Your home is likely your biggest asset, and the equity you’ve built in it can be a powerful financial tool. At Kearns Mortgage Team, we help Tampa homeowners understand home equity alternatives that can unlock cash for major expenses, debt consolidation, or life goals.

Whether you’re considering a HELOC, home equity loan, or cash-out refinance, each option works differently. The right choice depends on your timeline, budget, and how you plan to use the funds.

Understanding Your Home’s Equity and How to Use It

What Your Equity Actually Represents

Your home’s equity is the difference between what your property is worth and what you still owe on your mortgage. If your Tampa home is valued at $400,000 and you have a $250,000 mortgage balance, you have $150,000 in equity. This isn’t just a number on paper-it’s real money you can access. Equity builds in two ways: as you pay down your mortgage principal over time, and when your home’s value increases. Tampa’s median sale price reached $460K recently, meaning many homeowners have seen their equity grow simply from living in an appreciating market.

Why Most Homeowners Miss This Opportunity

Most people don’t realize how much equity they’ve accumulated or how to put it to work for them. Tapping into your equity makes sense when you face a major expense-whether that’s a $30,000 roof replacement, consolidating credit card debt at a lower interest rate, or funding a kitchen remodel that adds value back to your home.

The Math Behind Smart Equity Access

The real power of accessing your equity lies in timing and purpose. If you’re paying 18% on credit card debt and you can borrow against your home at 6–7%, the math is obvious: you’ll save thousands in interest while freeing up monthly cash flow. Home improvements funded through equity access often deliver strong returns-bathroom remodels can recover up to 79.9% of their cost at resale, according to the latest Cost vs Value reports.

The Risk You Must Understand

The key is having a clear reason for tapping your equity and understanding that you’re using your home as collateral, which means nonpayment puts your property at risk. This is why choosing the right vehicle-whether a fixed-rate home equity loan with predictable payments, a flexible HELOC for staged projects, or a cash-out refinance that rolls everything into one mortgage-matters far more than most homeowners realize. The wrong choice can leave you overpaying in fees or locked into inflexible terms when your needs change. Each option works differently, and understanding those differences will help you pick the one that fits your situation.

Three Ways to Access Your Home Equity in Tampa

HELOCs: Flexibility for Staged Projects

A HELOC gives you a revolving credit line secured by your home equity, much like a credit card but typically at lower rates. You access funds during the draw period (usually 10 years) and pay interest only on what you borrow. The trade-off is that rates are variable, meaning your monthly payment can increase if rates rise. This flexibility works best when you plan staged home improvements, fund education expenses over time, or manage irregular cash needs. Tampa lenders currently offer HELOCs with variable rates starting around 8–9%, though your actual rate depends on your credit score, equity position, and lender. The draw period eventually ends, and you enter a repayment phase where you can no longer borrow and must pay down the balance, typically over 10–20 years.

