Getting pre-approved for an FHA loan opens doors to homeownership with lower down payment requirements and flexible credit standards. The process involves meeting specific financial criteria and submitting detailed documentation.

We at Kearns Mortgage Team guide borrowers through each step to streamline approval. Understanding how to get pre approved for FHA loan requirements saves time and prevents costly delays.

What Financial Requirements Must You Meet for FHA Pre-Approval

Credit Score Thresholds That Actually Matter

FHA loans require a minimum credit score of 500, but this baseline creates unrealistic expectations. Most lenders set their own standards at 580 or higher for the 3.5% down payment benefit. Borrowers with scores between 500-579 face a 10% down payment requirement, which defeats the primary advantage of FHA financing. The average FHA borrower today carries a credit score of 670 (according to recent HUD data). Focus on reaching 580 as your practical minimum target, though scores above 620 provide better interest rates and smoother approvals.

Income Documentation Standards

Employment verification demands two years of consistent work history in the same field or with the same employer. Self-employed borrowers need two years of tax returns plus profit and loss statements for the current year. FHA guidelines accept various income sources including overtime, bonuses, and commission, but only if you document them for 24 months. Part-time income counts when you maintain it for two years alongside primary employment. Social Security, disability, and pension income qualify with award letters and bank statements that show regular deposits.

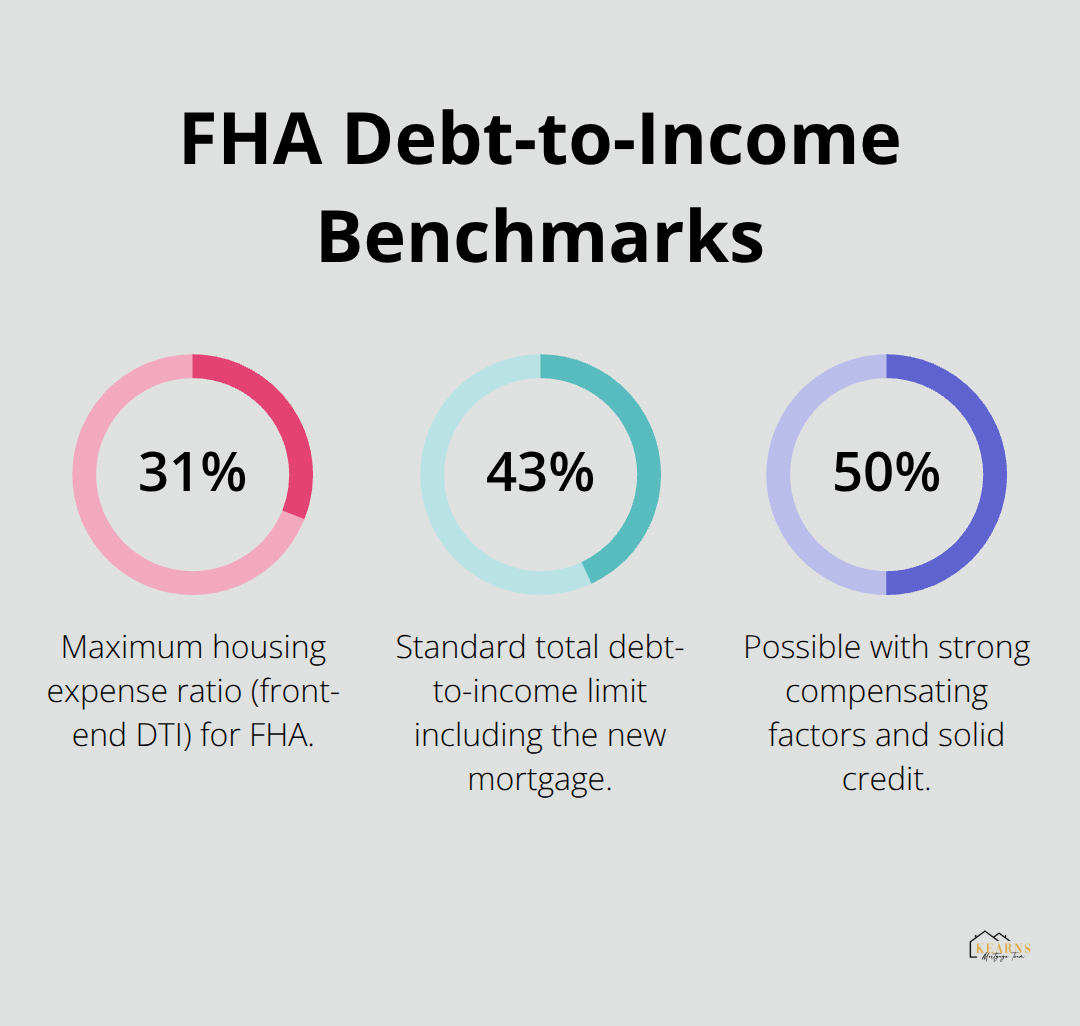

Debt-to-Income Calculations

FHA allows debt-to-income ratios up to 43% for total monthly obligations, including the new mortgage payment. Housing expenses alone cannot exceed 31% of gross monthly income. Calculate your housing ratio when you divide your proposed mortgage payment, insurance, taxes, and HOA fees by monthly gross income. For the total ratio, add all monthly debt payments including credit cards, student loans, and car payments.

