Choosing the right mortgage lender can save you thousands of dollars and months of stress. Yet most homebuyers rush into this decision without asking the essential questions.

We at Kearns Mortgage Team see borrowers make costly mistakes because they didn’t know what questions to ask their mortgage lender upfront.

The right questions protect your financial future and reveal which lenders truly have your best interests at heart.

What Loan Types and Terms Should You Expect

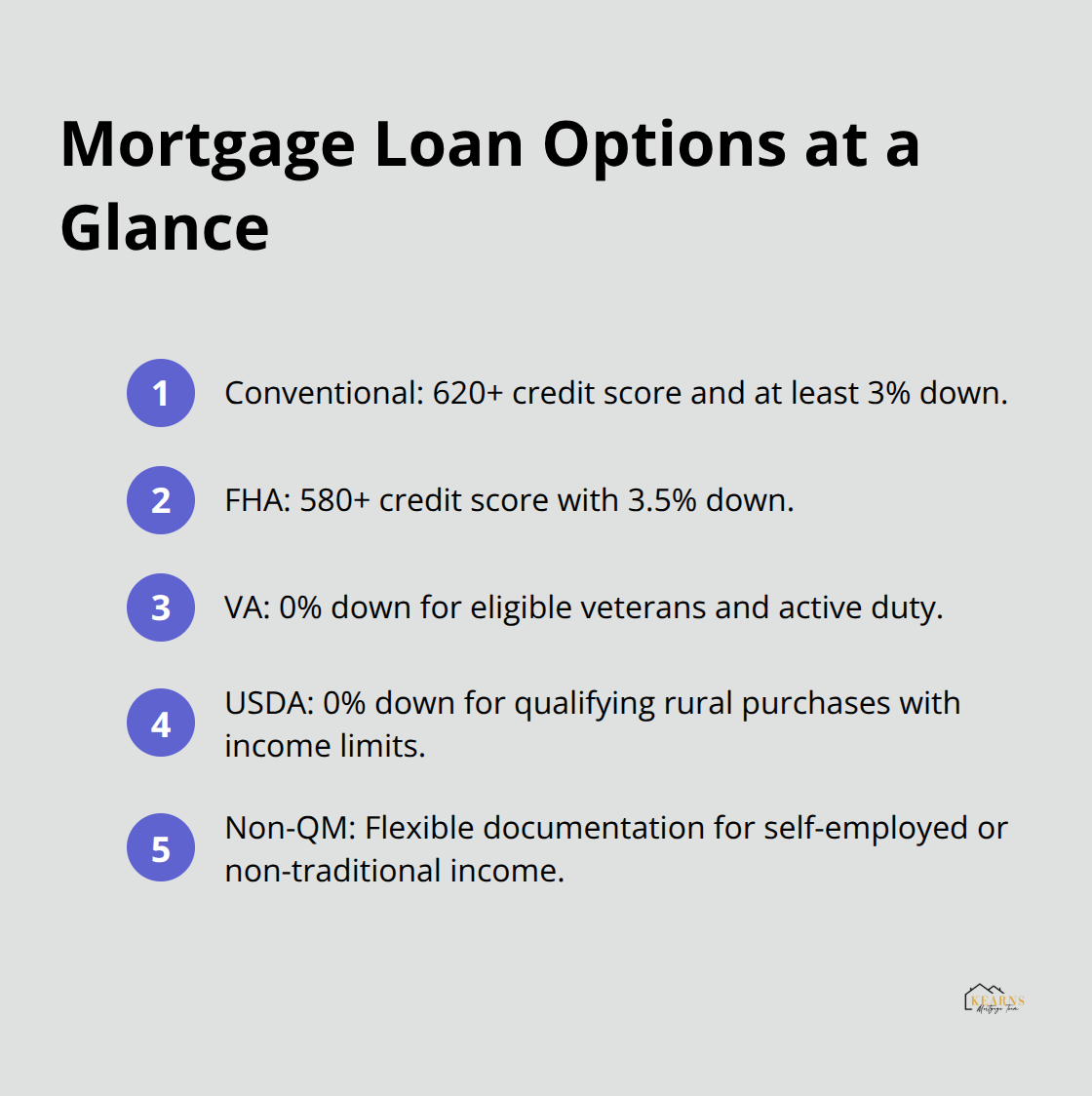

Your lender should offer multiple loan options and explain which fits your specific financial situation. Conventional loans work best for borrowers with strong credit scores above 620 and at least 3% down payment. FHA loans serve borrowers with credit scores as low as 580 and require just 3.5% down. VA loans provide zero down payment options for eligible veterans and active military members. USDA loans offer zero down payment for rural property purchases with income restrictions. Non-QM loans help self-employed borrowers or those with unique income situations who don’t fit traditional boxes.

