Buying your first home feels overwhelming, but the right preparation makes all the difference. We at Kearns Mortgage Team have guided thousands of first-time buyers through this process successfully.

The key lies in understanding your finances, avoiding common pitfalls, and working with experienced professionals. These first time home buyer tips and advice will set you up for homeownership success.

What Can You Actually Afford

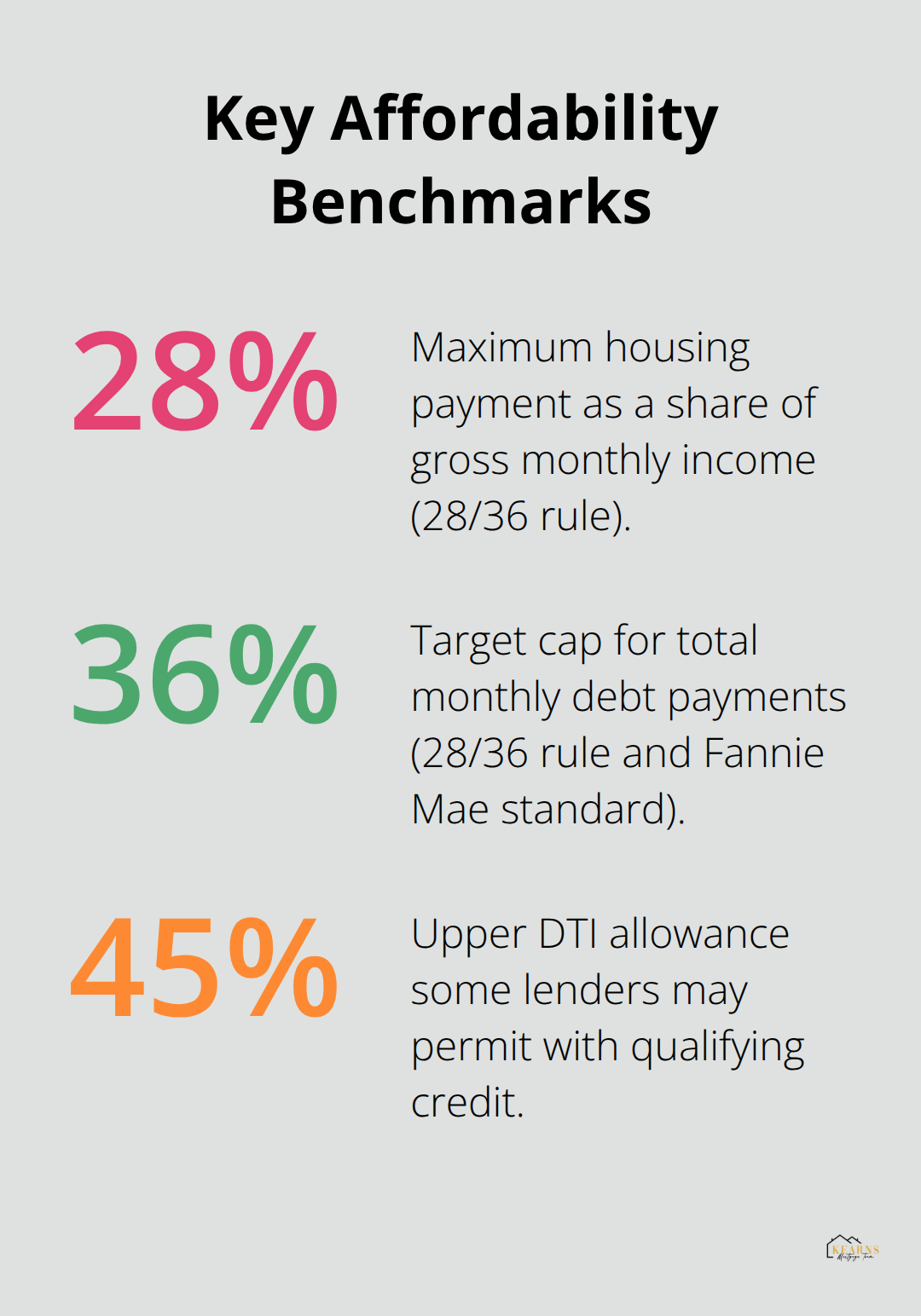

Your debt-to-income ratio determines everything about your home purchase power. Lenders may allow total monthly debt payments up to 45% of your gross monthly income if you meet credit requirements, though Fannie Mae’s standard maximum is 36%. Calculate this by adding all monthly debt payments (including car loans, credit cards, and student loans), then divide by your gross monthly income. A borrower who earns $5,000 monthly with $1,500 in debt payments has a 30% DTI ratio, which puts them in strong position for mortgage approval.

