Florida’s housing market is shifting in 2025, and understanding what’s ahead matters for anyone buying or investing in the state. Interest rates, population growth, and inventory levels are all moving in ways that will reshape affordability and opportunity. We at Kearns Mortgage Team have analyzed the key trends to help you navigate what’s coming.

Whether you’re a first-time buyer or seasoned investor, the decisions you make now will determine your success in this changing market.

What’s Driving Florida’s Housing Market in 2025

Interest Rates Create New Opportunities for Buyers

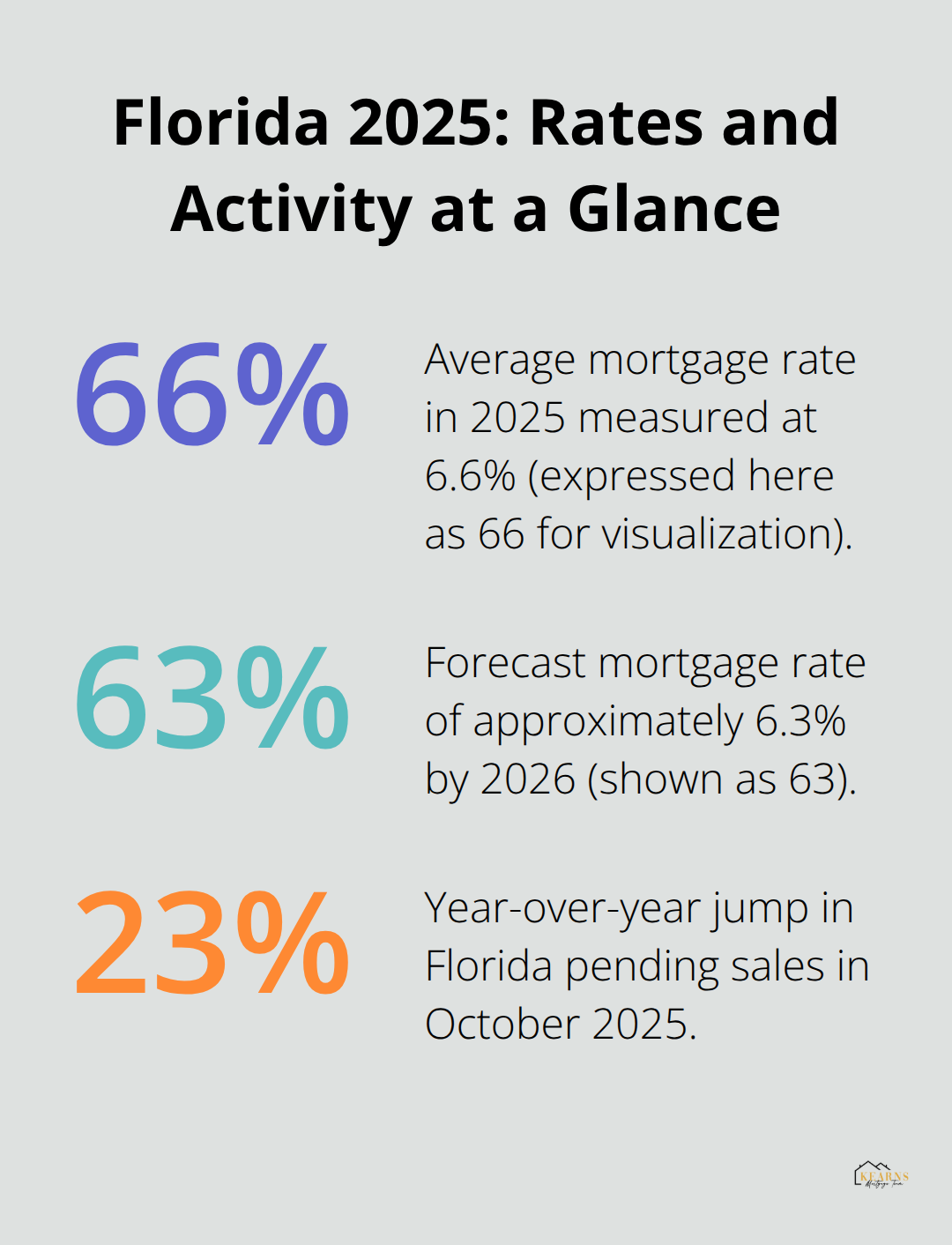

Interest rates are falling faster than most expected, and that shift is reshaping Florida’s entire housing landscape. Mortgage rates averaged around 6.6% through 2025 but are forecast to ease to approximately 6.3% by 2026.

