Seller financing offers flexibility, but it often comes with higher interest rates and shorter loan terms that can strain your budget. Refinancing a seller financed mortgage into a conventional loan can lower your monthly payments and give you better long-term stability.

At Kearns Mortgage Team, we’ve helped homeowners navigate this transition successfully. This guide walks you through the process step by step, from understanding your current situation to finding the right lender for your needs.

Understanding Seller Financing and Why Refinancing Matters

What Seller Financing Really Costs You

Seller financing happens when the property seller acts as your lender instead of a bank. You make monthly payments directly to the seller, and they hold the title until you’ve paid off the full purchase price plus interest. This arrangement often includes a balloon payment at the end-a large lump sum that comes due on a specific date. The interest rates on seller-financed deals typically range from 4% to 7%, though some arrangements charge higher rates depending on the seller’s risk tolerance and market conditions. Unlike traditional mortgages reported to credit bureaus, seller-financed payments on your credit report may not build your credit score, leaving you without proof of payment history when you later apply for conventional financing. Many homeowners enter seller financing as a stepping stone, planning to refinance within five to ten years into a conventional, FHA, or VA loan once they’ve built stronger credit or accumulated equity.

Why Refinancing Becomes Necessary

Most seller-financed deals come with fixed terms of five to ten years, which means that balloon payment arrives whether you’re ready or not. If you have a balloon payment of $150,000 or more looming, refinancing into a conventional mortgage becomes your best option to avoid a financial crisis. Lower interest rates offer another compelling reason-if you locked in a 6% seller-financed rate five years ago and conventional rates have dropped to 4.5%, refinancing could cut your monthly payment by hundreds of dollars. Refinancing also switches your loan to a traditional lender, giving you standard amortization schedules instead of unpredictable payment structures. The typical timeline starts around the 12-month mark after your first on-time seller-financed payment, when lenders start viewing your payment history as legitimate proof of creditworthiness. At this point, you have enough documentation to shop multiple conventional lenders and compare their offers side by side.

Real Obstacles You’ll Face

Lenders typically require 12 to 24 months of on-time seller-financed payments before considering your application, and those payments must be documented. If your seller didn’t require a title company to manage payments, you’ll need cancelled checks or a written payment summary from the original note holder to prove your history. Many lenders won’t recognize seller-financed payments on your credit report, so you’re essentially starting from scratch with credit bureaus-a frustrating reality that makes the refinancing process slower. The land contract itself must be properly recorded with the county; if it isn’t, lenders may treat your refinance as a new purchase rather than a refinance, which affects your access to home equity and tax treatment. Appraisals can also work against you if the property hasn’t appreciated since you bought it under seller financing. If the appraised value falls below your purchase price, your loan-to-value ratio climbs, making lenders nervous and potentially forcing you into private mortgage insurance or higher interest rates.

Moving Forward With Your Refinancing Plan

These obstacles are real, but they’re not insurmountable. The key is understanding what lenders need from you and preparing your documentation well in advance. Once you know exactly what you’re working with-your current interest rate, remaining balance, balloon payment date, and payment history-you can start evaluating which conventional loan products actually fit your situation.

Taking Action on Your Refinance

Organize Your Seller-Financed Loan Documents

Start by gathering your seller-financed loan documents and reviewing the exact terms you’re working with. You need the promissory note, the land contract or deed of trust, and your payment history showing every on-time payment for the past 12 to 24 months. Contact your original note holder or the title company managing payments and request a formal payment summary or copies of cancelled checks proving your payment record. This documentation becomes your foundation when you approach lenders, so organize it now rather than scrambling later.