The 28/36 Rule Changes Everything

The 28/36 rule provides the clearest framework for affordability decisions. Your housing payment should never exceed 28% of gross monthly income, while total debt stays under 36%. This means someone who earns $6,000 monthly can afford a $1,680 housing payment maximum. Most buyers ignore this rule and end up house poor within months.

Your credit score directly impacts your interest rate and loan options. Conventional loans require 620 minimum, while FHA loans accept scores as low as 580 with 3.5% down. Higher scores unlock better rates and save thousands over your loan term.

Down Payment Strategy That Actually Works

Save 20% down payment to avoid private mortgage insurance, but don’t let this delay your purchase indefinitely. FHA loans allow 3.5% down, while VA loans require zero down payment for eligible veterans. Beyond your down payment, maintain an emergency fund that covers three to six months of expenses.

Closing costs average 2-6% of your loan amount, which adds $7,700 to $23,100 on a $385,000 purchase according to recent market data. High-yield savings accounts help your down payment fund grow faster while they keep funds accessible when you find the right property.

Pre-Approval Sets Your Budget

Pre-approval gives you real numbers instead of estimates and shows sellers you mean business in competitive markets. This process verifies your income, assets, and credit to determine your exact loan amount. Pre-approval also locks your interest rate for 60-90 days, which protects you from rate increases while you shop for homes.

How Do You Navigate the Buying Process

Pre-approval transforms you from a window shopper into a serious buyer with real purchasing power. Freddie Mac research shows that shopping with multiple lenders can save you $600 to $1,200 annually on mortgage payments. Apply with three to five lenders within a 14-day window to compare rates without damaging your credit score. Each lender evaluates your application differently, so one might approve you for $350,000 while another offers $400,000 based on the same financial profile.

Choose Your Team Wisely

Your real estate agent makes or breaks your home search experience. Interview at least three agents and ask specific questions about their recent sales volume, average days on market for their listings, and negotiation strategies. Top agents handle 15-20 transactions annually and know local market conditions that affect your offer strategy. Never work with an agent who pressures you to increase your budget or skip home inspections.