Interest Rate Transparency Reveals True Costs

Ask your lender to explain their rate determination process and current market conditions. Mortgage rates depend on your individual credit profile and broader economic conditions, changing based on your credit score, loan amount, and down payment percentage. The difference between a 6.5% and 7% interest rate on a $300,000 mortgage costs you an extra $90 monthly and $32,400 over 30 years. Request both the interest rate and APR (which includes all lender fees). A lender who offers 6.75% with 1% fees might cost more than one who offers 7% with no fees. Rate locks protect you from increases during your 30-60 day period.

Closing Cost Breakdown Prevents Surprises

Total costs typically range from 2% to 6% of your loan amount, which means $6,000 to $18,000 on a $300,000 mortgage. Demand a detailed breakdown that includes appraisal fees around $500-800, charges up to 1% of loan amount, title insurance that costs 0.5% to 1% of home price, and government fees near $125. Some lenders advertise no costs but hide these expenses in higher monthly payments. Compare total costs over five years since most borrowers refinance or move within this timeframe.

Documentation Requirements Set Expectations

Your lender should provide a clear list of required documents upfront. Standard requirements include two years of tax returns, recent pay stubs, bank statements from the past two months, and employment verification letters. Self-employed borrowers need additional documentation like profit and loss statements and business tax returns. The application and approval process becomes much smoother when you understand exactly what paperwork your lender needs from the start.

How Long Will Your Mortgage Application Take

Timeline Expectations From Application to Closing

Most mortgage applications take 30 to 45 days from submission to closing, though this timeline varies based on your loan type and documentation completeness. FHA and VA loans typically require 45 to 60 days due to additional government processing requirements. Conventional loans with strong credit profiles and complete documentation often close within 25 to 35 days. The Consumer Financial Protection Bureau requires lenders to provide a Loan Estimate within three business days of your application (which gives you the first concrete timeline for your specific situation). Cash-out refinances take longer than purchase loans, often extending the process by 10 to 15 additional days.

Documentation Speed Determines Your Success

Your pre-approval strength depends entirely on documentation completeness at submission. Incomplete applications create delays that push closing dates back weeks. Tax returns from the past two years, recent pay stubs that cover 30 days, bank statements from two months, and employment verification letters form the foundation of every strong application. Self-employed borrowers need profit and loss statements, business bank statements, and CPA-prepared financial statements. Missing any single document restarts the underwriter review process and adds 7 to 14 days to your timeline.

