life using VA financing. If you purchased a $250,000 home fifteen years ago and sold it last year, your full entitlement restored itself the moment the loan paid off. You can now buy again in Florida without losing a single dollar of benefit.

Some veterans strategically use their VA loans for a primary residence, then later purchase investment properties or upgrade to larger homes as their families grow. The VA does not restrict you to one transaction or one property type per lifetime. What matters is that each property meets the occupancy requirement for that specific loan-your primary residence must be owner-occupied, but you cannot flip between multiple owner-occupied homes simultaneously.

Entitlement Restoration Happens Automatically

Entitlement restoration works automatically in most cases, though you can request formal restoration through VA Form 26-1880 if you want official documentation before shopping. A qualified veteran-transferee assuming your loan also restores your entitlement without requiring any action from you. This flexibility means you can plan multiple home purchases across different life stages without worrying about losing your VA loan advantage.

VA Loans Don’t Slow Down Your Timeline

The processing speed myth also deserves correction. VA loans do not inherently take longer than conventional mortgages when you work with experienced lenders who understand VA underwriting. The appraisal requirement, which some believe slows things down, actually protects you by ensuring the property value supports the loan amount. Conventional buyers get appraisals too. What actually matters for timeline is submitting complete documentation upfront and choosing a lender familiar with VA loans in Florida. You can expect your VA loan to close within 40 to 50 days, a standard timeline for the mortgage industry regardless of financing type.

Delays happen when borrowers submit incomplete financial documents or when properties need repairs the VA appraiser flags. You control these variables. The real advantage for Florida veterans isn’t speed-it’s the financial benefit that persists across multiple home purchases throughout your lifetime.

Final Thoughts

VA loan requirements in Florida open doors that conventional financing keeps closed. Eligibility depends on service history, not perfect credit or massive down payments, and your Certificate of Eligibility unlocks borrowing power without mortgage insurance. Your entitlement resets after each home sale, giving you lifetime access to VA financing benefits that compound across multiple properties throughout your life.

Request your Certificate of Eligibility online through the VA or ask a lender to submit it on your behalf. Check your residual income against Florida’s South region minimums for your family size, and calculate your remaining entitlement to understand your buying power without a down payment. Then connect with a lender experienced in VA loan requirements in Florida who can walk you through prequalification and answer questions specific to your situation.

We at Kearns Mortgage Team specialize in VA loans and understand the nuances that make your Florida purchase successful. Contact Kearns Mortgage Team to discuss your VA loan options and start your path to homeownership with a partner who knows your benefits inside and out. What aspect of VA financing matters most to your family’s next chapter?