Buying your first home in Tampa is a major financial decision, and the process can feel overwhelming without proper guidance. We at Kearns Mortgage Team have helped countless first-time homebuyers navigate Tampa’s market, and we know what it takes to succeed.

This guide walks you through everything you need to know-from understanding local market conditions to closing on your new home. You’ll learn about financing options, timelines, neighborhoods, and the mistakes to avoid along the way.

What’s the Real Price of Homes in Tampa Right Now

Price Tiers Across Tampa’s Neighborhoods

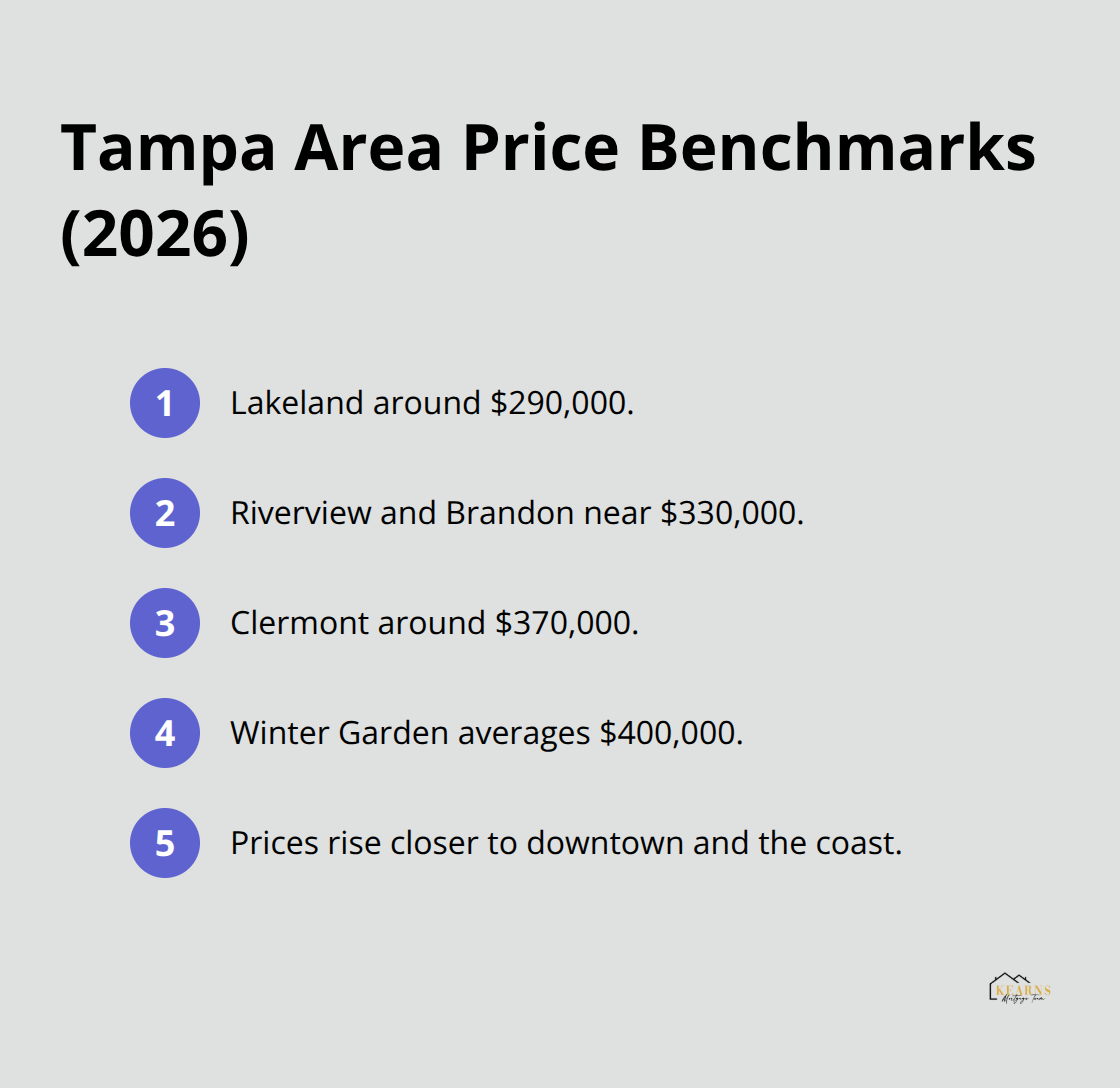

Tampa’s housing market in 2026 shows distinct price tiers based on location, and understanding these differences shapes your entire budget conversation. Inland areas like Lakeland sit around $290,000, while Riverview and Brandon hover near $330,000. If you move closer to Orlando’s western suburbs, Winter Garden averages $400,000 and Clermont around $370,000. Distance from downtown Tampa and coastal areas directly affects what you’ll pay. A $290,000 home in Lakeland requires far less down payment and monthly payment than a $400,000 property in Winter Garden, even with identical loan terms.

Affordability Across Safe Neighborhoods

The Tampa market itself favors buyers willing to look beyond the most popular coastal neighborhoods. Housing inventory in high-growth metros like Tampa, Orlando, and Miami continues to shift as market conditions evolve. Neighborhoods like Ballast Point, Beach Park, Hyde Park, Riverside Heights, and Seminole Heights offer different value propositions. Ballast Point’s median home price sits at $407,620 with a median household income of $97,886, making it a stable but pricier choice. Riverside Heights offers genuine affordability without sacrificing safety-it ranks safer than 75% of Tampa neighborhoods. Seminole Heights is even more accessible at $131,633 median home price, though it ranks safer than only 47% of Tampa neighborhoods.

Timing and Inventory Advantages

New construction in inland Polk County and central Florida areas west of Orlando continues to add inventory, reducing the bidding wars you’d face in established neighborhoods. This inventory growth means you have more negotiating power and a wider range of options than buyers faced in 2024 and 2025. The timing advantage exists right now because multiple neighborhoods simultaneously offer fresh listings and competitive pricing. With these price ranges and neighborhood options in mind, your next step involves calculating what you can actually afford and exploring the financing options that work best for your situation.

How Much House Can You Actually Afford

Calculate Your True Monthly Housing Cost

Your budget isn’t what you want to spend-it’s what you can actually afford without stretching dangerously thin. Tampa’s first-time buyers commonly miscalculate by focusing only on the monthly mortgage payment and ignoring property taxes, insurance, and maintenance costs. The real monthly housing expense includes principal and interest, property tax, homeowners insurance, and private mortgage insurance if your down payment is under 20%. In Tampa, homeowners insurance costs vary by location and property characteristics, and that’s before flood or windstorm coverage, which can add significantly depending on your property’s flood zone and elevation.

