Real estate investing doesn’t require a massive bank account or wealthy connections. Many successful investors started with minimal capital by using smart financing strategies and creative approaches.

We at Kearns Mortgage Team see first-time investors build wealth through house hacking, REITs, and partnership deals. Learning how to start investing in real estate with little money opens doors to financial freedom that seemed impossible just months earlier.

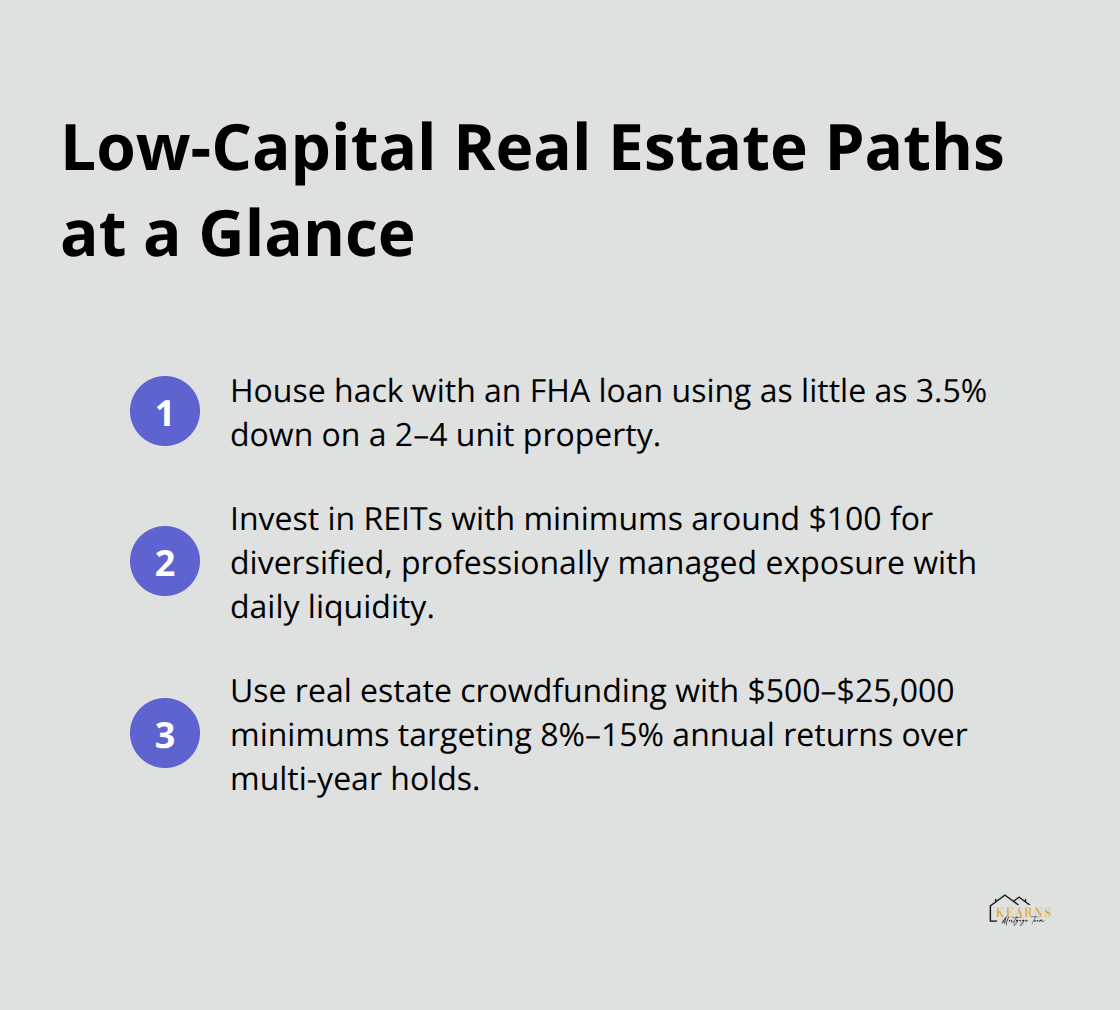

What Investment Options Work With Minimal Capital?

House Hacking Through FHA Loans

House hacking transforms your primary residence into an income-producing asset while you need just 3.5% down with an FHA loan. You purchase a duplex, triplex, or four-unit property, live in one unit, and rent the others to cover your mortgage payments. The Federal Housing Administration allows this strategy because you occupy the property as your primary residence for at least one year.

Properties with two to four units typically generate $800 to $2,500 monthly rental income per unit (depending on location and market conditions). This approach often reduces your housing costs to zero or creates positive cash flow from day one. You build equity in the property while tenants pay down your mortgage balance.