Home Equity Loans: Predictability and Fixed Payments

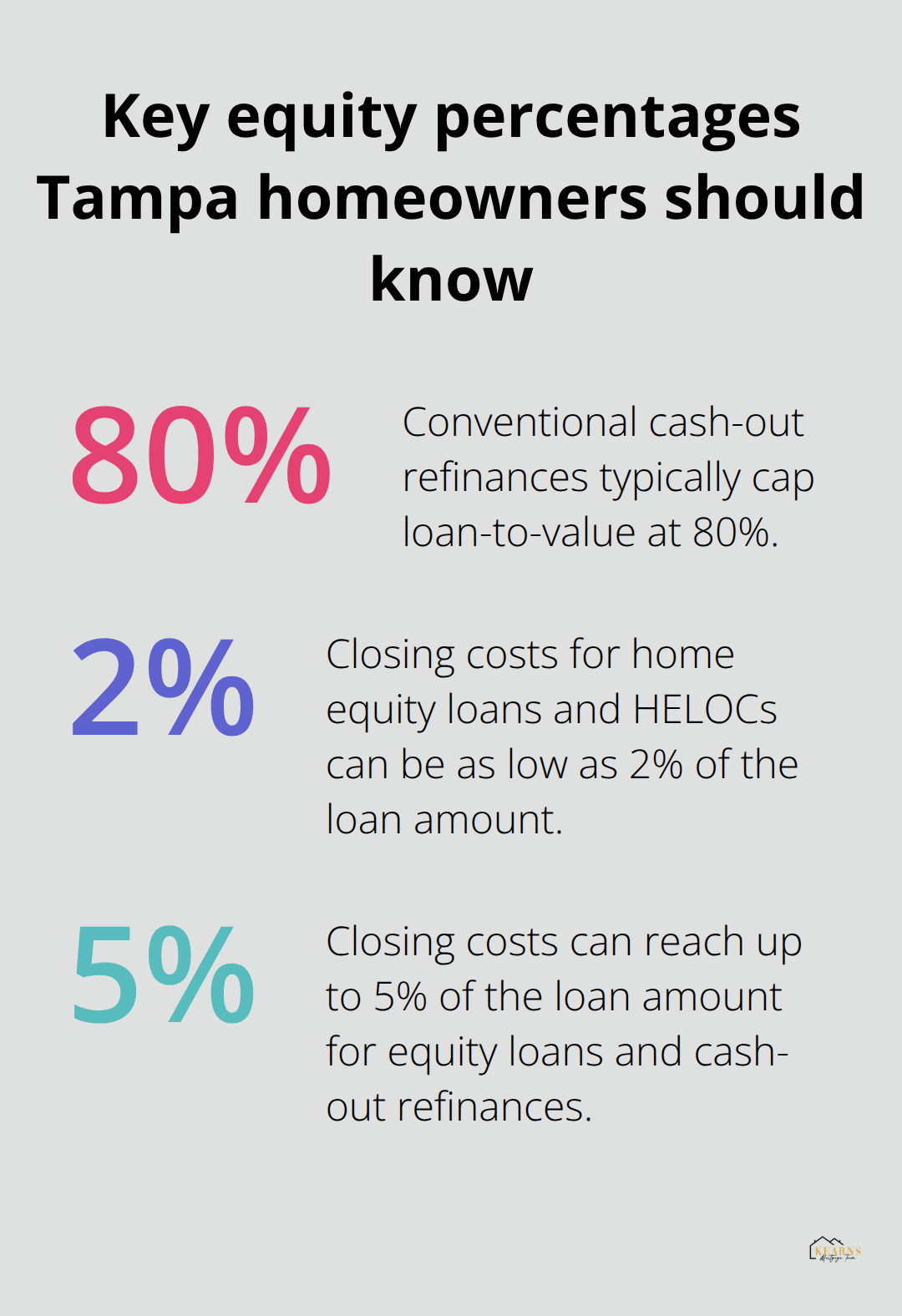

A home equity loan provides a lump sum upfront with a fixed interest rate and fixed monthly payments, giving you certainty in your budget. You know exactly what you’ll pay each month for the entire loan term (usually 5–15 years). This approach suits homeowners with a specific, known expense: a roof replacement, debt consolidation, or a complete kitchen remodel. Fixed-rate home equity loans in Tampa currently range from 7–8.5% depending on your profile, and closing costs typically run 2–5% of the loan amount. The downside is inflexibility-if your needs change, you’re locked into the loan terms. However, the predictability appeals to homeowners who want to eliminate guesswork from their monthly obligations.

Cash-Out Refinancing: Consolidation and Rate Opportunity

Cash-out refinancing replaces your existing mortgage with a larger loan and gives you the difference in cash. If you owe $250,000 on a home worth $400,000 and refinance for $300,000, you pocket $50,000 at closing. This works when you want to consolidate multiple debts into one payment or fund a major project while potentially lowering your overall interest rate. The catch is that you extend your mortgage timeline and increase the total interest paid over the life of the loan. Conventional cash-out refinances typically cap your loan-to-value at 80%, meaning you can borrow up to 80% of your home’s current value. The process takes 30–45 days and requires a fresh appraisal, but if rates have dropped since you bought, this option can meaningfully reduce your monthly housing payment while freeing up cash.

