Buying a home in Florida involves multiple steps, from getting your finances in order to signing the final paperwork. The home buying process in Florida can feel overwhelming if you don’t know what to expect at each stage.

We at Kearns Mortgage Team have guided countless buyers through this journey, and we’ve seen how much clarity helps. This guide walks you through every phase so you can move forward with confidence.

Getting Your Finances Ready

Your credit score is the first thing lenders examine, and Florida Housing programs require a minimum of 640. If you’re below that, focus on paying down existing balances and fixing any errors on your credit report before applying. Check your score for free through annual credit reports at AnnualCreditReport.com. Even a 20-point improvement can lower your interest rate and save thousands over the life of your loan. Pay all bills on time for at least three to six months before applying, as lenders weight recent payment history heavily. Avoid opening new credit accounts or making large purchases during this period, since these actions trigger hard inquiries that temporarily lower your score.

How Much Do You Actually Need to Save

Down payment assistance programs in Florida significantly reduce what you need upfront. Florida Assist provides up to $10,000 for down payment and closing costs as a 0% interest deferred second mortgage-you only repay it when you sell, refinance, or transfer the property. The Florida HLP Second Mortgage offers $12,500 at 3% interest amortized over 30 years. These programs must pair with a Florida Housing first mortgage, so they’re worth exploring if you qualify.

Beyond assistance programs, closing costs in Florida typically range from 2% to 5% of your home price. A mortgage application fee runs $1,000–$1,500. Total closing costs often reach 2–5% of your loan amount, so calculate this carefully into your savings plan.

Pre-Approval Separates Serious Buyers from Casual Ones

Pre-approval isn’t just helpful-it’s essential in competitive Florida markets. A pre-approval letter shows sellers you’re a qualified buyer with verified income and assets, not someone who might lose financing at the last minute. The process takes a lender three to five business days and involves submitting recent pay stubs, tax returns, and bank statements. Once approved, you know your exact budget and can search with confidence. Kearns Mortgage Team offers free consultations to discuss which loan options work best for your situation, whether that’s Conventional, FHA, VA, USDA, or other products tailored to your financial profile.

With your finances in order and pre-approval in hand, you’re ready to find the right property and make a competitive offer.

Finding the Right Property and Making an Offer

Work with a Real Estate Agent Who Knows Florida Markets

A real estate agent familiar with Florida’s market dynamics becomes your most valuable asset during the search phase. Your agent accesses the Multiple Listing Service and understands local inventory trends-Florida saw 1.2 million home sales in 2024 according to the Florida Association of Realtors, and knowing where that activity concentrates helps you position competitive offers. Ask your agent about days-on-market for comparable properties in your target neighborhood; homes selling in 20 days versus 60 days tell you whether you’re in a buyer’s or seller’s market. Your agent also handles critical negotiations around closing cost splits-in Florida, seller-paid broker commissions vary, and your agent advocates for favorable terms.

Research Neighborhoods and Property Values Thoroughly

When evaluating neighborhoods, pull property tax records and HOA fees before making an offer; a $350,000 home in one county might carry a $3,000 annual tax bill while an identical home elsewhere costs $4,500. Research flood zones using FEMA’s flood map tool and check your county’s property appraiser website for recent comparable sales. Properties in high-risk flood zones require flood insurance, which adds to your annual costs depending on location and coverage.

