Getting preapproved for a mortgage puts you ahead of other buyers in today’s competitive housing market. The process involves submitting financial documents to a lender who then evaluates your creditworthiness and determines how much you can borrow.

We at Kearns Mortgage Team see buyers with preapproval letters close deals 23% faster than those without them. Learning how to get preapproved for a mortgage properly can make the difference between landing your dream home or losing it to another buyer.

What Makes Preapproval Different from Prequalification

Mortgage preapproval requires a comprehensive financial review where lenders verify your income, assets, employment history, and credit score through hard documentation. This process includes a hard credit check and requires you to submit pay stubs, tax returns, bank statements, and W-2 forms. Prequalification relies on self-reported financial information and typically uses only a soft credit inquiry. The difference matters significantly because preapproval gives you a concrete loan amount based on verified data, while prequalification provides only an estimate that may not hold up during actual underwriting.

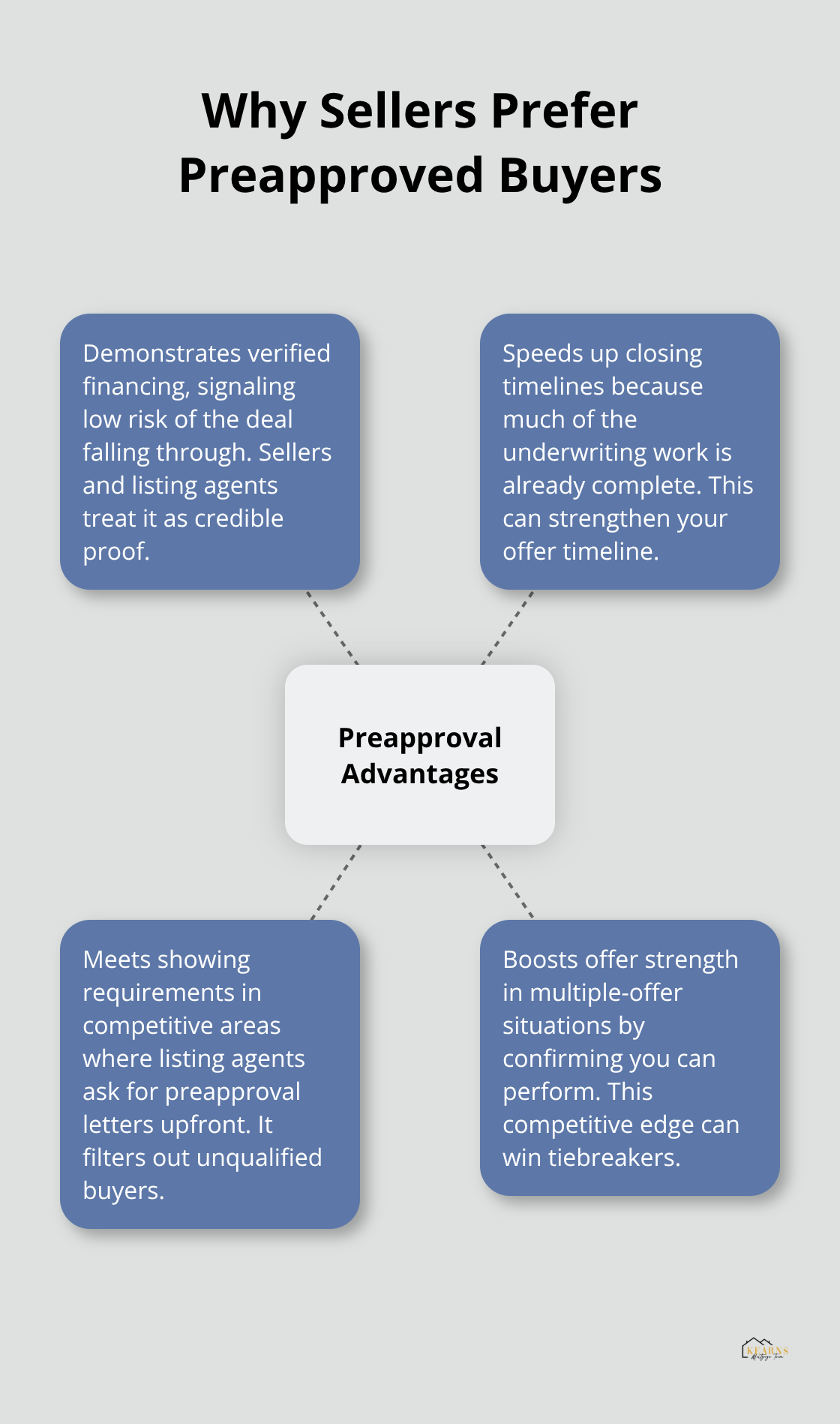

Why Sellers Choose Preapproved Buyers

Real estate agents report that preapproved buyers have significant advantages in competitive markets. Sellers view preapproval as proof that your financing is legitimate and unlikely to fall through during closing. In competitive markets, listing agents often require preapproval letters before they schedule showings, which effectively eliminates unqualified buyers from consideration. Your preapproval letter demonstrates financial capability and speeds up closing timelines since much of the underwriting work is already complete.

