Mortgage rates fluctuate constantly, and homeowners often wonder when refinancing makes financial sense. The answer depends on multiple factors beyond just interest rates.

We at Kearns Mortgage Team see three main scenarios that typically justify refinancing: significant rate drops, major life changes, and specific financial goals. Each situation requires careful analysis of costs versus benefits to determine the right timing.

When Interest Rates Drop Significantly

Interest rate drops create the most compelling refinance opportunities, but the magic number isn’t what most homeowners expect. The old rule that required a 2% rate reduction is outdated. Today’s market reality shows that a 0.5% to 1% reduction can generate substantial savings, especially with current refinance costs that average 2% to 5% of your loan amount according to recent industry data.

Rate Reduction of 0.5% or More Creates Savings

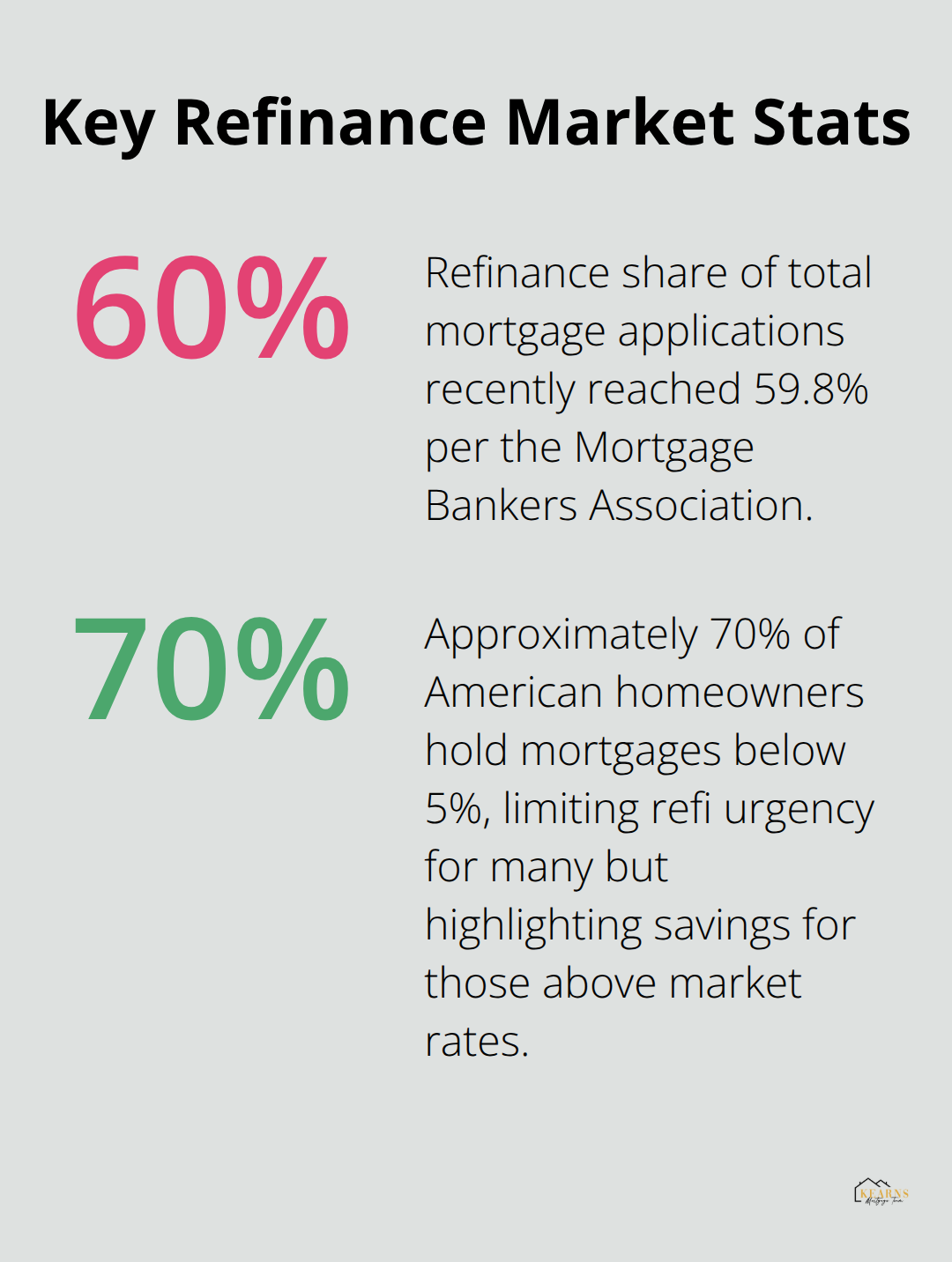

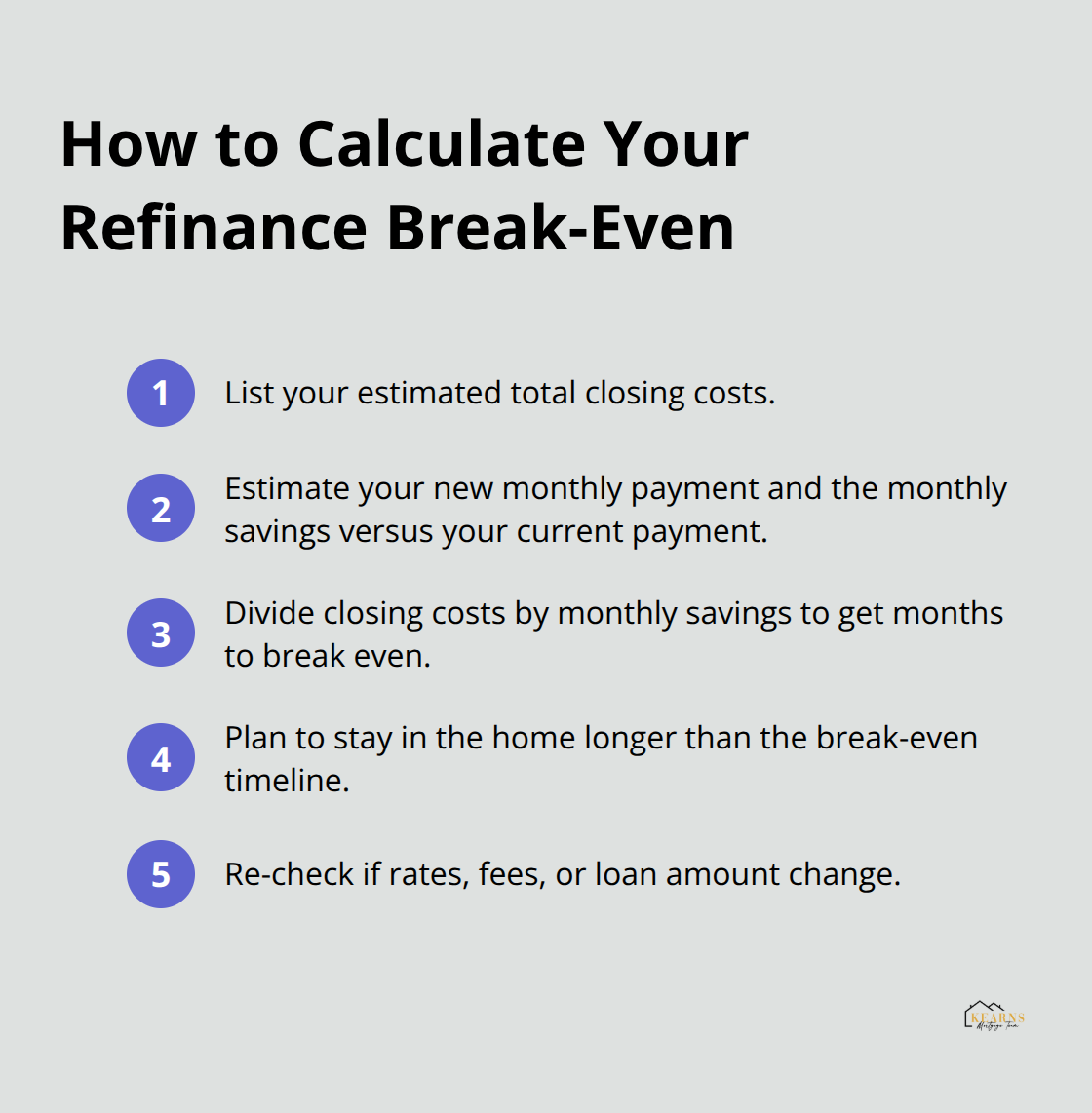

The break-even point determines whether refinance makes financial sense for your situation. With the national average 30-year fixed refinance rates tracked by the Federal Reserve, homeowners who pay rates significantly above current market levels should seriously consider refinance options. Most borrowers recover their closing costs within 24 to 36 months when they secure a 0.75% rate reduction. The Mortgage Bankers Association reports that refinance applications have increased substantially, with the refinance share reaching 59.8 percent of total applications.

Current Market Conditions and Rate Trends

Current market conditions show mortgage rates that hover above 6% with experts who predict they’ll remain elevated through 2025. This creates urgency for homeowners with rates above 7%. The Federal Reserve’s monetary policy directly influences these rates, which makes timing critical. Approximately 70% of American homeowners currently hold mortgages below 5%, but those with higher rates face significant savings potential.