This matters because a single percentage point drop in rates expands the eligible buyer pool by roughly 5.5 million people nationally, with first-time buyers benefiting most. For perspective, a $500,000 home with 10% down costs about $3,895 monthly at 7% but only $3,672 at 6.25%-that’s $223 in monthly savings that suddenly makes homeownership achievable for thousands of Floridians.

Florida’s median sale price sits at $412,734, roughly 5.2% lower than the national median, which means rate relief hits harder here. The National Association of Realtors confirmed that Florida pending sales jumped 23% year-over-year in October 2025, a direct response to rates moving downward. Buyers who move quickly will have more negotiating power than they’ve had in years.

Population and International Investment Reshape Demand

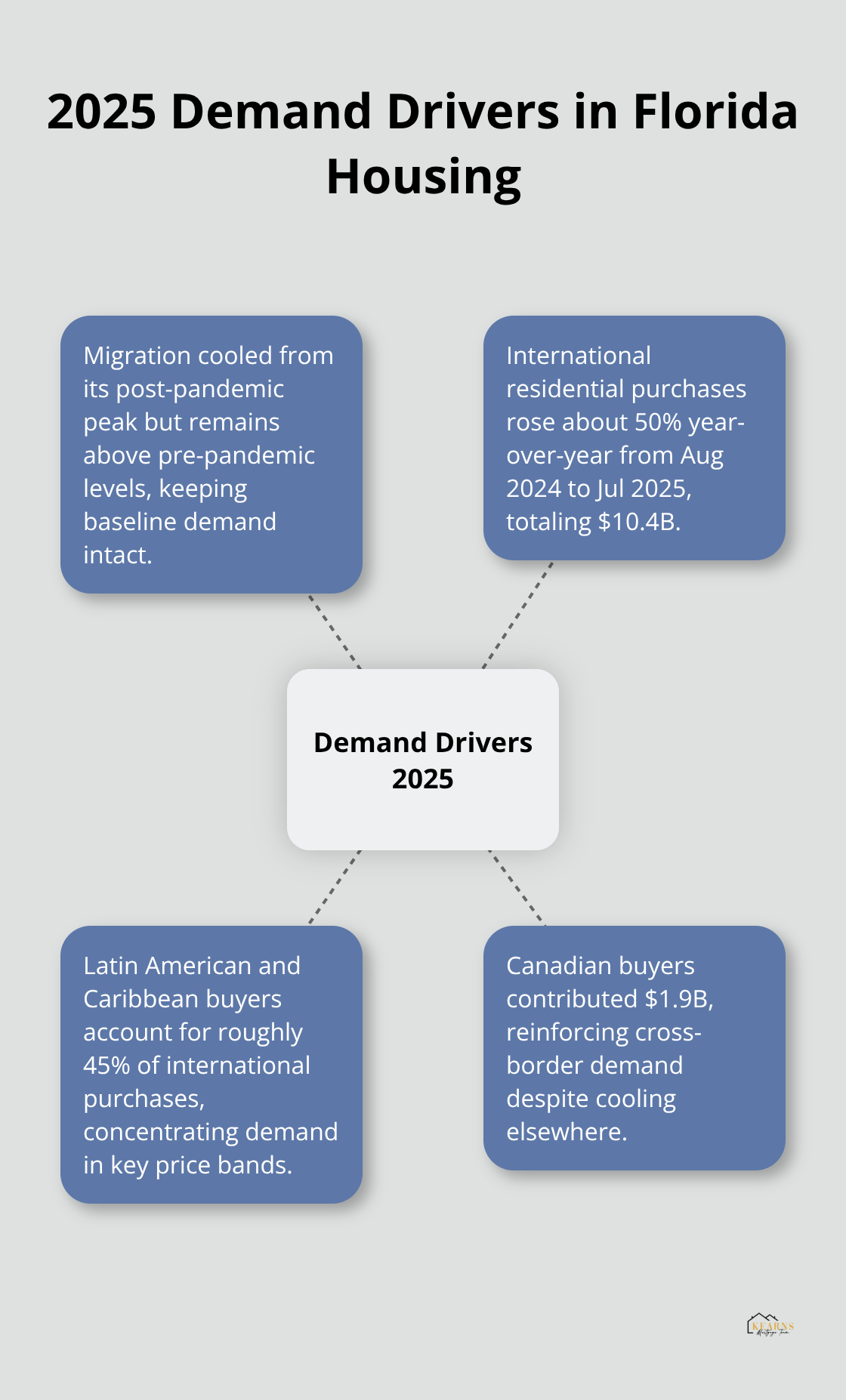

Population migration into Florida has cooled from its post-pandemic peak, but it remains above pre-pandemic levels, and falling rates could reignite that demand. International buyer activity already rebounded sharply, with Florida international residential purchases rising about 50% year-over-year from August 2024 to July 2025, bringing in $10.4 billion in dollar volume. Latin American and Caribbean buyers dominate this activity at roughly 45% of international purchases, with Canada contributing $1.9 billion alone.

Hidden Costs Offset Rate Relief

Affordability pressures remain real despite lower rates. Homeowners insurance premiums surged roughly 54% from 2019 to 2024, and property taxes continue climbing-these costs offset some of the relief lower mortgage rates provide. Inflation and cost-of-living pressures cool demand in some segments, but Realtor.com projects nominal home prices will rise only about 2.0% in 2025, with real prices actually dipping when adjusted for inflation. This conservative growth means Florida isn’t a speculative market right now; it’s a practical one.