Preapproval Letter Expiration Dates

Most preapproval letters remain valid for 60 to 90 days, though some lenders may issue limits as short as 30 days. The expiration date reflects changing financial markets and helps lenders keep your approved loan terms current with interest rates and lending guidelines. If your letter expires before you find a home, you’ll need to update your financial documents and potentially undergo another credit check. Interest rates can shift during this period (sometimes significantly), so expired preapprovals may result in different loan terms when renewed.

The Documentation Advantage

Preapproval documentation creates a paper trail that underwriters trust. Lenders verify employment through direct contact with employers, confirm bank balances through statements, and calculate debt-to-income ratios using actual figures rather than estimates. This thorough vetting process means fewer surprises during final underwriting. Self-employed borrowers particularly benefit from preapproval since they can address complex income documentation upfront (rather than scrambling during closing).

Now that you understand how preapproval differs from prequalification, the next step involves gathering all the necessary documents and paperwork that lenders require for this comprehensive review process.

How Do You Navigate the Preapproval Process

Start by collecting your most recent pay stubs from the last 30 days, tax returns from the previous two years, and bank statements that cover the past two to three months. Self-employed borrowers need additional documentation that includes profit and loss statements, 1099 forms, and business tax returns. Veterans should obtain their Certificate of Eligibility from the Department of Veterans Affairs before they apply. Keep copies of government-issued identification, Social Security cards, and contact information for all employers from the past two years readily available.

Choose the Right Lender for Your Situation

Credit unions typically offer rates 0.25% to 0.50% lower than traditional banks, while online lenders often provide faster processing times with decisions within 24 to 48 hours. Compare at least three different lenders since interest rates can vary by up to 0.75% between institutions for identical borrower profiles. Submit applications within a 14-day window to minimize credit score impact (multiple mortgage inquiries can impact your credit scores, though the effect may vary). Request detailed loan estimates that include all fees and closing costs upfront to avoid surprises later.

Complete Employment and Income Verification

Lenders contact your employer directly to verify employment status, salary, and job tenure, usually within 72 hours of receipt of your application. This verification process confirms your current position and income stability. Employment history verification extends back two years, so prepare contact information for previous employers if you changed jobs recently.

Submit to Financial Account Review

Bank account verification involves confirmation of balances and deposit patterns over the past 60 days to identify any unusual activity. Lenders examine your savings, checking, and investment accounts to verify assets for down payment and closing costs. Large deposits require explanation and documentation (gift letters for family contributions or sale receipts for asset liquidation).