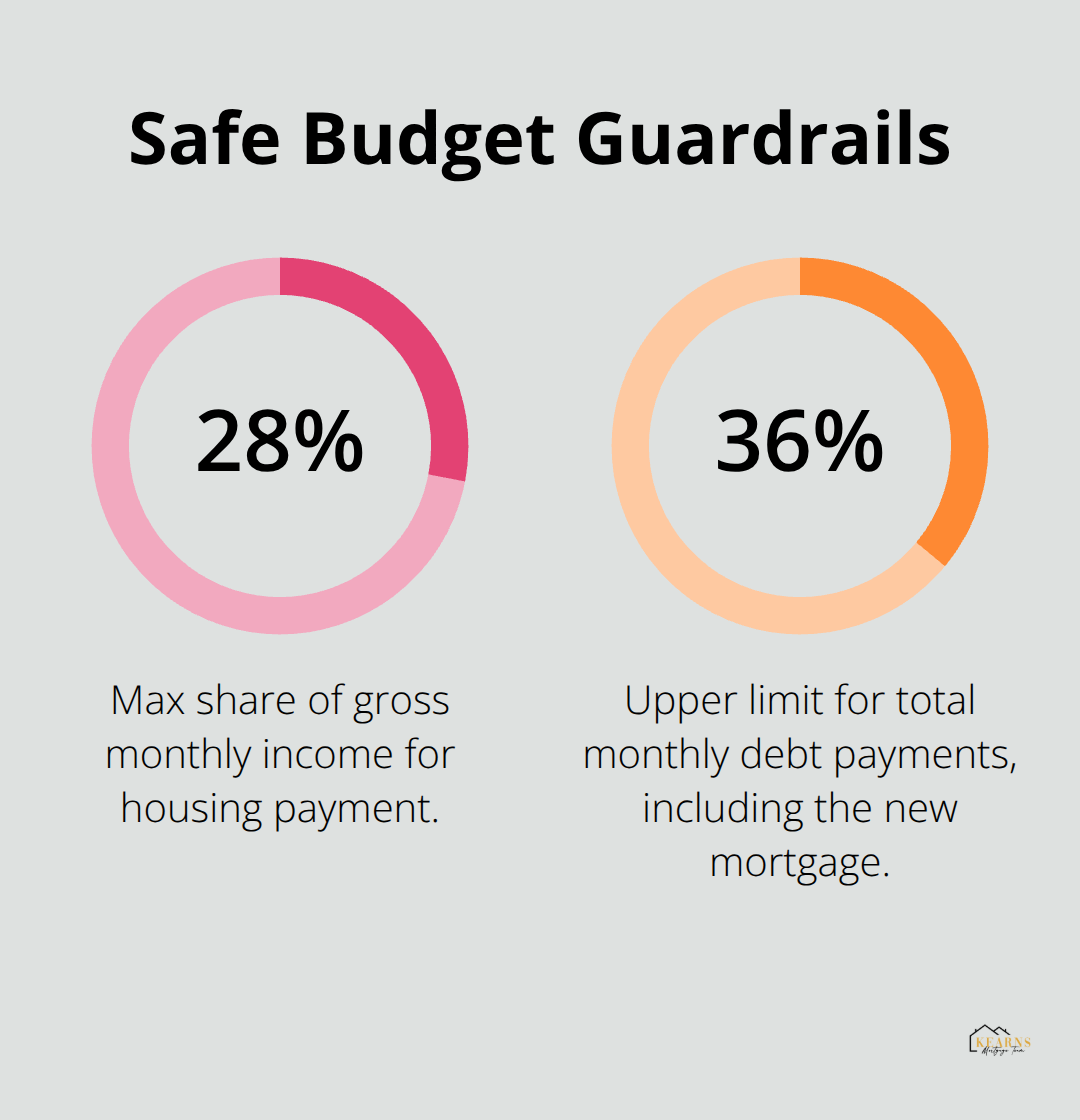

Your housing payment should never exceed 28% of gross monthly income, while total debt stays under 36%. If you earn $5,000 monthly, your maximum total debt obligation is $2,150-and that includes your car payment, student loans, credit cards, and your new mortgage payment combined.

Most Tampa buyers underestimate closing costs, which typically run 2% to 5% of the purchase price. On a $325,000 home, that means $6,500 to $16,250 in closing costs alone, plus your down payment.

Work Backwards From Your Income

Total cash needed to close ranges from 5% to 8% of the purchase price when you combine down payment, closing costs, and prepaid items like insurance and property taxes. A practical approach: calculate backwards from your income. If you earn $60,000 annually, your maximum total debt is roughly $2,150 monthly. Subtract existing debts-if you have a $300 car payment and $100 in student loans, you have $1,750 remaining for your mortgage payment. On a 30-year mortgage at current rates, that $1,750 supports roughly a $320,000 purchase with 5% down, but only after you’ve saved the down payment and closing costs upfront.

Down Payment Options and Private Mortgage Insurance

Down payment options matter more than most Tampa buyers realize, and the myths about needing 20% are costing buyers thousands in unnecessary payments. FHA loans require just 3.5% down with a credit score around 580, while conventional loans through programs like Conventional 97 need only 3% down with a credit score near 620. VA loans offer 0% down for eligible veterans, and USDA loans provide 0% down financing in eligible rural areas outside Tampa’s core. The trade-off for lower down payments is private mortgage insurance on conventional and FHA loans-PMI protects the lender if you default, adding roughly $100 to $300 monthly depending on your loan amount and credit profile.

However, PMI on conventional loans drops automatically once you reach 20% equity, while FHA mortgage insurance premium stays for the loan’s life if you put down less than 10%. This means a conventional loan with 3% down and PMI is often superior to FHA for buyers planning to stay 7+ years.