Comparing the Three Options Side by Side

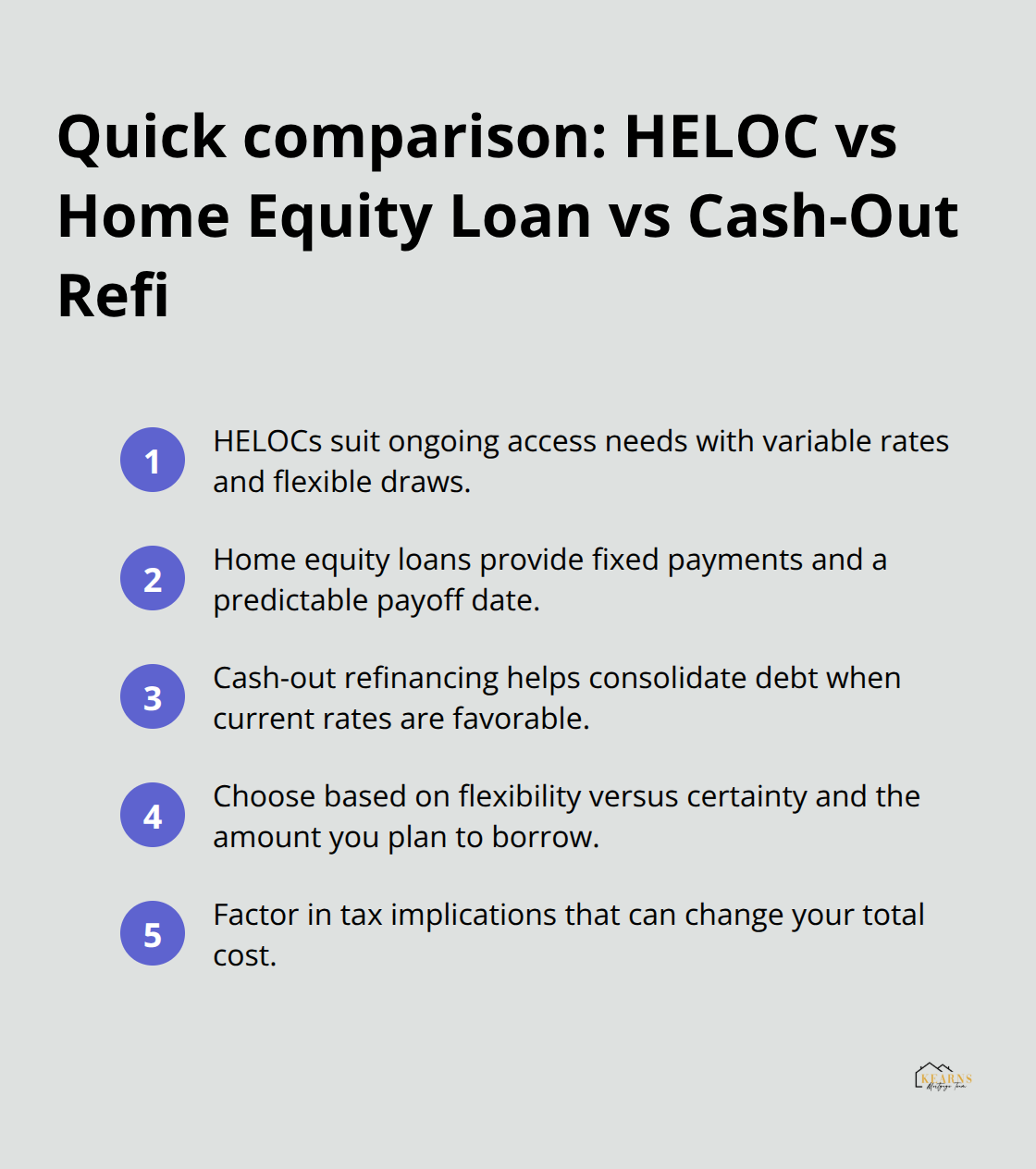

Each option serves a different financial situation. HELOCs work best for homeowners who need ongoing access to funds and can tolerate variable rates. Home equity loans appeal to those who want fixed payments and a clear payoff date. Cash-out refinancing makes sense when you’re consolidating debt or when current rates offer a genuine advantage over your existing mortgage. Your choice depends on whether you need flexibility or certainty, how much you plan to borrow, and your comfort level with variable versus fixed rates.