REITs Offer Professional Management Without Property Ownership

Real Estate Investment Trusts provide immediate access to diversified real estate portfolios with investments that start at just $100 through most brokerages. According to the National Association of Real Estate Investment Trusts, nearly 170 million Americans own REITs through retirement accounts and brokerage platforms.

Equity REITs own income-producing properties and typically pay dividends of 3% to 8% annually, while mortgage REITs finance real estate deals and often yield 8% to 12%. Public REITs trade like stocks with daily liquidity, which makes them perfect for beginners who want real estate exposure without property management responsibilities.

Crowdfunding Platforms Lower Entry Barriers

Real estate crowdfunding platforms allow investments in commercial properties and development projects with minimums that range from $500 to $25,000. Platforms like Fundrise and RealtyMogul pool investor funds to purchase properties that individual investors couldn’t afford alone. These platforms typically target annual returns between 8% and 15%, though investments often require three to seven-year commitments.

Crowdfunding works best for investors who want higher potential returns than REITs but can accept reduced liquidity and higher risk profiles. These alternative approaches work well when traditional bank loans prove difficult to obtain or when you want to explore creative financing solutions like refinancing.

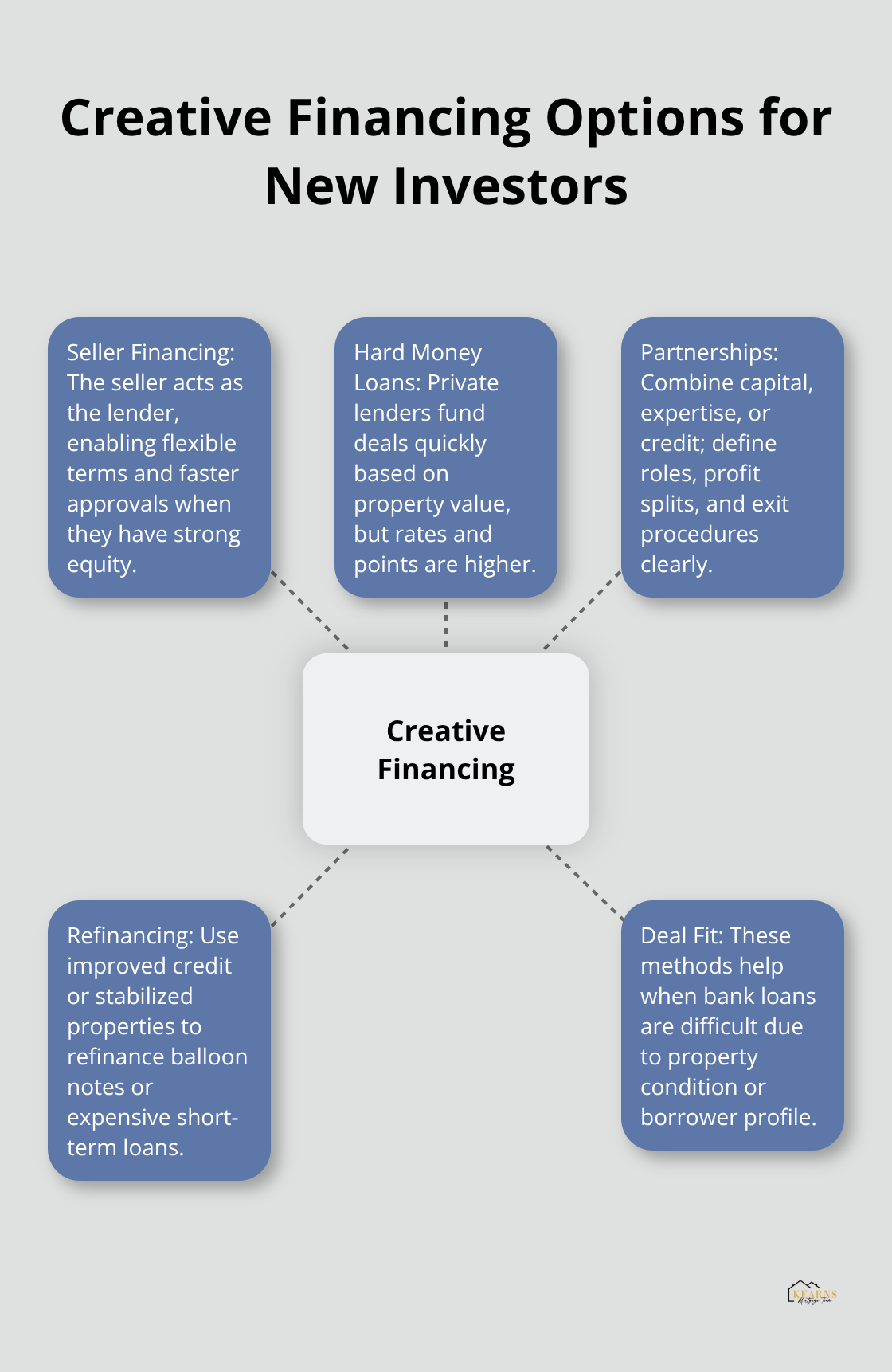

What Creative Financing Options Work for New Investors

Seller Financing Opens Doors Without Bank Approval

Seller financing allows property owners to act as the bank, where buyers make monthly payments to the seller instead of using a traditional mortgage from a lender. This strategy works particularly well when sellers own properties outright or have substantial equity built up over decades. Sellers benefit from steady monthly income streams and often negotiate above-market prices to compensate for flexible terms, while buyers avoid strict lending requirements and lengthy approval processes.