Meet Debt-to-Income Requirements

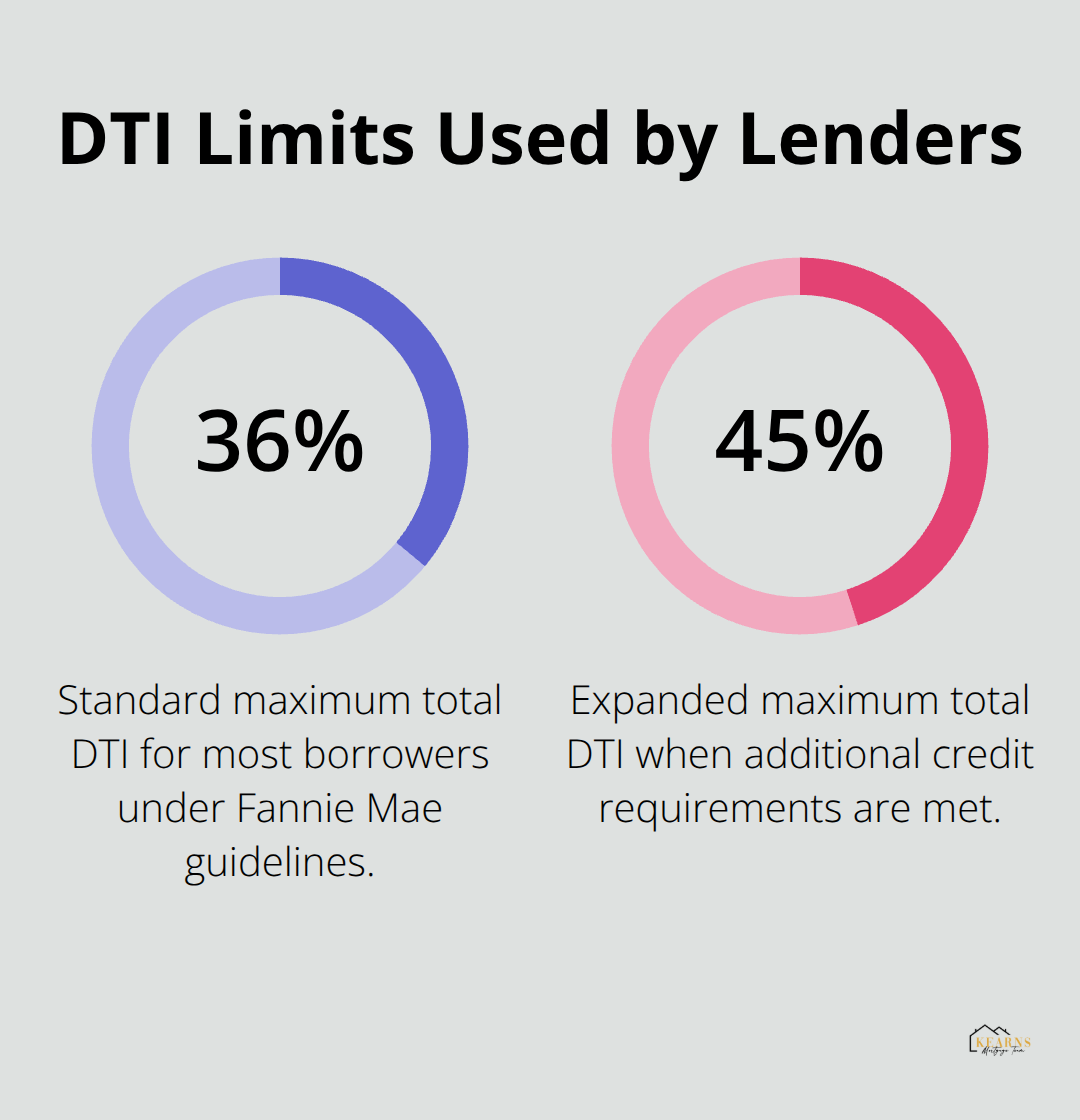

Your debt-to-income ratio calculation includes all monthly obligations, and Fannie Mae’s maximum total DTI ratio is 36% of the borrower’s stable monthly income, though this can be exceeded up to 45% if the borrower meets certain credit requirements. Lenders calculate this ratio using verified income and documented debt payments from credit reports. Avoid opening new credit accounts or making large purchases during this verification period, as these actions can delay approval or change your loan terms significantly.

Once lenders complete this comprehensive review of your finances, you’ll receive your preapproval decision and learn what to expect during the final approval timeline.