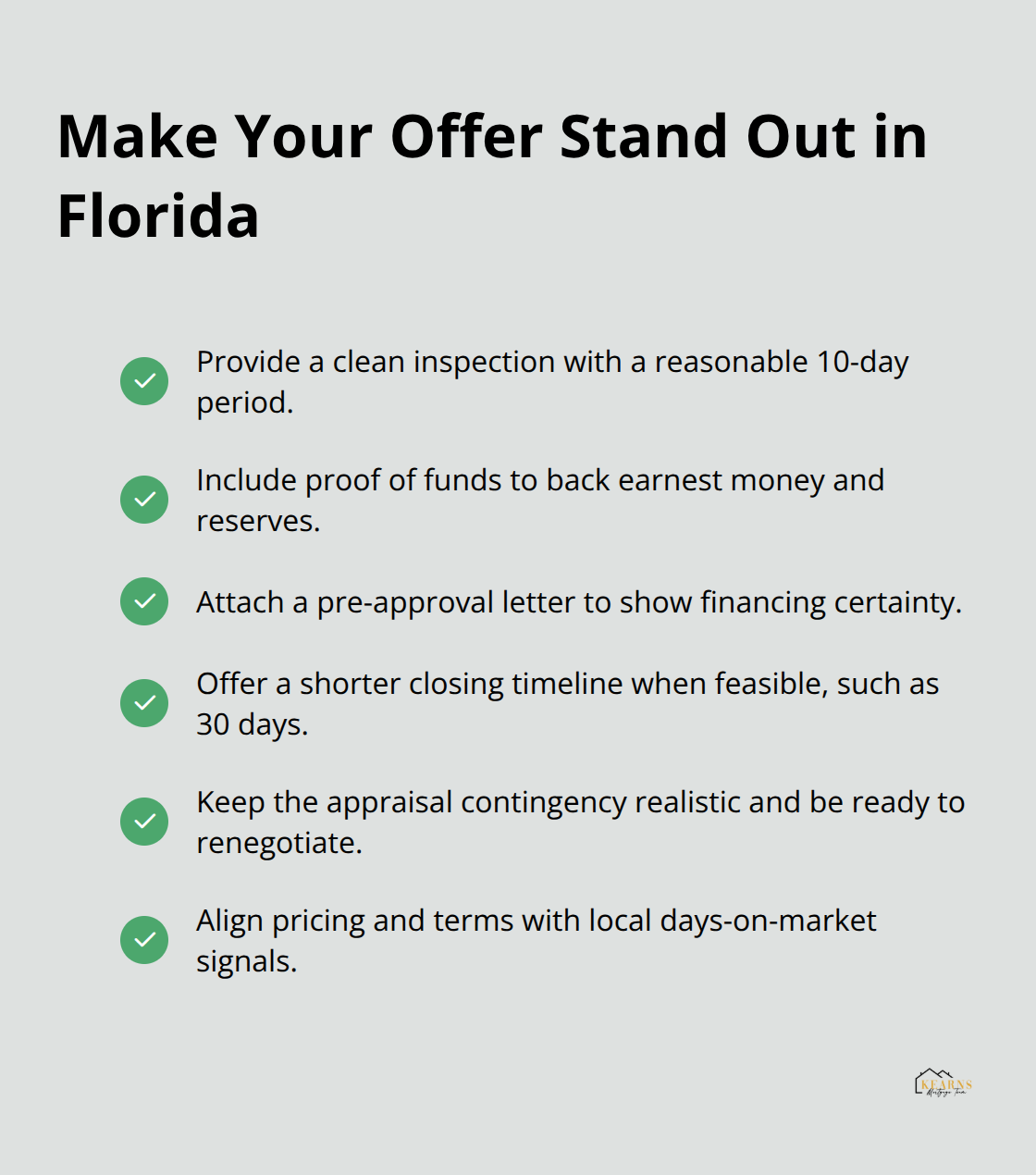

Submit a Competitive Offer That Stands Out

Submitting a competitive offer requires understanding what sellers actually want, not just offering the highest price. In strong markets, sellers respond to clean inspections, proof of funds, and short closing timelines just as much as to price. Include a pre-approval letter with your offer to demonstrate financing certainty-lenders require appraisals that validate your offer price, and a low appraisal kills deals at closing. Request a 10-day inspection period, which is standard in Florida and gives you time to hire a qualified home inspector and identify any structural or mechanical issues before committing.

Negotiate Key Terms and Contingencies

Negotiate the appraisal contingency carefully; if the property appraises low, you’ll need extra cash or a renegotiated price. When closing dates matter, offering a 30-day close instead of 45 days can make your offer stand out, though you should confirm your lender can meet that timeline. Once your offer gets accepted, the inspection, appraisal, and closing process begins-and this phase determines whether your purchase actually reaches the finish line.

