Refinancing your mortgage can save you thousands in interest payments, but many homeowners miss out on potential tax benefits because they don’t understand the rules. The question of whether mortgage refinancing is tax deductible isn’t straightforward-it depends on several factors, from how you structure the loan to your overall tax situation.

At Kearns Mortgage Team, we’ve seen clients leave money on the table simply because they didn’t know what deductions applied to their refinance. This guide walks you through the tax implications of refinancing so you can make an informed decision.

How Mortgage Interest Deductions Actually Work

The Itemization Requirement

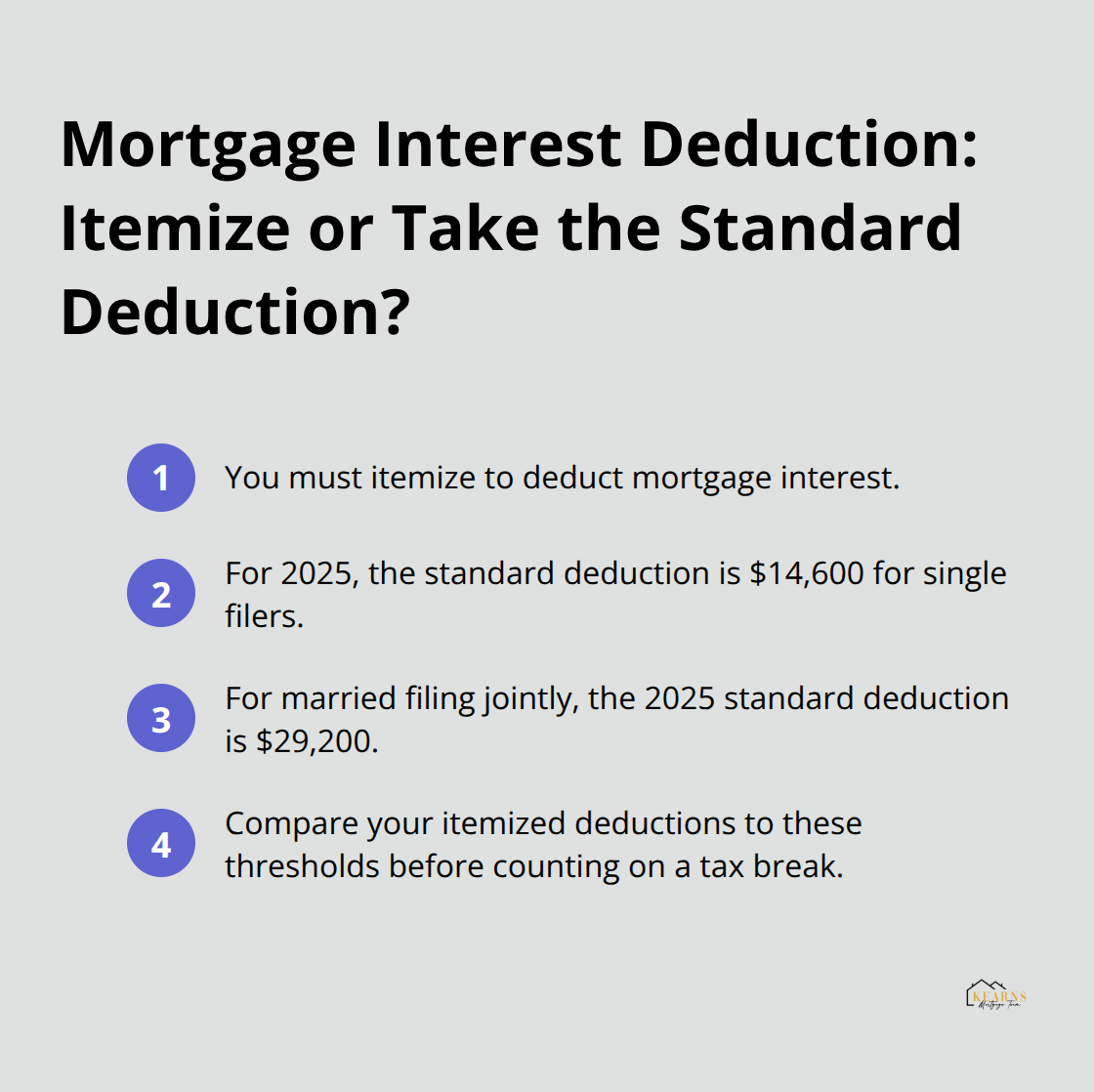

The mortgage interest deduction is only available if you itemize deductions on your tax return, and this is where most homeowners make their first mistake. The IRS allows you to deduct mortgage interest paid on loans secured by your primary residence or a second home you own, but only if that interest exceeds your standard deduction when combined with other itemizable expenses like property taxes and charitable contributions. For 2025, the standard deduction sits at $14,600 for single filers and $29,200 for married couples filing jointly, according to IRS guidelines. If your total itemized deductions don’t exceed these amounts, you gain nothing from the mortgage interest deduction because you’ll claim the standard deduction instead.

