Buying a home in Florida is one of the biggest financial decisions you’ll make, and getting preapproved for a mortgage puts you in the driver’s seat from day one.

At Kearns Mortgage Team, we’ve seen firsthand how preapproval transforms the entire Florida home buying process-from making stronger offers to closing faster. This roadmap walks you through exactly what you need to know and do to get preapproved and move confidently toward homeownership.

Understanding Mortgage Preapproval in Florida

What Preapproval Really Means for Florida Buyers

A mortgage preapproval is your lender’s formal confirmation of how much you can borrow based on a thorough review of your income, assets, and credit score. This isn’t a casual estimate or a promise-it’s a conditional commitment backed by verified financial documentation. When you apply for preapproval, your lender examines your W-2s, recent pay stubs, tax returns, bank statements, and credit history to determine your exact borrowing capacity. The result is a mortgage preapproval letter that states your approved loan amount, and this letter becomes your entry ticket to the Florida housing market. Most sellers won’t take your offer seriously without one, and in Florida’s competitive real estate environment, preapproval often makes the difference between closing on your dream home and losing it to another buyer. The preapproval process typically takes one to seven days, depending on how quickly you provide necessary documents, and your preapproval remains valid for 60 to 90 days-so timing matters.

Preapproval vs. Prequalification: Know the Difference

Many people confuse preapproval with prequalification, but they’re fundamentally different. Prequalification is a quick, informal estimate based on information you provide over the phone or online, requiring no documentation and no credit check. It offers a rough sense of your borrowing power, but it carries no weight with sellers. Preapproval, on the other hand, involves a detailed financial review, a hard inquiry on your credit report, and actual verification of your income and assets. Your preapproval letter is a formal document that signals to sellers you’re a serious buyer with financing already arranged. This distinction matters enormously in Florida’s market: a prequalified buyer looks like a tire-kicker, while a preapproved buyer looks ready to transact. If your preapproval expires during your home search, you’ll need to reapply with updated documents and another credit check, so stay aware of your expiration date and ask your lender about extensions well in advance.

The Real Financial Advantage of Preapproval

You’ll know your maximum loan amount, your likely interest rate range, and your estimated monthly payment when you secure preapproval before you start house hunting-eliminating the frustration of falling in love with homes outside your price range. More importantly, preapproval protects you from overextending yourself. Many buyers make the mistake of waiting until after they find a house to apply for preapproval, only to discover they can’t actually qualify for the loan amount they need. Starting with preapproval means you shop within reality, not fantasy. In Florida’s competitive markets, preapproval also gives you negotiating power: sellers are far more likely to accept your offer if you’ve already cleared the financial hurdles. Additionally, securing preapproval early allows you to lock in your interest rate before rates move, protecting yourself against potential increases while you search for your home.

Moving Forward with Your Preapproval

Now that you understand what preapproval means and why it matters, the next step is to gather the right documentation and find a lender who understands your specific situation. The documents you’ll need and the lender you choose will shape how smoothly your preapproval process unfolds.

Getting Preapproved: What Documents You’ll Need and How to Choose Your Lender

Organize Your Financial Documents First

The preapproval process moves fast when you come prepared. Start by collecting your financial documents before you contact a lender. If you work as an employee, bring your two most recent pay stubs and your W-2s from the last two years. If you receive overtime or bonuses, grab your year-end pay stubs to show the full picture of your income. Self-employed borrowers need a different approach: you’ll submit your profit and loss statement for the current year plus tax returns from the last two years to verify consistent income.

If you have rental income, your most recent tax return documents that source. Military borrowers should prepare Leave and Earnings Statements to show active duty income. Next, collect 60 days of bank statements for any account you’ll use for your down payment or closing costs. If you’re using a 401(k), provide the most recent quarterly statement. For investment accounts, CDs, or IRAs, bring two months of statements.

Prepare Your Housing and Debt Information

You’ll also need your two most recent months of mortgage or rent statements to show your housing payment history. Bring your Social Security card and a government-issued ID like a driver’s license or passport. If you’re using a gift for your down payment, prepare for that conversation now-most lenders ask for a gift letter and proof that the funds actually transferred to you.