Assemble Your Personal Financial Records

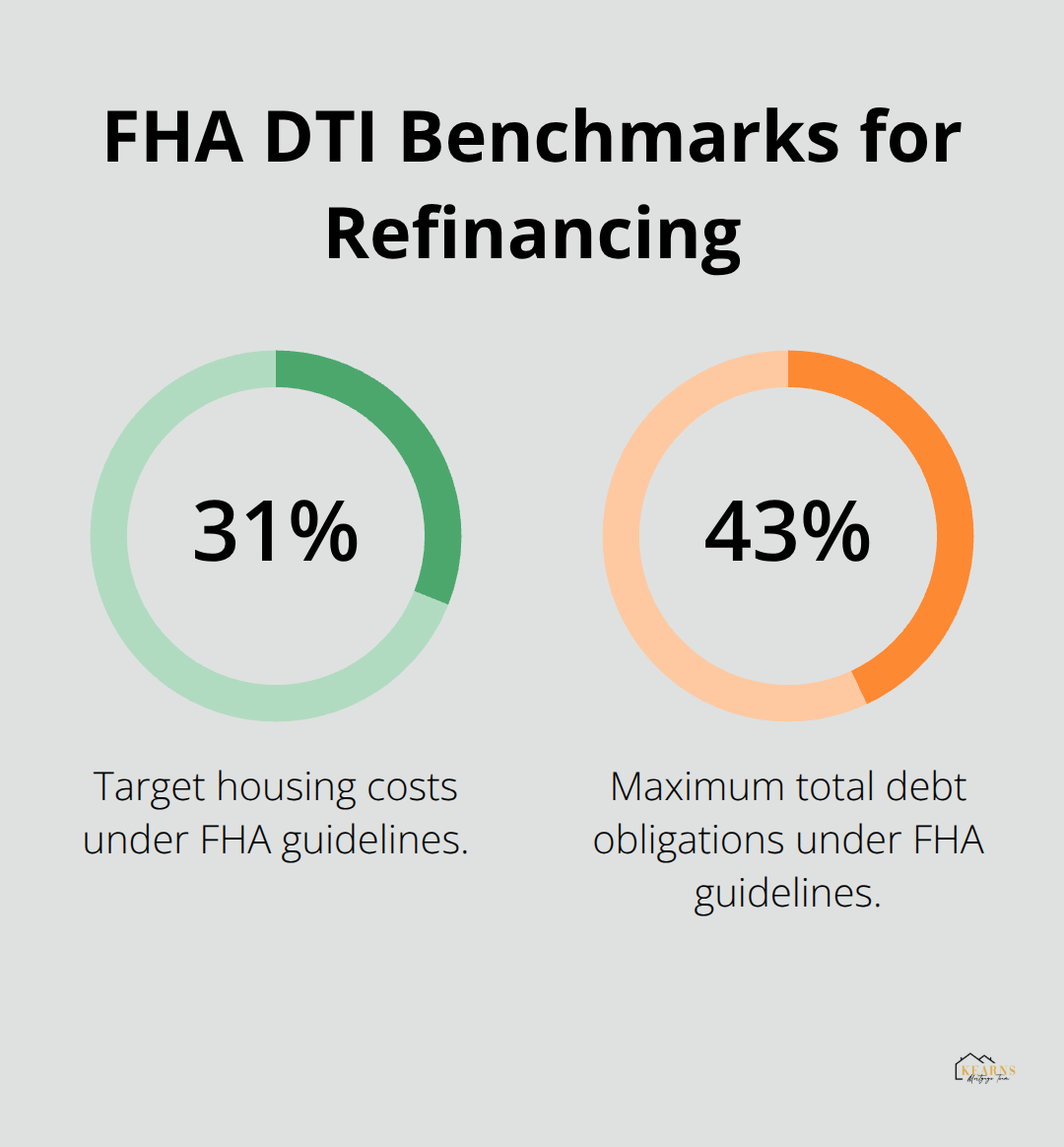

Next, gather your personal financial records: recent tax returns (typically two years), W-2s or 1099s showing stable income, current bank statements showing liquid reserves of three to twelve months of mortgage payments, and a detailed list of your debts with current balances. Lenders want to see a debt-to-income ratio that works within FHA guidelines of 31% toward housing costs and 43% toward total debt obligations. Calculate this number yourself before applying anywhere.

If you’re self-employed or have non-traditional income, prepare 12 to 24 months of bank deposits and up-to-date profit and loss statements to demonstrate income stability. Most importantly, check your credit report and dispute any errors before submitting applications, since even one incorrect late payment can tank your approval odds.