Employment and Financial Readiness Drive Success

Employment growth remains steady across Florida metros, particularly in Tampa, Orlando, and Jacksonville, supporting sustained buyer interest despite affordability headwinds. The reality is that 2025 favors buyers who are financially ready-those with minimal debt, solid emergency reserves, and down payment savings will find more inventory and better terms than they would have in 2024. Your financial position matters more than market timing in this environment.

What Florida’s Housing Market Will Look Like in 2025

Regional Price Movements Tell an Uneven Story

Orlando’s median sale price reached $445,000 in Q1 2025, up 2.3% from the prior year, while Tampa held steady at $400,000 with a slight 1.3% decline, and Jacksonville remained flat at $390,000 year-over-year according to Florida Realtors data. This divergence signals that not all Florida metros will perform equally-Orlando’s job growth in tech and healthcare drives price appreciation, while Tampa and Jacksonville face softer demand despite strong employment fundamentals. In Florida’s eight largest metro areas, median sales prices for existing homes and condos are projected to fall an average of 1.9% in 2026, meaning sellers banking on rapid equity gains will face disappointment. The real story is that appreciation will be glacial, which actually favors buyers who can lock in payments now before rates stabilize.

International buyers are clustering in the $250,000 to $500,000 price band, with the median price for international purchases sitting at $442,000 in 2025, down from $469,000 in 2024. This shift suggests that high-end properties above $750,000 may face longer selling timelines and potential price pressure, while the mid-market remains relatively resilient.