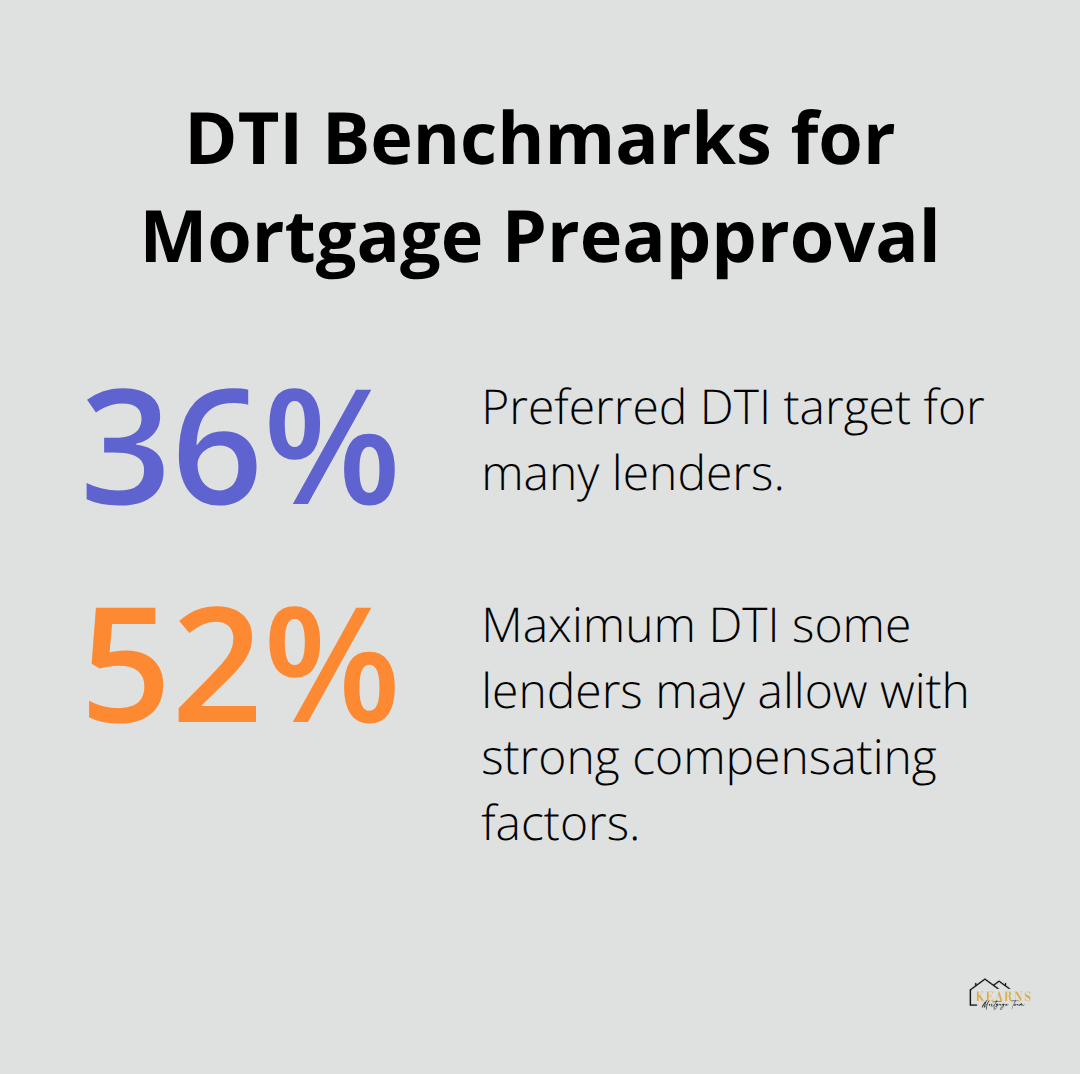

Have a list of all your debts ready: credit cards, car loans, student loans, medical bills, anything with a monthly payment. Your lender calculates your debt-to-income ratio by dividing your total monthly debt payments by your gross monthly income. Most lenders prefer this ratio under 36%, though some approve up to 50-52% with compensating factors like strong savings or a large down payment.

Interview Multiple Lenders to Find Your Match

Choosing the right lender shapes your entire preapproval experience. You want someone who understands Florida’s market and your specific financial situation, not a one-size-fits-all operation. Kearns Mortgage Team offers multiple loan programs including Conventional, VA, FHA, USDA, and Non-QM options, so your lender can match you with what actually works for your situation rather than forcing you into a standard box.