The next step is understanding how interest rates, fees, and tax implications affect your total cost across these three options.

Which Option Costs Less and Works With Your Timeline

Monthly Payments Tell Different Stories

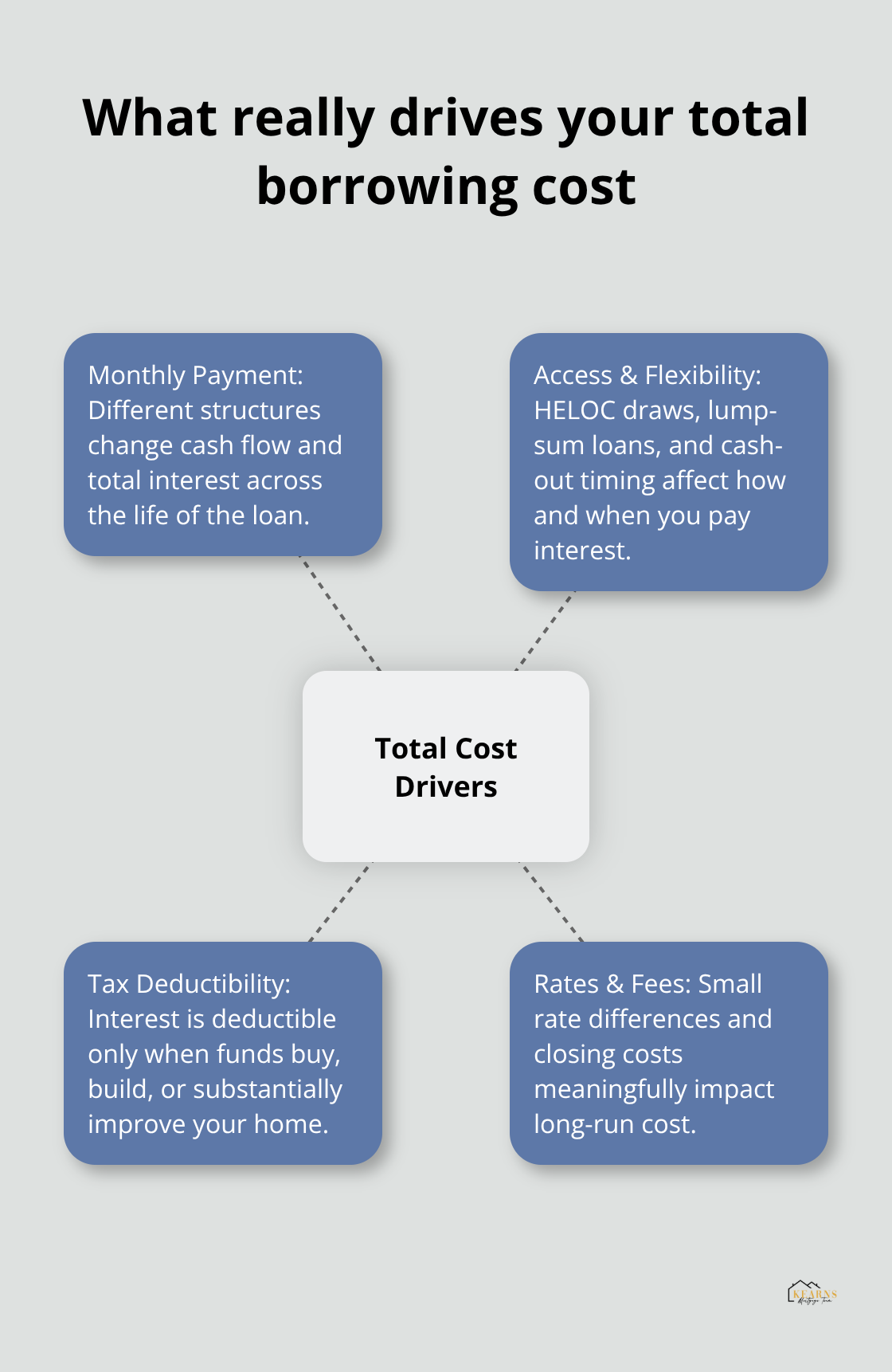

The real difference between these three options shows up in your monthly payment, total interest paid, and how quickly you access funds. A home equity loan at 7.5% on $50,000 over 10 years costs you roughly $595 per month with about $21,400 in total interest. That same $50,000 through a HELOC at 8.5% variable costs around $355 monthly during the draw period, but only if you pay interest-only. Once the draw period ends and you enter repayment, your payment jumps significantly-often doubling or tripling-because you now must repay principal plus interest over the remaining term.