Inventory Expansion Shifts Competitive Dynamics

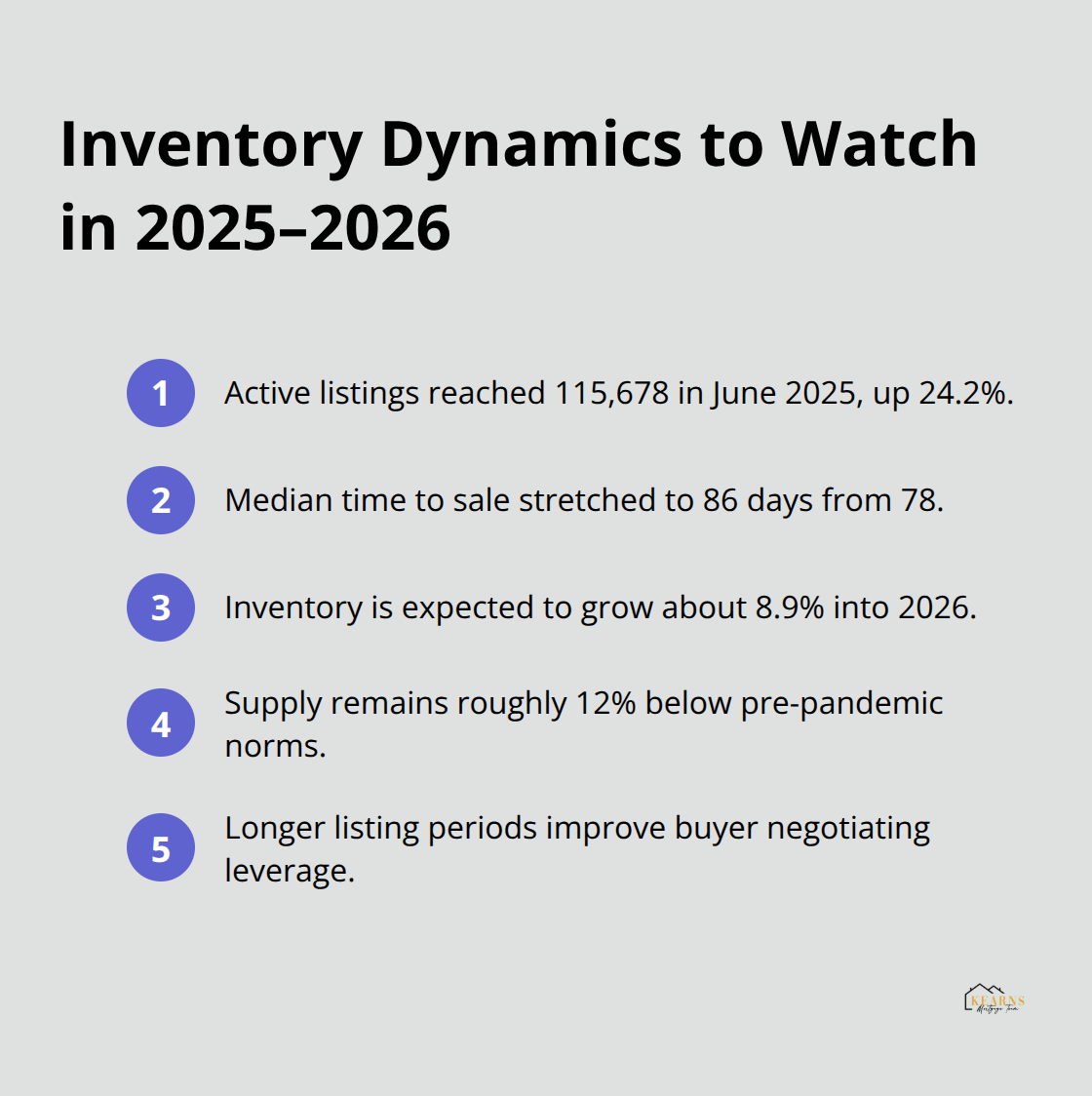

Florida active listings reached 115,678 in June 2025, a 24.2% increase from 93,105 in June 2024, but this growth came because homes took longer to sell rather than from a flood of new listings-the median time to sale stretched to 86 days from 78 days just one year prior. This matters because longer listing periods give you negotiating leverage you didn’t have in 2024. Inventory will grow approximately 8.9% heading into 2026, though it will remain roughly 12% below pre-pandemic norms, meaning supply constraints persist but are loosening.

Closed sales in Florida climbed 2.8% year-over-year to 23,827 in June 2025, confirming that falling rates are pulling buyers back into the market. For investors, this environment rewards disciplined property selection-focus on properties in employment-strong metros like Orlando and Tampa where rental demand remains solid, and avoid overpriced inventory that has been sitting more than 100 days.