Compensating factors like large down payments or cash reserves can push these ratios higher, sometimes reaching 50% with strong credit profiles.

Property and Down Payment Requirements

FHA loans require the property to serve as your primary residence, not an investment or vacation home. The minimum down payment starts at 3.5% for borrowers with credit scores of 580 or higher. You can source down payment funds from savings, family gifts, or approved down payment assistance programs. Gift funds must come with proper documentation from the donor. Properties must meet FHA safety and soundness standards, which an FHA-approved appraiser will verify before loan approval.

Once you understand these baseline requirements, the next step involves gathering the specific documents that prove you meet each criterion.

How Do You Navigate the FHA Pre-Approval Process

Collect Your Financial Documentation Package

You need your most recent two pay stubs, W-2 forms from the past two years, and federal tax returns with all schedules. Self-employed borrowers must provide signed tax returns, profit and loss statements for the current year, and business bank statements that span three months.

You should gather bank statements for all accounts from the past two months, which includes savings, checking, and investment accounts. Document any large deposits over $1,000 with paper trails that show their legitimate sources. Asset verification extends beyond bank balances to include retirement accounts, stocks, and bonds that demonstrate your financial stability.

Submit Your Application and Manage Underwriting

You complete the Uniform Residential Loan Application through your chosen lender and provide accurate information that matches your documentation exactly. Inconsistencies between application data and supporting documents trigger automatic delays. The underwriter reviews your file within 3-5 business days for initial approval or conditional approval with specific requirements. Conditional approvals typically request additional documentation like employment verification letters, explanation letters for credit inquiries, or updated bank statements. You should respond to underwriter requests within 24-48 hours to maintain momentum. The final underwriting decision arrives within 10-15 business days of complete file submission (assuming no complications arise).

Manage Timeline Expectations During Review

FHA pre-approval typically takes 30-60 days from application submission to final approval letter. Automated underwriting systems like Desktop Underwriter provide faster initial decisions, often within hours for straightforward applications. Manual underwriting extends timelines to 30-45 days but accommodates borrowers with unique financial situations. You must avoid major financial changes during this period, which includes new credit applications, large purchases, or job changes. Your pre-approval letter remains valid for 60-90 days (depending on lender policies), which gives you adequate time to shop for homes within your approved price range.

Even with proper preparation and documentation, many borrowers encounter preventable obstacles that can derail their pre-approval timeline.

What Pre-Approval Mistakes Can Destroy Your FHA Timeline

Documentation Errors That Stop Approval Dead

Missing signatures on tax returns create automatic rejections that add 7-10 days to your timeline. Bank statements must show consecutive months without gaps – a missing statement from two months ago forces you to restart the entire documentation process. Pay stubs need employer contact information that matches your W-2 forms exactly. Discrepancies between your application income and actual pay stub amounts trigger manual underwriting, which extends approval times. Self-employed borrowers who submit incomplete profit and loss statements face immediate conditional denials. You must sign every page of tax returns, including schedules, because unsigned documents get rejected without review. Asset statements require all pages, including blank ones that show account numbers.

Financial Changes That Kill Pre-Approval

New credit card applications during pre-approval drop your credit score by 5-15 points and trigger automatic re-underwriting. Job changes require 30 days of pay stubs from your new employer before underwriters will approve your file. Large deposits over $1,000 need complete paper trails – unexplained deposits create fraud alerts that can delay approval by 2-3 weeks. Complete credit card payoffs can actually hurt your score if they eliminate your credit utilization history. Car purchases during pre-approval change your debt-to-income ratio and often disqualify borrowers who were previously approved. Co-signers for family members add their debt to your DTI calculations and can push you over the 43% limit. These changes force lenders to restart the entire underwriting process, which means you lose your original approval and start over with new documentation requirements.

Lender Selection Mistakes That Cost Time and Money

Big box lenders often quote attractive rates but lack FHA expertise, which leads to conditional approvals that smaller specialized lenders would have avoided. Credit unions may offer member benefits but typically take 45-60 days for FHA approvals compared to 30 days with experienced FHA lenders. Online-only lenders create communication delays when underwriters need additional documentation – phone access to loan officers can save 5-7 days per request. Some lenders advertise FHA programs but actually prefer conventional loans, which results in delayed responses and poor service quality. Interest rate shopping should happen within 14 days to avoid multiple credit inquiries that damage your score (each inquiry can drop scores by 2-5 points). First-time buyers often make costly mistakes during this process that can be avoided with proper guidance.

Final Thoughts

Successful FHA pre-approval requires you to meet the 580 credit score threshold, maintain stable employment for two years, and keep debt-to-income ratios below 43%. The process moves faster when you submit complete documentation upfront and avoid financial changes during underwriting. Your pre-approval letter demonstrates serious buyer intent to sellers and real estate agents.

After you receive pre-approval, you have 60-90 days to find a home within your approved price range. Start shopping immediately because competitive markets move quickly, and delays can force you to restart the approval process. Understanding how to get pre approved for FHA loan requirements prevents costly mistakes that derail timelines (and saves you weeks of frustration).

Professional guidance eliminates documentation errors and timing issues that create unnecessary delays. We at Kearns Mortgage Team help borrowers navigate every step of the FHA pre-approval process. Which aspect of FHA pre-approval feels most challenging for your current financial situation?