Compare Conventional Loan Options From Multiple Lenders

Shopping for the right conventional loan means comparing offers from at least three different lenders, not just one. Each lender will provide a Loan Estimate within three business days of your application, showing interest rates, closing costs, and monthly payments so you can appraise offers side by side. FHA loans work well if your credit is average and you have limited down payment funds, though they require mortgage insurance premiums that add to your monthly cost. Conventional loans become attractive once you’ve rebuilt credit and have at least 20% equity in the property, eliminating private mortgage insurance entirely. VA loans for eligible veterans and service members offer competitive rates without mortgage insurance requirements, making them the strongest option if you qualify.

Order an Appraisal and Understand Its Impact

Request a property appraisal early in the process and let the lender order it, not you, since lenders need the appraisal aligned with their underwriting standards. The loan-to-value ratio determines your interest rate and whether you’ll need mortgage insurance. If you’ve owned the property for less than 12 months, lenders typically use the lower of your original purchase price or the appraised value; after 12 months, they use a fresh appraisal alone. Shop rates with urgency but without panic-multiple inquiries within 45 days typically count as a single credit inquiry, so the small initial credit score dip from the first application won’t multiply with each additional lender you contact.

Move Toward Underwriting and Approval

Once you’ve selected your preferred lender and submitted your complete application, the underwriting process begins. The underwriter reviews your finances and property value, then requests additional documents if needed. Respond promptly to any requests, as delays can slow your timeline significantly. When approved, your new lender pays off the existing seller financing at closing, and you notify the original seller that their loan has been satisfied. At this point, your loan transfers to the traditional lender, and your seller no longer holds any claim to the property.

Finding the Right Loan Type and Lender for Your Refinance

Which Loan Product Fits Your Situation

FHA loans dominate the seller-financed refinance market because they accept non-traditional payment documentation and forgive credit history issues. FHA allows credit scores as low as 580, making it ideal if your seller-financed payments never reported to credit bureaus and your score suffered from other debts. The tradeoff is mandatory mortgage insurance premiums that add roughly 0.55% annually to your loan amount, increasing your monthly payment by $100 to $300 depending on your loan size. Conventional loans require a minimum credit score around 620 and at least 20% equity to skip private mortgage insurance entirely, but they offer lower interest rates once you qualify. If you’ve made on-time payments for 18 months and your credit has recovered, conventional refinancing saves thousands in insurance costs over the loan term.

VA loans for eligible veterans and service members eliminate mortgage insurance completely and typically offer the lowest interest rates available, making them the strongest choice if you served. Current 2026 mortgage rates for seller-financed refinances range from approximately 4% to 7% depending on credit, equity position, and loan type. Shorter amortization periods like 15 or 20 years save dramatically on total interest paid but increase monthly payments significantly; 30-year terms lower payments but cost more overall. If you face a balloon payment and need breathing room, a 10-year interest-only structure can bridge the gap until you refinance again or your financial situation improves.