Break-Even Point Analysis for Refinance Costs

Smart borrowers calculate monthly payment savings against total closing costs to determine their personal break-even timeline. Closing costs typically range from $3,000 to $6,000 for a $200,000 loan (depending on your location and lender fees). A homeowner who saves $200 monthly through refinance will recover these costs in 15 to 30 months. Rather than wait for perfect conditions, homeowners who secure favorable rates when available beat those who attempt to time the market perfectly.

These rate considerations work hand-in-hand with personal circumstances that can make refinance even more attractive.

Life Changes That Trigger Refinancing Opportunities

Personal financial improvements create powerful refinancing opportunities that often deliver better savings than waiting for perfect market conditions. Credit score improvements can reduce your mortgage rate, which translates to thousands in savings over your loan term. The Consumer Financial Protection Bureau shows that borrowers with scores above 740 qualify for the best available rates, while those between 620 and 679 face significantly higher costs.

Improved Credit Score Opens Better Rate Options

Recent credit score gains put you in position to secure rates previously unavailable to you. Lenders price mortgages in tiers, with dramatic rate drops at key credit thresholds. A borrower who improves from a 650 to 720 credit score can expect rate reductions of 0.5% to 1%, which creates immediate refinance value even without broader market rate changes. Pay down credit cards, eliminate collections, and correct credit report errors before you apply to maximize your rate potential.

Income Increases Allow Shorter Loan Terms

Higher income levels qualify you for 15-year mortgages that cut total interest costs dramatically while they build equity faster. A $300,000 mortgage at 6% costs $347,514 in total interest over 30 years versus $151,894 over 15 years. The monthly payment difference of approximately $800 becomes manageable with income increases of 20% or more. Debt-to-income ratios below 28% for housing expenses (including principal, interest, taxes, and insurance) position you for the most favorable terms.

Home Value Appreciation Eliminates PMI Requirements

Property appreciation that pushes your equity above 20% creates automatic savings through PMI elimination. PMI costs range from 0.3% to 1.5% of your original loan amount annually, which means $900 to $4,500 yearly on a $300,000 mortgage. Rising rates reduce sale probability and prevent transactions, which increases home prices and moves many homeowners past the 80% loan-to-value threshold required for PMI removal. An appraisal that costs $400 to $600 can confirm your equity position and potentially save thousands annually.

These personal financial improvements often align with specific goals that make refinance even more attractive for your situation.