Financial Changes During Underwriting Can Derail Your Loan

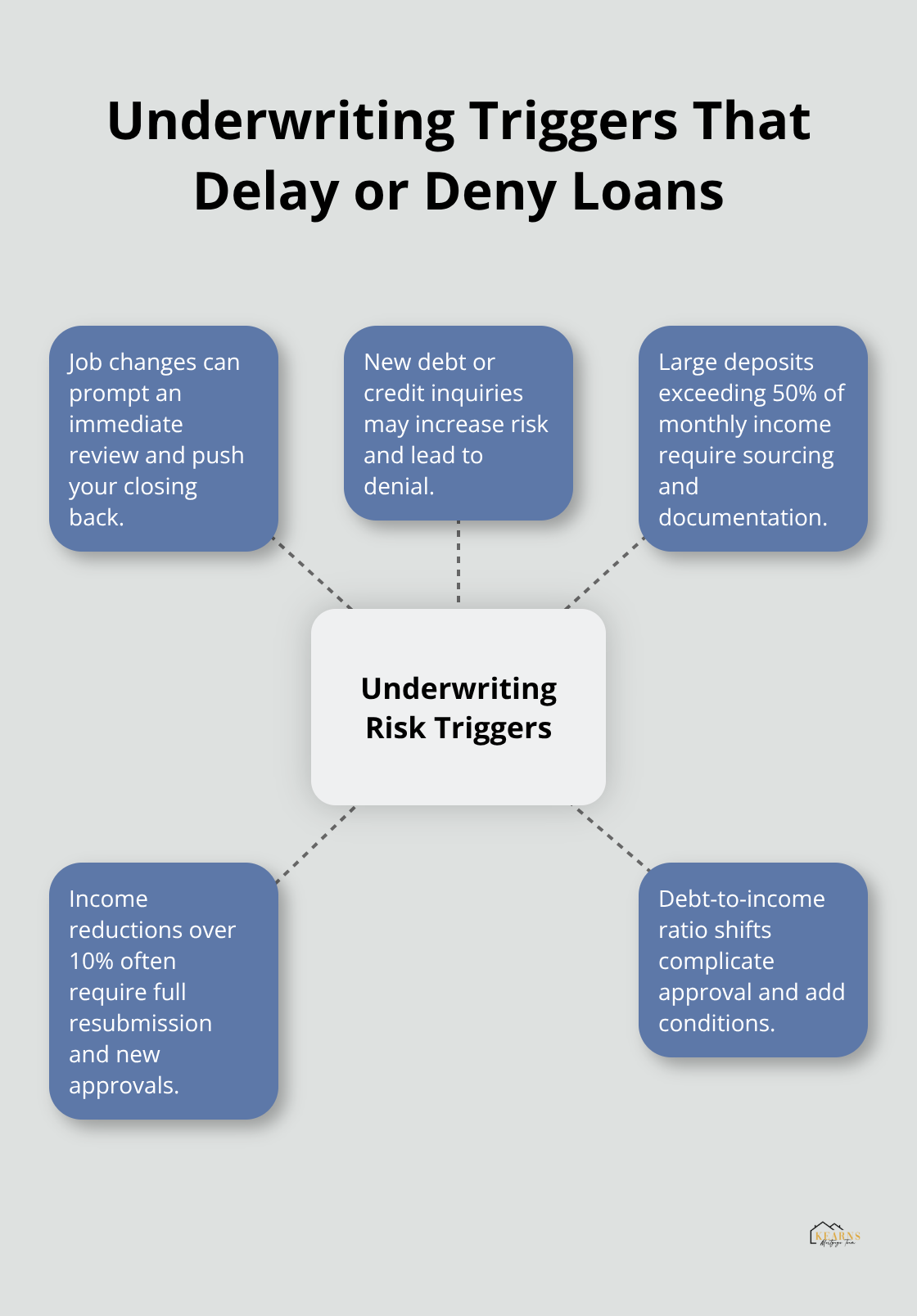

Job changes, new debt, or large deposits trigger immediate underwriter reviews that can delay or deny your loan approval. Opening new credit cards or financing furniture purchases between application and closing often results in loan denial (even days before your scheduled closing). Large deposits that exceed 50% of your monthly income require extensive documentation and explanation, regardless of the source. Income reductions of more than 10% typically require complete loan resubmission with updated documentation. The underwriting process becomes significantly more complex when your debt-to-income ratio changes after initial approval.

Understanding these timelines helps you plan your home purchase or refinance effectively, but the process becomes much smoother when you know exactly how your lender will communicate with you throughout each stage.

What Communication Can You Expect From Your Lender

Weekly Updates Keep Your Purchase on Track

Your lender should contact you at least weekly with specific progress updates, not generic automated messages. Strong lenders provide detailed status reports that include completed milestones, pending requirements, and exact next steps with deadlines. Purchase contracts can fall through due to financing issues, often stemming from poor communication between lenders and borrowers. Your loan officer should respond to emails within 24 hours and phone calls within 4 hours during business days. Demand access to an online portal where you can track your application status in real time and upload documents instantly.