What Happens After You Submit Your Application

Timeline for Preapproval Decisions

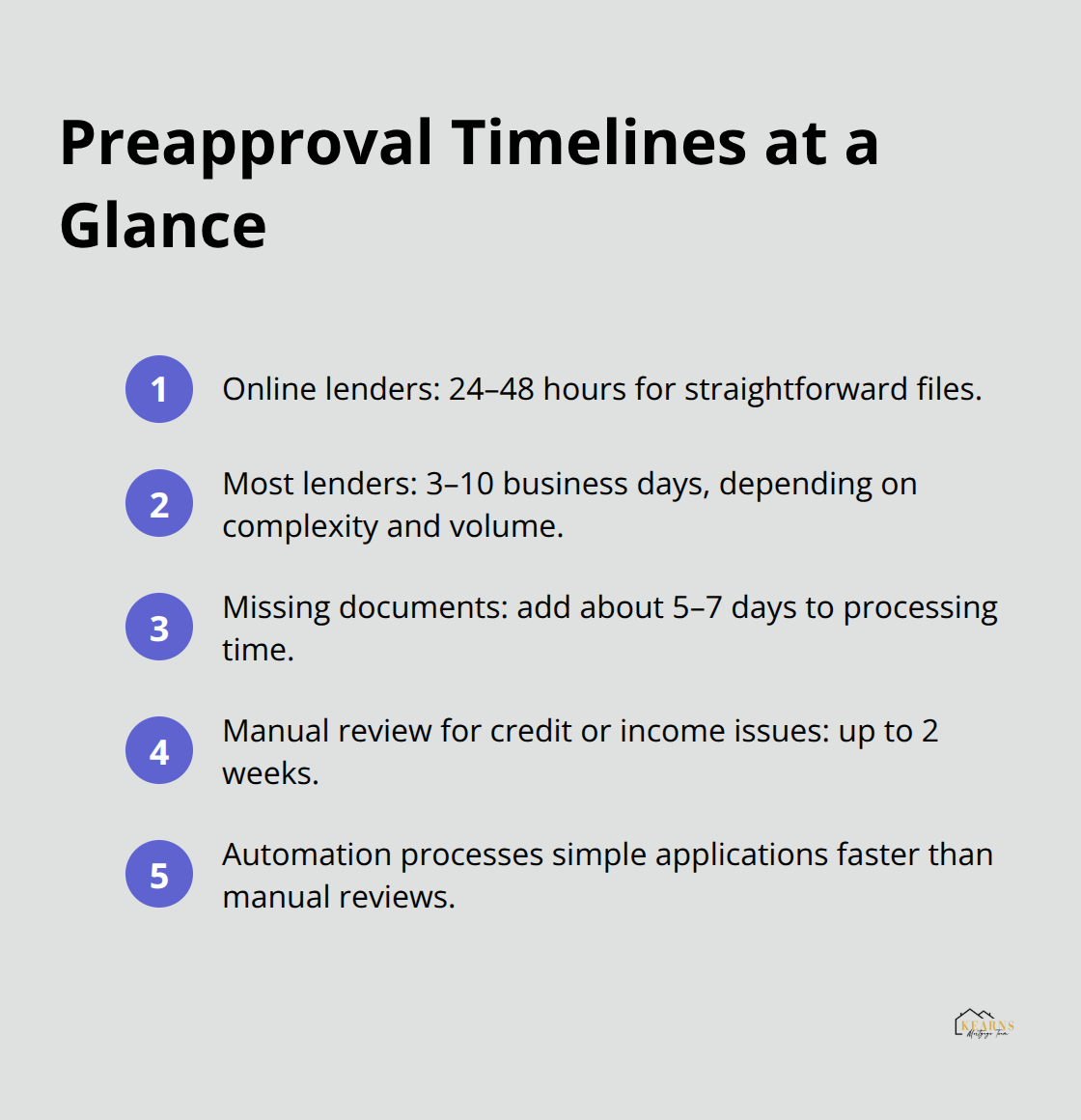

Most lenders provide preapproval decisions within 3 to 10 business days, though some online lenders deliver results in 24 to 48 hours. The timeline depends on your financial complexity and the lender’s current application volume. Automated systems process straightforward applications faster, while manual review adds time for self-employed borrowers or those with unique financial situations.

Incomplete documentation represents the primary cause of delays. Missing bank statements or employment verification extend timelines by 5 to 7 days. Credit issues like recent late payments or high debt-to-income ratios trigger manual review processes that can stretch decisions to 2 weeks.

How to Read Your Preapproval Letter

Your preapproval letter specifies the maximum loan amount, estimated interest rate, loan term, and expiration date. The loan amount reflects your qualified capacity based on verified income and credit profile, not necessarily what you should spend. Interest rates listed are estimates that can change before you close based on market conditions and final review.

Pay attention to the debt-to-income ratio calculation, as this determines your monthly payment capacity. Conditional approvals require additional documentation or debt payoff before final approval. The letter includes property requirements like maximum loan-to-value ratios and occupancy restrictions.

Some lenders include rate lock options that protect against interest rate increases for 30 to 60 days. Document any conditions carefully since you void your preapproval when you fail to meet them.

Employment Verification Requirements

Employment verification typically occurs again within 10 days of your close, so avoid job changes during this period. Lenders contact your employer directly to confirm your current position, salary, and job tenure. This verification process confirms your employment status and income stability throughout the loan process.

Common Reasons for Denial or Delays

Applications face denial when debt-to-income ratios exceed 50% for conventional loans or when credit scores fall below minimum thresholds. Recent credit inquiries, job changes within 6 months, or unexplained large deposits trigger additional scrutiny.

Self-employed borrowers experience delays when profit and loss statements don’t match tax returns or when business income shows decline trends. Bank account overdrafts within 60 days (even small ones) raise red flags about financial management. Lenders deny applications for undisclosed debts discovered during credit verification or when employment verification fails.

Gift funds require proper documentation with donor letters and bank statements. Missing paperwork delays approval and can jeopardize your home purchase timeline. If you’re considering an FHA loan, be aware that these loans have specific requirements that may affect your approval process.

Final Thoughts

Mortgage preapproval requires thorough preparation, complete documentation, and the right lender partnership. Your success depends on stable finances throughout the process, accurate paperwork submission, and clear understanding of your debt-to-income limits. The 60 to 90-day validity period means you must time your home search strategically after you receive approval.

Your preapproval letter opens doors to serious home shopping within your approved budget range. Connect with a real estate agent who understands the mortgage process and can guide you through competitive offers. Keep your financial situation stable (avoid new credit applications, job changes, or large purchases until closing) and review your letter carefully to understand any conditions that could affect final approval.

Experienced mortgage professionals make the process of how to get preapproved for a mortgage significantly smoother and more efficient. We at Kearns Mortgage Team provide personalized guidance through every step of your homeownership journey. What financial steps will you take today to strengthen your preapproval application and move closer to homeownership?