What Lenders Examine in Your Application

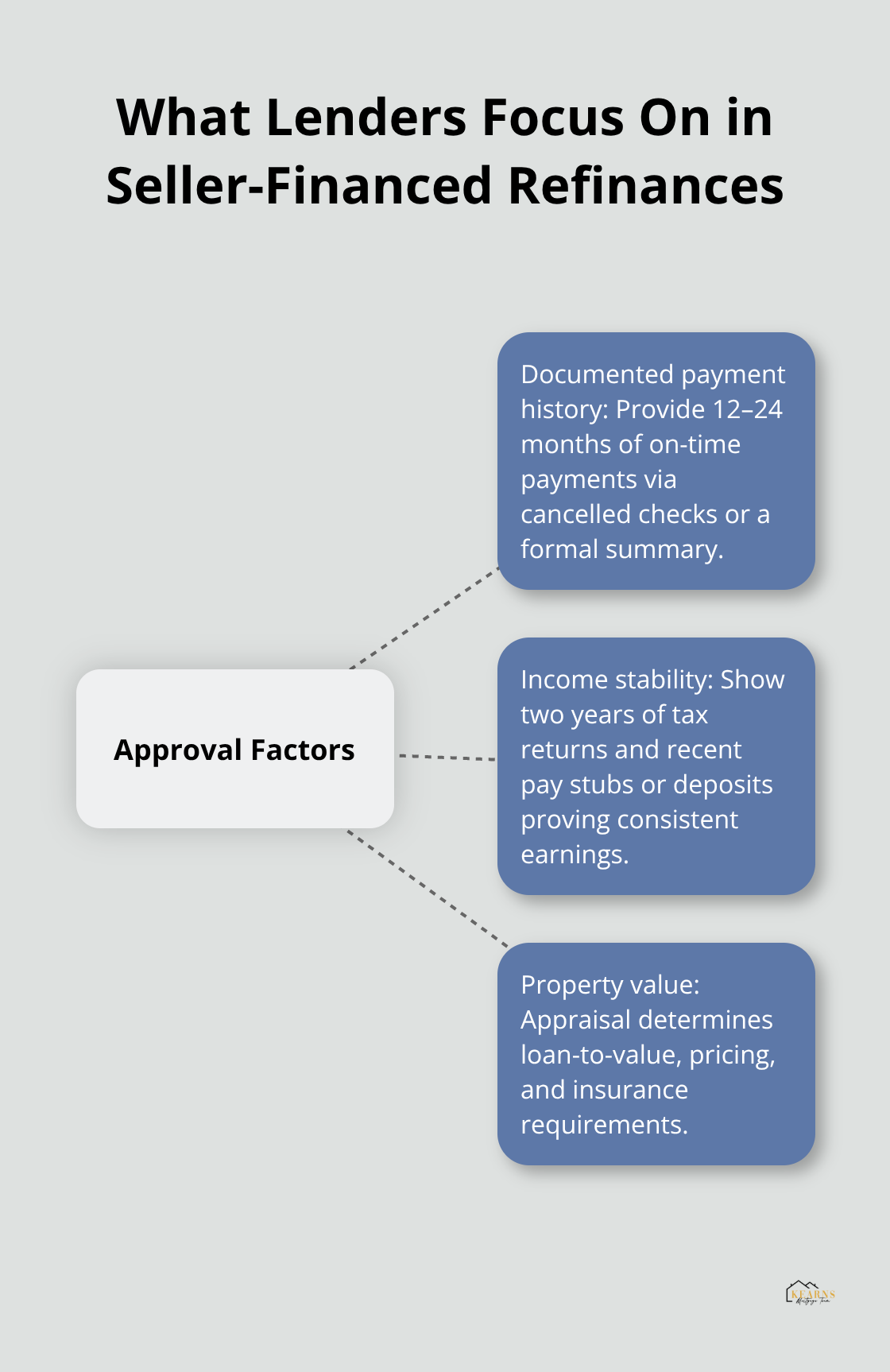

Lenders scrutinize three core areas when evaluating seller-financed refinance applications: documented payment history, income stability, and property value. You must show 12 to 24 months of consecutive on-time payments through cancelled checks or a formal payment summary from your original note holder, since most lenders won’t trust unverified payment records. Expect to provide two years of tax returns, recent pay stubs, and three to twelve months of bank statements proving liquid reserves equal to your mortgage payments.

Self-employed borrowers face stricter requirements and must submit 12 to 24 months of bank deposits plus current profit and loss statements to demonstrate income consistency.

Your debt-to-income ratio should stay around 40% or better; anything higher signals financial stress and triggers automatic denials. Lenders order professional appraisals to verify property value and calculate your loan-to-value ratio accurately. The appraisal determines whether you’ll qualify for favorable rates or face additional insurance costs, so its accuracy matters tremendously.

How Professional Guidance Strengthens Your Application

Working with a mortgage professional eliminates guesswork because they know exactly which documentation each lender demands and which loan products match your specific situation. A professional presents your seller-financed history in the strongest possible light, coordinates with your original note holder, orders the appraisal through proper channels, and manages the underwriting process so nothing falls through the cracks. This expertise accelerates your timeline and increases your approval odds significantly.