Interview at least two or three lenders before deciding. Ask about their rates, but also ask about their timeline-how long do they typically take from application to preapproval letter? Ask whether they can lock your interest rate during the preapproval period, protecting you if rates rise while you search. Ask about their experience with your loan type; if you’re self-employed or military or buying a rental property, find someone who regularly handles those situations.

Submit Your Application and Move Through Underwriting

When you apply with multiple lenders, do it within a 14-45 day window; prequalification can allow you to shop around without a hard credit inquiry. Once you’ve chosen your lender, submit your application and documents. Your lender’s underwriting team reviews everything-income verification, asset verification, employment history, credit report-and typically completes preapproval within one to seven days depending on how quickly you provide what they ask for. They’ll contact your current employer to verify your job and salary, so stay in touch with your HR department. If anything is unclear or they need additional paperwork, respond immediately; delays here delay your entire timeline.

With your preapproval letter in hand, you’re ready to move into the next phase: using that letter strategically as you search for homes and make offers in Florida’s competitive market.

Using Your Preapproval Letter to Strengthen Your Offer in Florida

Your preapproval letter is now your most powerful tool in Florida’s competitive housing market. Sellers receive multiple offers on desirable properties, and they’re looking for one signal above all else: you can close. A preapproval letter proves you’ve already cleared the financial hurdles that kill most deals, which means your offer looks less risky than one from a prequalified buyer or someone with no documentation. In Florida’s current market, where homes often receive multiple offers within hours of listing, this advantage matters enormously. When you submit an offer with your preapproval letter attached, you tell the seller your financing is already vetted and verified, not dependent on you jumping through underwriting hoops later.

How Sellers React to Preapproved Buyers

Real estate agents understand the power of preapproval-they push you harder to act quickly once you hold that letter because they know it dramatically increases the likelihood your offer will be accepted. The moment you find a property you want, your agent should submit your offer immediately with your preapproval letter included. Waiting even a few hours can mean losing to another buyer, especially in hot markets like Tampa, Miami, or Orlando where homes sell in days, not weeks. Your preapproval letter also gives you confidence to make a stronger offer-perhaps offering fewer contingencies or a shorter inspection period-because you know exactly what you can afford and that your financing is solid.

The Timeline from Offer Acceptance to Closing

From the time your offer is accepted to closing day, expect four to six weeks in most Florida transactions. Once the seller accepts your offer, your lender moves into the formal underwriting phase, which typically takes 10 to 15 business days. During this time, the underwriting team orders the appraisal, verifies employment one final time, and confirms all the financial information from your preapproval is still accurate.

Protecting Your Approval Between Offer and Closing

This is why maintaining financial stability between preapproval and closing matters-don’t change jobs, make large purchases, apply for new credit, or accumulate new debt, as any of these can trigger a reevaluation and potentially kill your loan approval. After underwriting approves your loan, you’ll receive a clear-to-close status, typically around three to five days before your scheduled closing date. At this point, your lender provides your Closing Disclosure, a detailed document showing your final loan terms, interest rate, monthly payment, and all closing costs. You have the right to review this document for at least three days before closing.

Closing Day and Beyond

During closing, you’ll sign the final paperwork, provide your down payment and closing costs, and receive the keys to your new home. The entire timeline from accepted offer to closing keys in hand usually spans 30 to 45 days in Florida, though some transactions close in as few as 21 days if both parties move quickly and no complications arise (such as appraisal issues or title problems). Your lender’s team stays in contact throughout this period to answer questions and keep everything on track toward your closing date.

Final Thoughts

Preapproval separates buyers who close on homes from those who lose to competitors in Florida’s fast-moving market. You now understand what preapproval means, how it differs from prequalification, and exactly what documents you need to move through the process quickly. Start this week by organizing your financial documents, then contact at least two lenders to compare rates, timelines, and loan programs that fit your specific situation.

We at Kearns Mortgage Team work with borrowers in every situation-conventional buyers, VA borrowers, self-employed professionals, and investors-because your loan program should match your life, not force you into a standard box. We offer free consultations to answer your questions and help you understand exactly what you qualify for, with competitive rates and lifetime support throughout your homeownership journey. Contact Kearns Mortgage Team today to start your preapproval and take control of your path to homeownership in the Florida home buying process.

The Florida housing market rewards prepared buyers who walk into negotiations with a preapproval letter in hand. That confidence, combined with the financial clarity preapproval provides, transforms your entire home buying experience. Ask yourself: Am I ready to commit to homeownership in the next 60 to 90 days, and do I have my financial documents organized and ready to share?