The Inspection, Appraisal, and Closing Process

Schedule and Attend Your Home Inspection

Your home inspection surfaces problems before you’re legally bound to the purchase. Schedule the inspection within 10 days of your offer acceptance, which gives you time to hire a qualified inspector without rushing. Florida home inspectors must be licensed, so verify credentials through the Florida Department of Business and Professional Regulation before booking. Attend the inspection yourself-this isn’t something to skip. Walk through with the inspector, ask about foundation cracks, roof condition, HVAC systems, plumbing, and electrical wiring. Bring a notebook and document anything the inspector flags as needing repair.

A thorough inspection typically costs a few hundred dollars and you pay this upfront. If major issues emerge-say, a roof needing replacement in five years or a failing water heater-you have leverage to renegotiate price or request repairs before closing. Some issues require specialists beyond the standard inspection, like septic system evaluations or buried oil tanks, so budget for those if they apply to your property.

Understand the Appraisal and Title Search

The appraisal happens simultaneously and your lender orders it, not you. The appraiser determines whether the property’s value supports your offer price; if it appraises low, you’ll need to cover the difference in cash or renegotiate with the seller. This is why a strong offer with realistic pricing matters-low appraisals kill deals at closing.

The title search protects you by confirming the seller actually owns the property free of liens or claims. Your lender requires title insurance, which you typically pay for; costs vary by county but generally run under $1,000 for properties under $300,000. A closing attorney handles the final steps in Florida, which often reduces costs compared to states requiring two separate attorneys. The attorney prepares closing documents, verifies funds, and coordinates with your lender.

Know Your Closing Costs and Taxes

You’ll pay a settlement fee to the closing attorney, typically $300–$900 depending on your county. Florida also charges Documentary Stamp Tax and Nonrecurring Intangible Tax at closing, both paid by you. Budget for these taxes when calculating your final closing costs.

Review Documents Before the Final Closing Meeting

The final closing meeting brings together you, the seller, both agents, the closing attorney, and sometimes the lender representative. You’ll sign mortgage documents, the promissory note, and the closing disclosure, which itemizes every fee and cost. Review the closing disclosure at least three days before closing; federal law requires this timeline. If numbers don’t match your expectations, flag discrepancies immediately-don’t sign if something looks wrong.

Bring a valid ID and a cashier’s check or arrange a wire transfer for your down payment and closing costs. After signing, the attorney records the deed and mortgage with your county, and you receive the keys. Flood insurance is mandatory if your property is in a high-risk zone, so confirm your lender’s requirements before closing. Some buyers overlook this and scramble at the last minute. If you’re purchasing a condo, HOA fees and building costs apply and are typically disclosed before closing. Once all documents are signed and funds transfer, the home is officially yours.

Final Thoughts

The home buying process in Florida moves through distinct phases, each with its own timeline and requirements. From checking your credit score and securing pre-approval through scheduling inspections and closing on your keys, you’ve now seen how these pieces fit together. The entire journey typically spans 30 to 45 days once your offer gets accepted, though this varies based on your lender’s speed and any complications that surface during the appraisal or title search. Common mistakes derail buyers at predictable moments: applying for new credit or making large purchases after pre-approval tanks your debt-to-income ratio and can kill your loan approval, skipping the home inspection to save a few hundred dollars costs thousands when hidden problems emerge after closing, and underestimating closing costs leaves buyers scrambling for cash at the final walkthrough.