Final Thoughts

Refinancing a seller financed mortgage transforms your financial situation from uncertain to stable, moving you from higher interest rates and looming balloon payments into predictable monthly obligations with a traditional lender backing your loan. The process demands organization, patience, and clear documentation, but the payoff justifies the effort. Most homeowners who complete this transition save hundreds of dollars monthly and gain peace of mind knowing their loan follows standard banking practices.

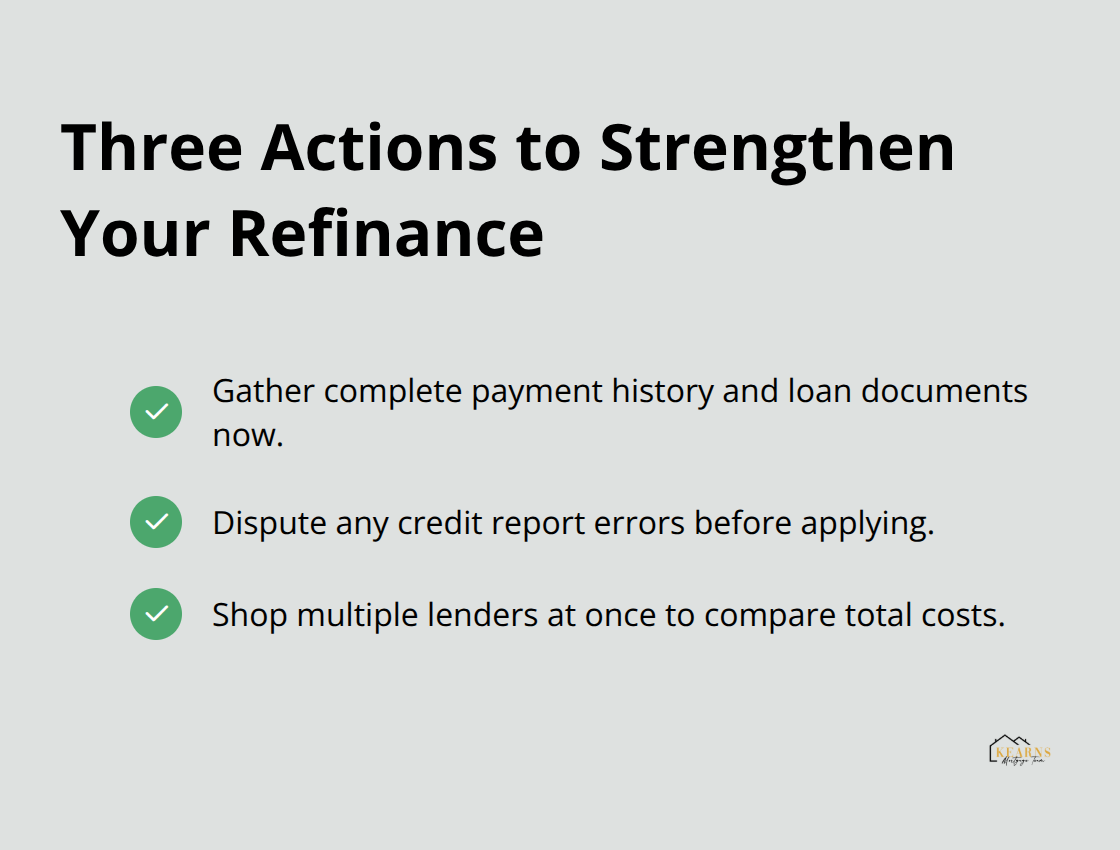

You control three concrete actions that determine your success. First, gather your complete payment history and loan documents now rather than waiting until you apply. Second, check your credit report for errors and dispute anything inaccurate before submitting applications anywhere. Third, shop multiple lenders simultaneously to compare rates, closing costs, and loan terms side by side, which reveals which offer actually saves you money over the life of your loan.

At Kearns Mortgage Team, we guide homeowners through refinancing seller financed mortgages every month and understand the specific challenges you face. We offer conventional, FHA, VA, and other loan options tailored to your exact situation, with competitive rates and transparent closing costs. What’s holding you back from starting your refinance conversation today?