The typical seller financing deal involves down payments with interest rates that vary depending on current market conditions and negotiation skills. Balloon payments usually come due within three to seven years, which gives buyers time to improve credit scores or secure traditional refinancing. This approach works best in markets where sellers struggle to find qualified buyers or properties need significant repairs that prevent conventional lending.

Hard Money Lenders Provide Speed Over Savings

Hard money lenders focus on property value rather than borrower creditworthiness and can close deals within seven to fourteen days compared to traditional lenders that require thirty to forty-five days. These private lenders typically charge high annual interest rates plus points upfront, which makes them expensive but valuable for time-sensitive opportunities like foreclosure auctions or fix-and-flip projects.

Hard money lenders typically offer loans based on a 60% to 75% loan-to-value ratio, which requires substantial down payments but allows investors to secure properties that banks won’t finance due to condition issues. The average hard money loan term runs six to twelve months, perfect for investors who plan quick renovations and resales but dangerous for those without solid exit strategies or adequate cash reserves.

Partnerships Multiply Your Buying Power

Investment partnerships combine complementary strengths where one person provides capital while another contributes time, expertise, or credit qualifications. Joint venture agreements typically split profits 50-50 when both partners contribute equally valuable resources, though ratios adjust based on actual contributions and risk levels that each party assumes.

Successful partnerships often pair experienced investors with newcomers who bring fresh energy and additional financing capacity. Clear partnership agreements prevent disputes when they define responsibilities, profit distributions, and exit procedures before partners purchase any properties together.

These creative financing strategies require careful planning and solid financial foundations to succeed long-term.