Get Pre-Approved and Shop Multiple Lenders

Pre-approval differs fundamentally from pre-qualification. Pre-qualification is a rough estimate based on self-reported income; pre-approval involves actual verification of your W-2s, tax returns, pay stubs, and bank statements. Lenders verify employment, check credit scores, review debt, and confirm reserves-the money left after closing. Tampa lenders typically require two months of reserves for conventional loans, meaning if your monthly payment is $1,500, you need $3,000 sitting in savings after closing.

Shopping multiple lenders is non-negotiable. A difference of 0.25% on your rate across 30 years costs roughly $15,000 more in interest on a $300,000 loan. With your budget and financing options clarified, you’re ready to explore the specific loan products and approval timeline that will move you toward an actual offer.

The Home Buying Timeline and Process in Tampa

Your offer to closing in Tampa typically spans 30 to 45 days, and every single day matters because delays cost money and kill deals. The moment your offer gets accepted, your timeline clock starts ticking. You have a narrow window to secure financing approval, complete the home inspection, order the appraisal, and handle any repairs or renegotiations. Most Tampa contracts require inspection contingencies within 10 days of acceptance, so you must schedule and complete your home inspection before that deadline passes. This inspection costs $300 to $500 and reveals structural issues, roof condition, HVAC functionality, plumbing problems, and anything else that could signal expensive repairs. Don’t waive this step under any circumstance, even in competitive markets. A $400 inspection that uncovers a $15,000 roof problem gives you leverage to renegotiate or walk away before you’re locked into a bad deal.