Timeline and Cost Expectations

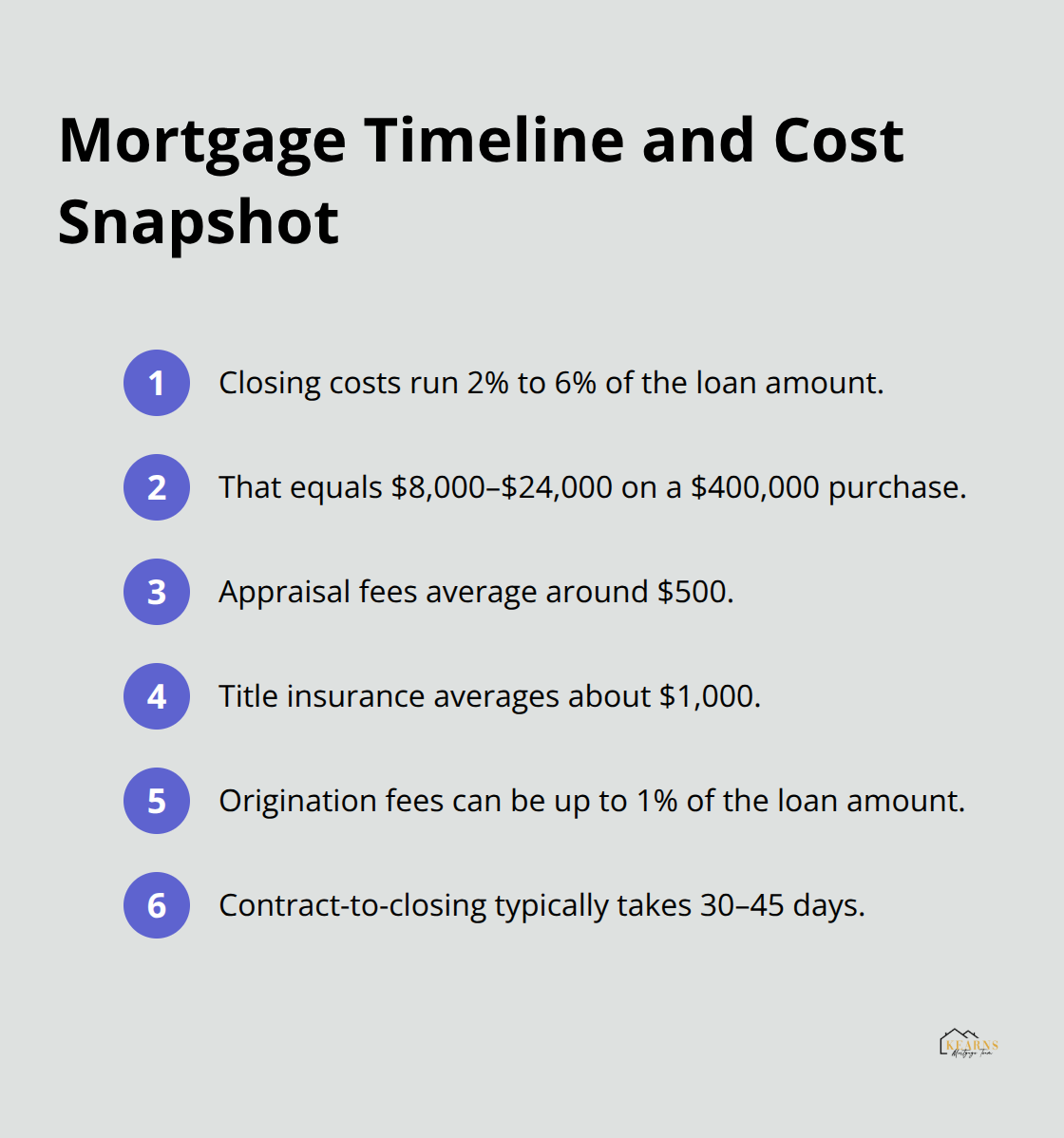

Closing costs run from 2% to 6% of the loan amount, which translates to $8,000-$24,000 on a $400,000 purchase according to current market data. These include appraisal fees (around $500), title insurance (averaging $1,000), and origination fees up to 1% of your loan amount. The entire process from contract to closing typically takes 30-45 days, though cash purchases close in 14-21 days.

Veterans should explore VA loan options early in the process to maximize their benefits.

Schedule Your Home Inspection

Schedule your home inspection within 7-10 days of contract acceptance to maintain your contingency timeline and negotiate repairs before your inspection period expires. This step protects you from costly surprises and gives you leverage in final negotiations. Even experienced buyers make mistakes during this phase that cost them thousands later.

What Mistakes Cost First-Time Buyers the Most

First-time buyers lose thousands of dollars through three predictable mistakes that experienced buyers avoid. These errors drain bank accounts and create stress that lasts for years.