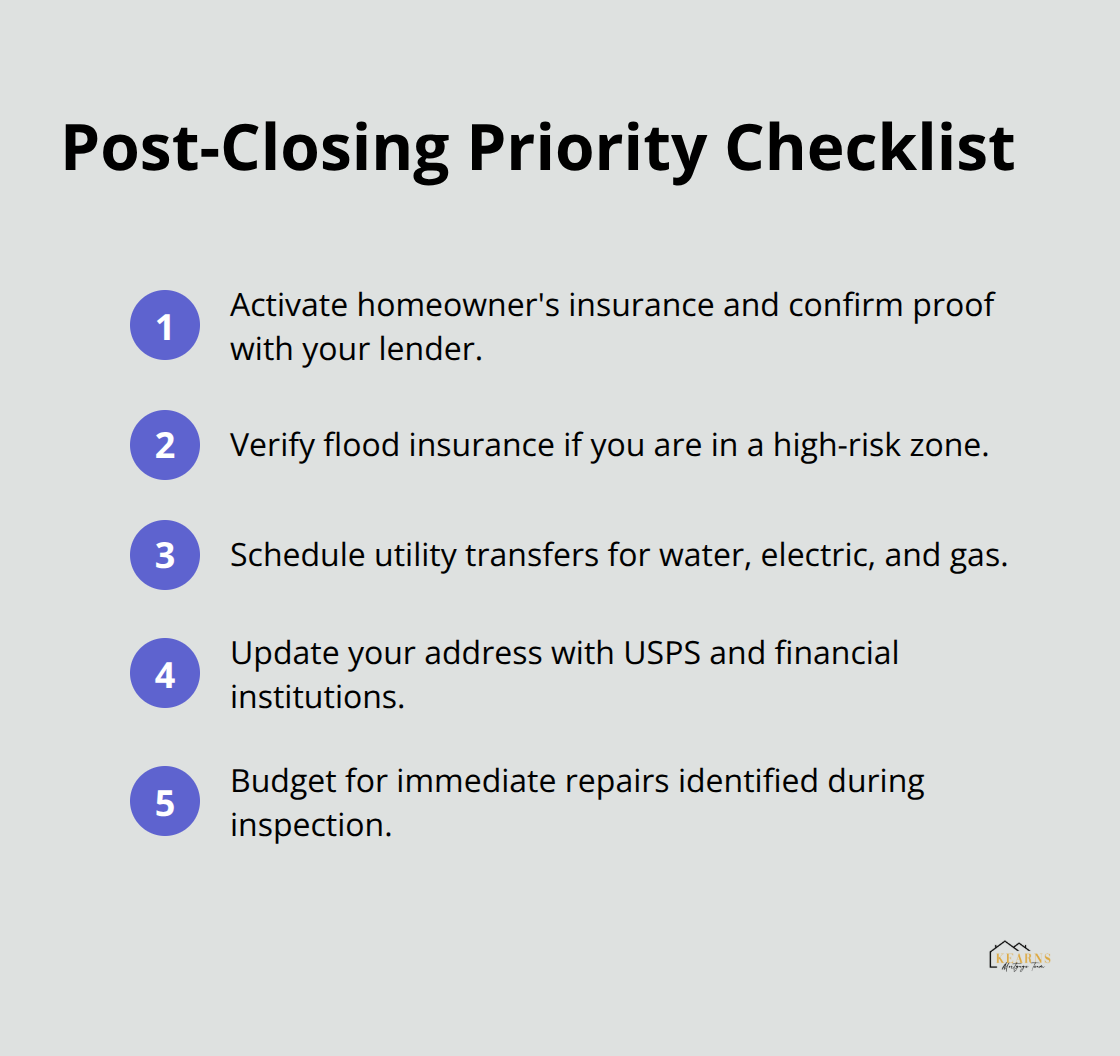

After closing, your first priority is setting up homeowner’s insurance if you haven’t already, since your lender requires proof before funding the loan. If your property sits in a high-risk flood zone, flood insurance becomes mandatory and non-negotiable. Schedule utility transfers for water, electric, and gas to activate on your closing date, update your address with the post office and financial institutions, and budget for immediate repairs identified during inspection.

The home buying process in Florida doesn’t end at closing-homeownership brings ongoing responsibilities, from property tax payments to HOA fees if applicable. Many buyers benefit from working with a trusted mortgage partner who understands Florida’s unique requirements and can answer questions that arise after purchase. Kearns Mortgage Team offers personalized guidance to help you navigate homeownership with confidence.