Post-Closing Support Determines Long-Term Value

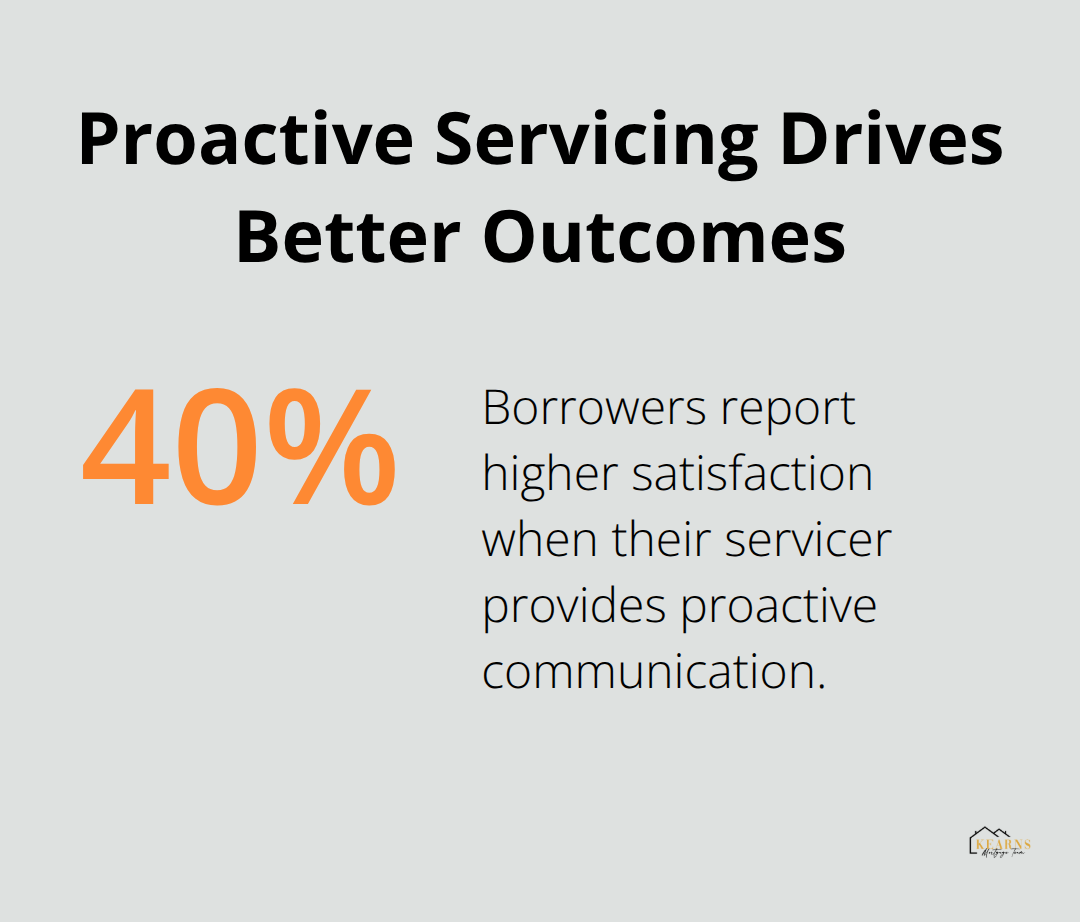

Top lenders provide lifetime support that extends far beyond your closing date. Your lender should offer free annual mortgage reviews to assess refinancing opportunities when rates drop or your financial situation improves. Quality lenders maintain dedicated servicing departments that handle payment questions, escrow adjustments, and payoff requests without transferring you between multiple representatives. According to J.D. Power mortgage servicing studies, borrowers who receive proactive communication from their servicer report 40% higher satisfaction scores. Your lender should also provide tax document preparation assistance and help you understand how mortgage interest deductions affect your annual tax planning.

Single Point of Contact Streamlines Your Experience

Work exclusively with lenders who assign one dedicated loan officer to handle your entire transaction from application through closing. This person should have direct access to underwriters and processors to resolve issues immediately rather than play telephone between departments. Your loan officer should attend your closing or have a designated representative who knows every detail of your file. Lenders who shuffle clients between multiple team members create confusion and delays that can jeopardize your purchase timeline. The best lenders also provide direct cell phone numbers for your loan officer and guarantee same-day responses to urgent questions during your transaction (which protects your closing date from unexpected complications).

Final Thoughts

The questions to ask your mortgage lender today determine whether you save thousands or lose money over the next 30 years. Borrowers who skip these conversations often face unexpected fees, poor communication, and limited loan options that don’t match their financial goals. The right lender partnership transforms homeownership from a stressful ordeal into a smooth process.

When your mortgage professional provides transparent rates, weekly updates, and lifetime support, you gain confidence in every decision. Poor lenders create delays, hidden costs, and communication gaps that can derail your purchase entirely. Your lender should provide a detailed timeline and explain each step before you sign any paperwork (which protects you from surprises during the process).

We at Kearns Mortgage Team provide expert guidance and personalized mortgage solutions throughout your entire home financing journey. Our team offers free consultations and transparent communication to help you make informed decisions. What specific financial goals do you want your mortgage lender to help you achieve beyond just approval for a loan?