Skip the Home Inspection at Your Own Risk

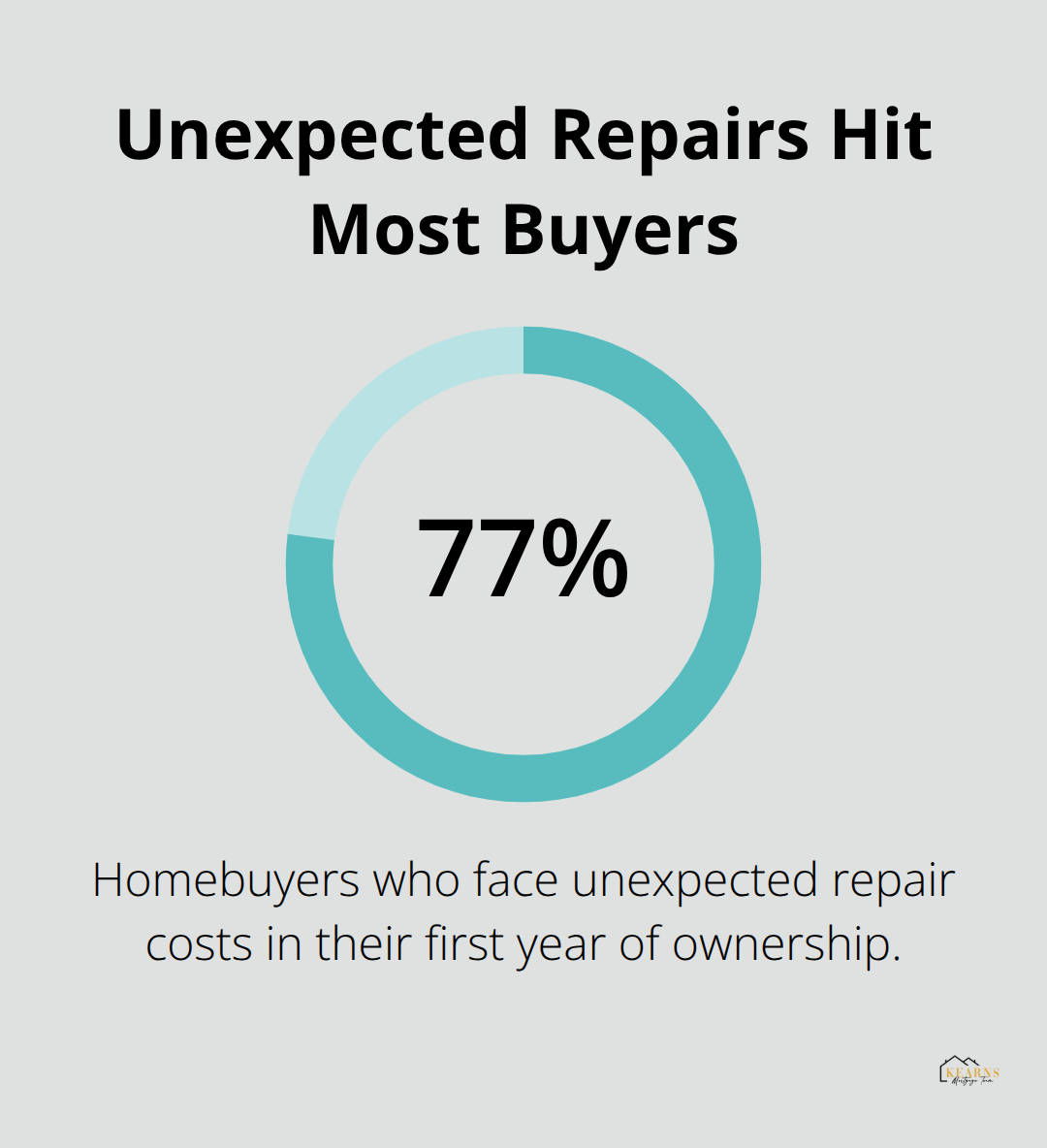

Home inspection mistakes rank as the costliest error new buyers make. Major issues like foundation problems or HVAC failures cost $15,000 to $50,000 after you close on the property.

77% of homebuyers face unexpected repair costs in their first year of ownership.

Home inspections cost $300 to $500 but identify problems that sellers must fix or credit back to you before you close. Professional inspectors examine electrical systems, plumbing, roofing, and structural elements that untrained eyes miss completely.

Hidden Homeownership Costs Destroy Budgets

Property taxes, homeowners insurance, and maintenance expenses add 1% to 3% of your home value annually beyond your mortgage payment. A $400,000 home generates $4,000 to $12,000 in additional yearly costs that renters never face.

Property taxes vary dramatically by location. Texas averages 1.69% while Hawaii averages just 0.31% according to Tax Foundation data. Homeowners insurance runs $1,200 to $3,000 annually (depending on your location and coverage levels). Set aside 1% of your home value each year for maintenance and repairs, which means $4,000 annually on that $400,000 purchase.

Emotional Decisions Lead to Financial Regret

Love at first sight with a house that stretches your budget creates years of financial stress and limits your other life choices. Buyers who exceed the 28% housing payment rule report significantly higher stress levels and lower satisfaction with their purchase according to recent housing studies.

Competition drives emotional bidding wars, but you win an overpriced home that means starting with negative equity when market conditions shift. Stick to your pre-approved budget regardless of how perfect a property seems. Perfect homes at wrong prices become financial nightmares that take years to escape.

Final Thoughts

Your path to homeownership becomes manageable when you follow proven first-time home buyer tips and advice. Calculate your debt-to-income ratio, save strategically for your down payment, and get pre-approved before house hunting. Avoid emotional decisions that stretch your budget beyond the 28% housing payment rule.

We at Kearns Mortgage Team provide personalized guidance through every step of your home purchase. Our loan officers help you compare Conventional, VA, FHA, USDA, and Non-QM loan options that match your financial situation. Professional mortgage guidance makes the difference between a smooth transaction and costly mistakes (especially for first-time buyers who face unfamiliar processes).

Start your homeownership journey by reviewing your credit report and calculating your true affordability. Connect with trusted mortgage professionals who understand your goals and can guide you through the process. The right preparation today creates the foundation for years of homeownership satisfaction.

What financial goal will you tackle first to move closer to your dream home?