This is the critical calculation most people skip: they assume refinancing preserves tax benefits without checking whether itemizing actually saves them money. Your lender must issue Form 1098 at the end of the tax year, which shows exactly how much mortgage interest you paid. That number goes on Schedule A of your tax return, line 8a, assuming you itemize. Many homeowners refinance believing they’ll receive tax savings, only to discover later that their standard deduction was higher all along.

Debt Caps and Loan Origination Dates

The Tax Cuts and Jobs Act introduced a hard cap that affects your deductibility: loans originated after December 15, 2017 can only deduct interest on debt up to $750,000 if you’re married filing jointly or $375,000 if married filing separately. Older mortgages originated before that date can deduct up to $1,000,000 in debt. This matters when you refinance because if your home’s loan balance exceeds these limits, only the interest on the capped amount qualifies for deduction.

Additionally, the interest must be on debt used to buy, build, or substantially improve your home. If you do a cash-out refinance and use $50,000 to consolidate credit card debt or fund a vacation, that portion’s interest is completely nondeductible. Your filing status also impacts whether you can claim this deduction at all: you must file as single, married filing jointly, or head of household. Married filing separately filers face the lower $375,000 cap and reduced standard deduction, making refinancing for tax purposes even less attractive for that group.

What You Need to Calculate Before Refinancing

Before refinancing, calculate whether your expected itemized deductions will actually exceed your standard deduction, and confirm your loan balance stays within the cap. This single calculation determines whether refinancing offers any tax benefit at all. Once you understand these rules, you’re ready to explore how specific refinancing strategies-like paying points or taking cash out-interact with your tax situation.