Appraisal and Title Work Run in Parallel

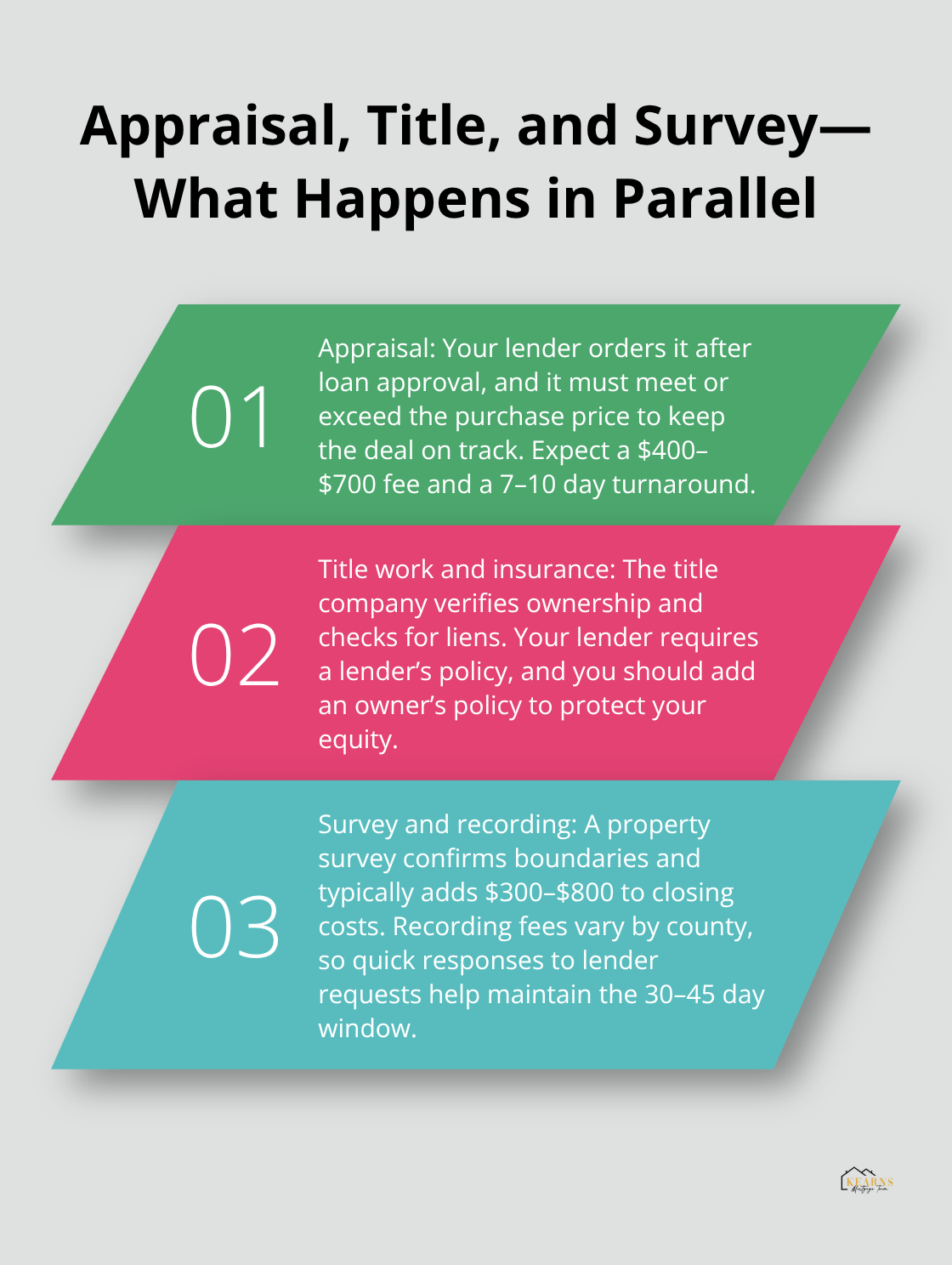

Your lender orders the appraisal immediately after loan approval, and this appraisal must come in at or above your purchase price or your deal stalls. The appraisal costs $400 to $700 and typically takes 7 to 10 days to complete. Meanwhile, the title company searches property records to confirm the seller actually owns the home and no liens exist against it. Title insurance protects you against ownership defects, and your lender requires a lender’s policy while you should purchase an owner’s policy to protect your equity.

Recording fees vary by county, and in Hillsborough County these charges depend on the document type and page count. A property survey confirms exact boundaries, adding another $300 to $800 to your closing costs. All of this happens simultaneously, which is why staying organized and responding quickly to lender requests accelerates your timeline. If you delay providing documents or the appraisal comes back low, your 30 to 45 day window shrinks fast.

Final Walkthrough and Closing Day Logistics

Three days before closing, you receive your Closing Disclosure, a federal document that itemizes every fee and shows your exact monthly payment. Review this document line-by-line because it’s your final chance to catch errors. Confirm that your down payment amount matches what you agreed to, that the interest rate reflects your locked-in number, and that all closing costs align with earlier estimates. Two days before closing, you conduct a final walkthrough to confirm agreed-upon repairs were completed and no new damage occurred. On closing day itself, you wire funds or bring a cashier’s check for your down payment and closing costs, then sign roughly 100 pages of paperwork and receive the keys. Tampa title companies typically close between 10 AM and 2 PM on weekdays, and the entire signing process takes 45 minutes to 90 minutes. Your lender funds the loan, the title company records the deed with Hillsborough County, and you officially own your home.

Final Thoughts

Buying your first home in Tampa requires you to balance multiple moving pieces simultaneously, and the buyers who succeed stay organized and avoid emotional decisions. You must take three foundational actions: secure pre-approval with a lender who understands Tampa’s market, calculate your actual budget based on income and existing debt, and research neighborhoods that align with your lifestyle and financial goals. The first-time homebuyer Tampa market rewards preparation over speed, so resist pressure to rush into offers before you complete this groundwork.

The most expensive mistakes happen before you even make an offer. Stretching your budget beyond what you can comfortably afford leaves no room for maintenance, property tax increases, or insurance premium jumps that inevitably occur in Florida (homeowners insurance, flood coverage, and windstorm protection add hundreds monthly to your housing expense). Skipping the home inspection to appear more competitive in bidding situations costs thousands when hidden problems surface after closing. Not shopping multiple lenders costs you tens of thousands in unnecessary interest over 30 years.

Contact Kearns Mortgage Team for a free consultation to discuss your specific situation. We provide personalized guidance throughout the entire process and offer competitive rates. With the right lender, the right neighborhood choice, and realistic expectations about costs and timelines, your first home purchase in Tampa becomes achievable rather than overwhelming.