A cash-out refinance tells a different story entirely. If you refinance $300,000 at 6.2% for 30 years instead of your current $250,000 mortgage at 7%, your monthly payment might actually drop from $1,663 to $1,814 despite borrowing $50,000 more. This happens because you extend the payoff timeline, which lowers the monthly obligation even though you pay more total interest over the life of the loan. The math works in your favor only if rates have genuinely dropped or if you consolidate high-interest debt that was costing you more monthly anyway.

Why Tampa Homeowners Overlook Cash-Out Refinancing

A cash-out refinance isn’t always the cheapest option upfront, but it can free up the most monthly cash flow when debt consolidation is the goal. This distinction often gets missed by homeowners focused only on the lowest rate rather than the lowest payment or best overall cash position.

Access and Flexibility Shape Your Real Costs

A HELOC lets you borrow $100,000 but use only $20,000 initially and draw the remaining $80,000 as your renovation progresses-you pay interest only on what you actually use. A home equity loan forces you to take the full amount at closing, meaning you pay interest on funds sitting in your account if you don’t need them immediately. Cash-out refinancing gives you all the money at once, which works perfectly for consolidating multiple debts but poorly if you fund a staged project.

Tax Deductibility Changes Everything

Tax deductibility applies only if you use the borrowed funds to buy, build, or substantially improve your home. The IRS allows this under current rules, but using equity for a vacation or car purchase makes the interest non-deductible. This distinction matters enormously: a $50,000 home equity loan used for a kitchen remodel at 7.5% becomes partially tax-deductible if you itemize deductions, potentially saving you $500–$1,000 annually depending on your tax bracket. That same loan used for credit card consolidation offers zero tax benefit.

Shopping for Rates and Fees Requires Comparison

A 0.5% difference on a $100,000 loan costs you roughly $50 monthly or $18,000 over 30 years. Closing costs for home equity loans and HELOCs typically run 2–5% of the loan amount, while cash-out refinances average 2–5% as well but include appraisal fees and title work that add another $500–$1,500. The lowest rate isn’t always the best deal if that lender charges $3,000 in fees while a competitor charges $800 for a rate only 0.25% higher.

You should obtain rate quotes from at least three lenders for each option you’re seriously considering to see the full picture of what each choice actually costs.

Final Thoughts

The three home equity alternatives Tampa homeowners can pursue each serve distinct financial situations. A HELOC offers flexibility for staged expenses and changing needs, though variable rates mean your payment can shift over time. A home equity loan provides certainty with fixed payments and a clear payoff date, making budgeting straightforward. Cash-out refinancing consolidates debt and potentially lowers your overall mortgage payment, but extends your loan timeline and increases total interest paid across decades.

Your choice hinges on three core factors: your timeline and how you plan to use the funds, your comfort with variable versus fixed rates, and the tax implications of your decision. A single, known expense like a roof replacement favors a fixed-rate home equity loan, while staged improvements point toward a HELOC. Debt consolidation often makes cash-out refinancing the smartest move, and only interest on funds used for home improvements qualifies for tax deduction. If rising rates would strain your budget, a fixed-rate loan removes that uncertainty; if you can tolerate payment fluctuations, a HELOC’s lower initial cost saves money upfront.

Gather your financial documents and obtain rate quotes from multiple lenders to move forward with confidence. Compare not just interest rates but total costs including closing fees, appraisal charges, and title work-the lowest rate rarely equals the lowest total cost. We at Kearns Mortgage Team help Tampa homeowners evaluate their options and find the path that truly fits their financial goals, so contact us for a free consultation to explore which alternative makes sense for your situation.