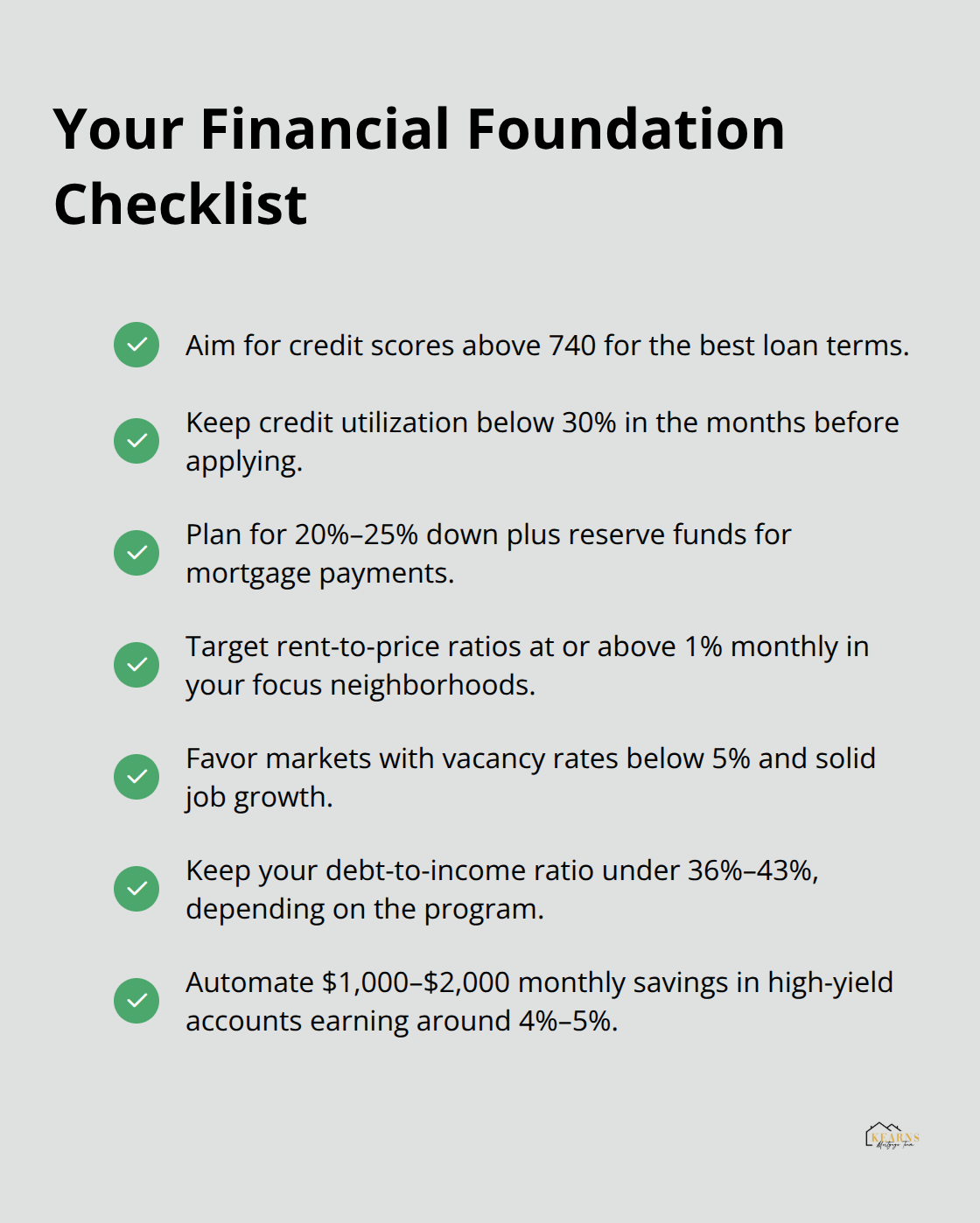

What Financial Foundation Do You Need Before Investing

Credit Score Optimization

Your credit score directly impacts every real estate investment opportunity, with scores above 740 securing the lowest interest rates and best loan terms from traditional lenders. Experian data shows that borrowers with credit scores between 620 and 639 pay approximately 1.5% higher interest rates than those with excellent credit, which translates to thousands in additional costs over a 30-year mortgage. Focus on paying down credit card balances below 30% utilization, dispute any errors on your credit reports, and avoid new credit inquiries for six months before you apply for investment property loans.

Emergency Reserves and Down Payment Strategy

Investment properties require larger cash reserves than primary residences, with most lenders demanding 20% to 25% down payments plus reserve accounts for mortgage payments. The median home price exceeded $510,000 by mid-2025 according to the U.S. Census Bureau, which means investors need $102,000 to $127,500 in down payment funds alone for average-priced properties. Smart investors automate savings transfers of $1,000 to $2,000 monthly into high-yield savings accounts that earn 4% to 5% annually while they build their investment war chest.

Market Research Drives Profitable Decisions

Successful investors study specific neighborhoods rather than broad metropolitan areas, focusing on rent-to-price ratios above 1% monthly and vacancy rates below 5% annually. Properties in areas with job growth above 2% annually and population increases typically appreciate faster and maintain stronger rental demand. Use rental listing websites to calculate average rents per square foot, then compare those figures against property purchase prices to identify markets where cash flow makes sense from day one rather than hoping for future appreciation.

Debt-to-Income Ratio Management

Lenders scrutinize your debt-to-income ratio more strictly for investment properties than primary residences (typically requiring ratios below 36% to 43% depending on the loan program). Calculate your total monthly debt payments including credit cards, student loans, and existing mortgages, then divide that figure by your gross monthly income. Pay off high-interest consumer debt first, then consider increasing your income through side hustles or career advancement before you pursue investment property loans.

Final Thoughts

Real estate investment with limited capital becomes achievable when you combine smart strategies with solid preparation. House hacking through FHA loans needs just 3.5% down while it produces rental income immediately. REITs offer instant diversification with $100 minimum investments, and crowdfunding platforms provide access to commercial properties with $500 entry points.

Creative financing through seller financing, hard money lenders, and strategic partnerships expands your options beyond traditional bank loans. Strong credit scores, adequate cash reserves, and thorough market research create the foundation for investment success. These approaches show you how to start investing in real estate with little money when you apply them systematically.

We at Kearns Mortgage Team help investors navigate complex financing options for investment properties (including FHA, VA, and conventional loans). Our team provides personalized mortgage solutions and free consultations to support your investment goals. Contact Kearns Mortgage Team to explore which financing strategy works best for your situation.

What investment approach feels most realistic for your current financial situation and risk tolerance?