Pricing Strategies Must Adapt to Market Conditions

The shift from a seller’s market to a balanced market means pricing strategies that worked in 2023 will fail in 2025. Properties priced aggressively above comparable sales will languish, while those positioned competitively will move within 60 to 75 days. Sellers who understand this dynamic and adjust their expectations accordingly will find success; those who cling to 2024 pricing will watch their homes accumulate days on market.

The data reveals that Florida’s housing market in 2025 operates on fundamentals rather than momentum. Rate relief, inventory growth, and regional employment patterns create distinct opportunities for different buyer profiles. Your next move depends on understanding where you fit in this landscape and what your financial position allows.

How to Position Yourself for Success in 2025’s Shifting Market

Build Financial Strength Before You Apply

The 2025 Florida market rewards preparation over timing. First-time buyers who arrive debt-free with a 3–6 month emergency fund and 5–10% down payment will qualify for better terms and have real negotiating power, while those stretching financially will face rejection or unfavorable rates. The difference between approval and denial often comes down to financial readiness months before you make an offer. Start now by calculating your debt-to-income ratio and checking your credit report; a 50-point credit improvement can lower your rate by 0.5%, saving tens of thousands over the loan term. If you carry high-interest debt, paying it down before applying costs less than paying a higher mortgage rate for 30 years. The median time to sale in Florida stretched to 86 days in June 2025, which gives you breathing room to prepare properly instead of rushing into a purchase.

Evaluate Your Credit and Debt Position

Your credit score and debt levels directly impact the rates you’ll receive. Lenders scrutinize debt-to-income ratios closely in 2025, and a ratio above 43% will limit your options significantly. Pull your credit report from all three bureaus and dispute any errors immediately; this step alone can take weeks but yields substantial rate improvements. High-interest credit card balances and personal loans should be paid down aggressively before you apply for a mortgage. The cost of carrying that debt into your mortgage term far exceeds the effort of eliminating it now.

Invest in Properties Where Rental Demand Holds Strong

Investment properties demand sharper analysis in 2025 than they did in 2024. The rental market in Florida shows modest rent declines expected in 2026 as new multifamily supply comes online, particularly in growth metros like Orlando and Tampa where employment remains strong. Try properties in the $250,000 to $500,000 range where international buyer demand clusters and local rental yields remain solid; high-end properties above $750,000 face longer selling timelines and potential price pressure. Calculate your cash-on-cash return before making an offer, and avoid properties sitting over 100 days unless the price reflects that reality.

Time Your Entry Around Rate Movements and Property Selection

Market entry timing matters less than property selection in this environment. Lower mortgage rates make acquisition costs more favorable now, but you will compete with fewer buyers if you wait 60–90 days for rates to stabilize further around 6.3% as forecast for 2026. The real advantage goes to investors who identify underpriced properties in employment-strong areas and lock in rates before the next wave of buyer activity arrives. Properties in Orlando and Tampa offer the strongest fundamentals, with steady job growth supporting tenant demand and price stability.

Final Thoughts

Florida’s housing market predictions for 2025 point to a market shaped by falling rates, expanding inventory, and regional variation rather than broad appreciation. The shift from 2024’s tight conditions to 2025’s balanced environment creates real opportunities for buyers who prepare financially and investors who select properties strategically. Rates moving toward 6.3% by 2026 will continue pulling buyers back into the market, but that window of advantage closes as competition increases.

Your preparation matters more than market timing in this environment. Start by eliminating high-interest debt and building your emergency fund to three to six months of expenses, then check your credit report for errors and work to improve your score before applying for a mortgage. If you’re an investor, focus on properties in employment-strong metros where rental demand supports cash flow, and avoid overpriced inventory sitting beyond 100 days.

The path forward requires honest assessment of your financial position and clear goals about what you want from homeownership. We at Kearns Mortgage Team understand that navigating this market involves more than just finding a property-our team offers personalized mortgage solutions across Conventional, VA, FHA, USDA, and Non-QM options to match your specific situation. Contact Kearns Mortgage Team to discuss your options and create a financing strategy that works for your goals.