Financial Goals That Support Refinancing Decisions

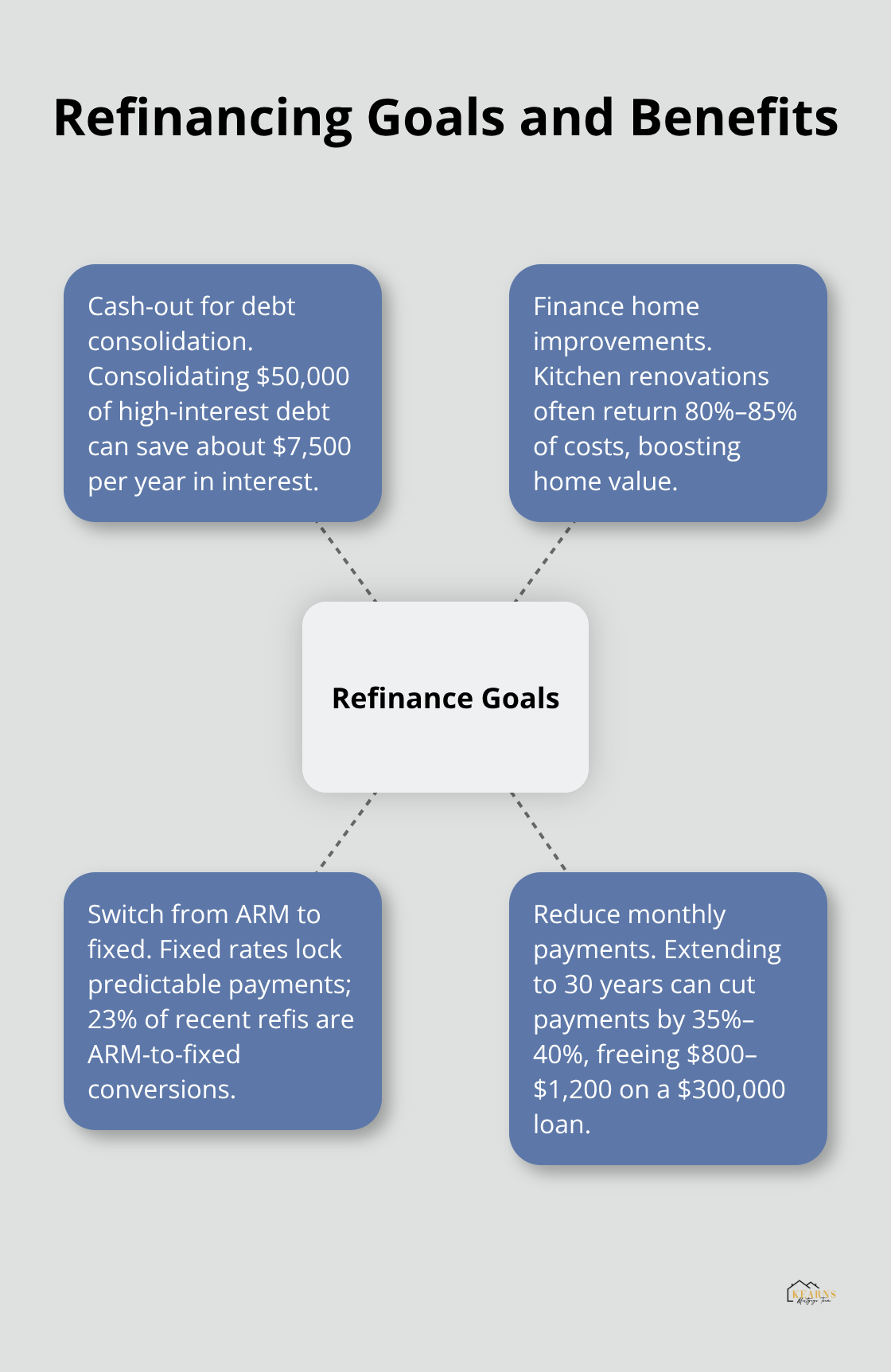

Specific financial objectives create compelling reasons to refinance beyond simple rate reductions. Cash-out refinance allows homeowners to access their equity at mortgage rates that remain significantly lower than credit cards or personal loans. Consumer credit increased at a seasonally adjusted annual rate of 2.7 percent during the third quarter, with revolving credit increasing at an annual rate of 2.0 percent, while cash-out refinance rates hover around 6.5% to 7%. Homeowners who consolidate $50,000 in high-interest debt through cash-out refinance save approximately $7,500 annually in interest payments.

Cash-Out Refinance for Home Improvements or Debt Consolidation

Home improvement projects funded through cash-out refinance also increase property values, with kitchen renovations typically returning 80% to 85% of investment costs according to Remodeling Magazine’s Cost vs. Value Report. This strategy works particularly well for homeowners who need substantial capital (typically $25,000 or more) and want to avoid high-interest personal loans or credit cards. The mortgage interest deduction on amounts up to $750,000 provides additional tax benefits that other debt consolidation methods cannot match.

Switching from Adjustable to Fixed-Rate Mortgages

Adjustable-rate mortgage holders face reset dates that can trigger payment increases of $300 to $800 monthly when rates adjust upward. ARM borrowers who secured initial rates below 4% now confront potential adjustments to 7% or higher as their teaser periods expire. Fixed-rate mortgages lock in predictable payments and protect against future rate volatility. The National Association of Realtors reports that 23% of recent refinance activity involves ARM-to-fixed conversions, with borrowers who prioritize payment stability over potential short-term savings.

Reducing Monthly Payments for Better Cash Flow

Homeowners who face temporary income reductions or increased expenses benefit from refinance to longer terms that reduce monthly obligations. Extension of a 15-year mortgage to 30 years typically cuts payments by 35% to 40%, which frees up $800 to $1,200 monthly for a $300,000 loan. This strategy works best for borrowers who plan to make additional principal payments when their financial situation improves, which avoids the total interest cost penalties of extended amortization schedules.

Final Thoughts

Rate reductions of 0.5% or more typically justify refinance costs, but personal circumstances often matter more than market conditions alone. Credit score improvements, income increases, and home value appreciation create opportunities that smart homeowners recognize and act upon. The question of when does refinance mortgage make sense requires careful evaluation of your complete financial picture.

The break-even analysis remains your most important calculation. Compare monthly savings against closing costs to determine your recovery timeline (most borrowers who save $200 monthly recover expenses within 30 months). This makes the decision financially sound for those who plan to stay in their homes long-term.

Experienced mortgage professionals streamline the process and help you avoid costly mistakes. We at Kearns Mortgage Team provide personalized guidance through various loan options and competitive rates. Take action when multiple factors align favorably rather than wait for perfect market conditions that may never materialize.