The Real Tax Impact of Points, Costs, and Cash-Out Refinancing

How Points Work on a Refinanced Loan

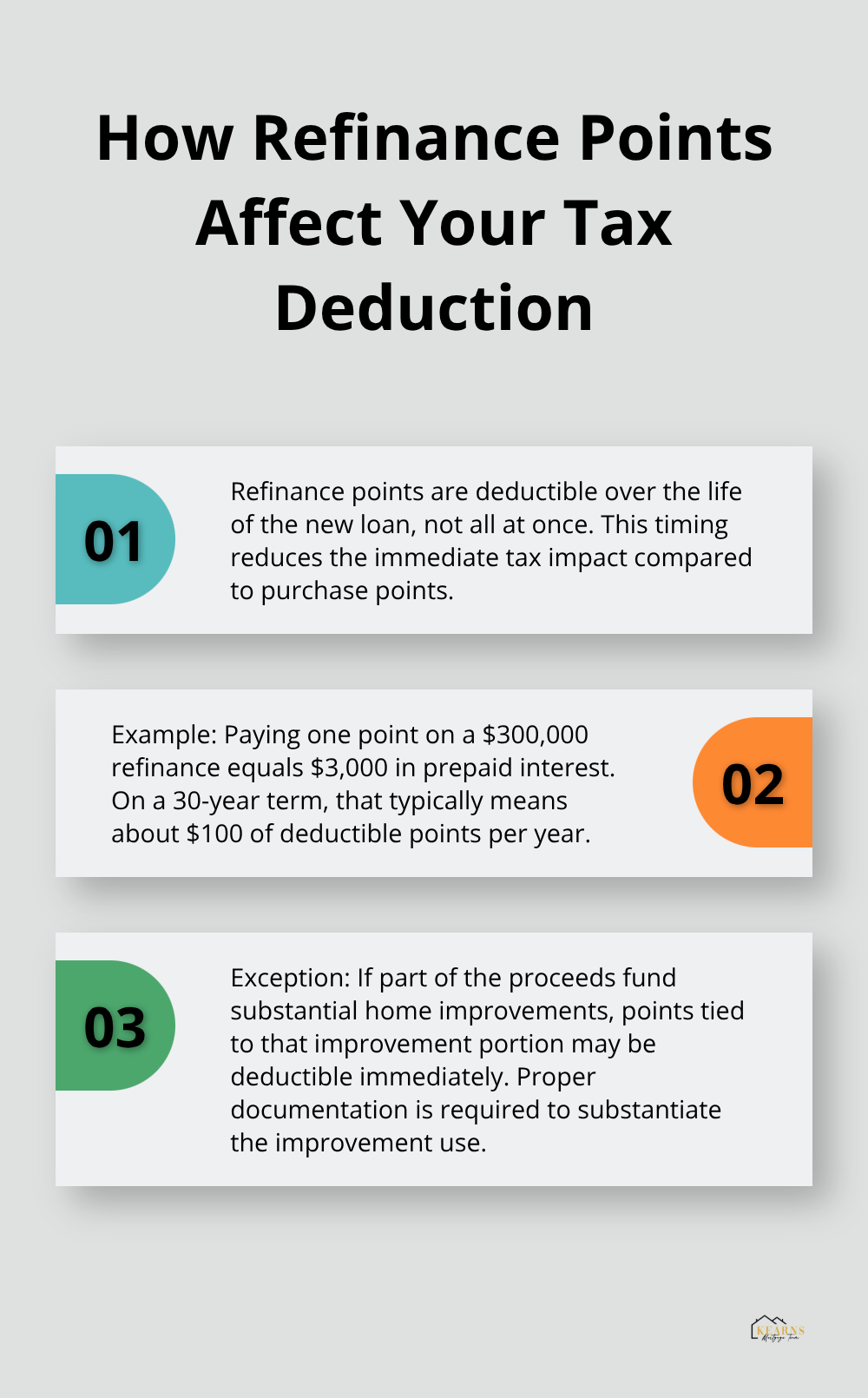

When you refinance, the IRS treats points very differently than most homeowners expect. Points paid on a refinance are deductible, but not all at once-you must spread them over the life of your new loan according to IRS Publication 936. If you pay one point on a $300,000 refinance, that equals $3,000 in prepaid interest spread across your loan term. On a 30-year mortgage, you deduct roughly $100 per year, not the full $3,000 upfront. This matters because many people refinance to lower their rate and assume they’ll recoup the points cost through immediate tax savings. That assumption fails.

The only exception occurs when part of your refinance proceeds go toward substantial home improvements like kitchen remodels, finished basements, or energy-efficient upgrades. In that case, you can deduct the interest on that portion immediately, potentially allowing full deductibility of points tied to improvements.

Closing Costs and the Break-Even Reality

Closing costs like appraisal fees, attorney fees, and recording fees are not deductible on a primary residence, even though they add to your out-of-pocket expense. This is where the math becomes critical-if you pay $4,000 in closing costs plus $3,000 in points, you won’t recover most of that through tax deductions. Calculate your break-even point by dividing total upfront costs by your monthly interest savings. If you save $150 per month in interest but paid $7,000 upfront, you need 47 months just to break even before considering the tax deduction delay. For rental properties, the situation flips entirely: you can deduct all closing costs, points, and mortgage interest against your rental income in the year paid. This transforms refinancing economics for investment properties because every dollar of costs reduces your taxable rental income immediately.

Loan Term Changes and Tax Consequences

Shortening your loan term from 30 years to 15 years during a refinance actually worsens your tax situation in most cases. With a shorter term, you pay less total interest over the life of the loan, which means smaller annual interest deductions. If you refinance from a 30-year mortgage at 5% interest to a 15-year mortgage at 4%, your monthly interest payments drop dramatically in year two and beyond. This is mathematically good for your wallet but bad for your tax deduction. Conversely, extending your loan term increases your annual interest deductions, but you’ll pay significantly more interest overall-a poor trade-off for a minor tax benefit.

Cash-Out Refinancing and Deductibility Rules

Cash-out refinancing creates the most confusion around deductibility. If you refinance for $400,000 and your previous loan balance was $300,000, that $100,000 cash-out is loan proceeds, not taxable income. However, only the interest on the $300,000 portion-the amount used to refinance your existing debt-remains deductible. The interest on the $100,000 cash-out is deductible only if you use those funds for substantial home improvements. Using cash-out proceeds for debt consolidation, vehicle purchases, or vacations generates completely nondeductible interest. This rule catches people off guard because they see the full loan amount and assume all interest is deductible. It isn’t. The IRS requires you to track how refinance proceeds are actually spent to determine what portion of your interest qualifies for deduction. If you took $100,000 cash-out and spent $60,000 on a kitchen renovation and $40,000 on credit card payoff, only the $60,000 portion’s interest is deductible-not the full loan’s interest. Understanding these distinctions between deductible and nondeductible portions of your refinance sets the stage for making decisions that actually improve your financial position rather than just your tax paperwork.

Making Refinancing Work Beyond the Tax Numbers

Focus on the Break-Even Math, Not Tax Timing

Most homeowners approach refinancing with their tax situation as the primary driver, but this puts the cart before the horse. The real question isn’t whether you’ll receive a tax deduction-it’s whether refinancing makes financial sense when you account for all costs and benefits. The timing of your refinance matters far less than people think. Popular advice suggests refinancing early in the year to maximize deductions, but this ignores a harder reality: if you’ll break even in 47 months, the three months you save from refinancing in January instead of April won’t meaningfully change your outcome. What actually matters is whether your monthly interest savings exceed your upfront costs within a reasonable timeframe-typically three to five years for most homeowners.

If you plan to sell or refinance again within that window, the math often doesn’t work, regardless of tax benefits. Run the actual numbers using your specific loan balance, new rate, loan term, and closing costs. A $4,000 closing cost on a $300,000 loan refinanced from 6% to 5% saves roughly $150 monthly in interest during year one, but that number shrinks each year as your principal balance drops. After 27 months, you’ve recovered your upfront costs. After that point, the remaining interest savings flow straight to your bottom line. To calculate your break-even analysis for refinancing, add up total costs and divide by your monthly savings. That’s when refinancing actually pays off-not because of tax deductions, but because the economics work.

Keep Meticulous Records for Tax Purposes

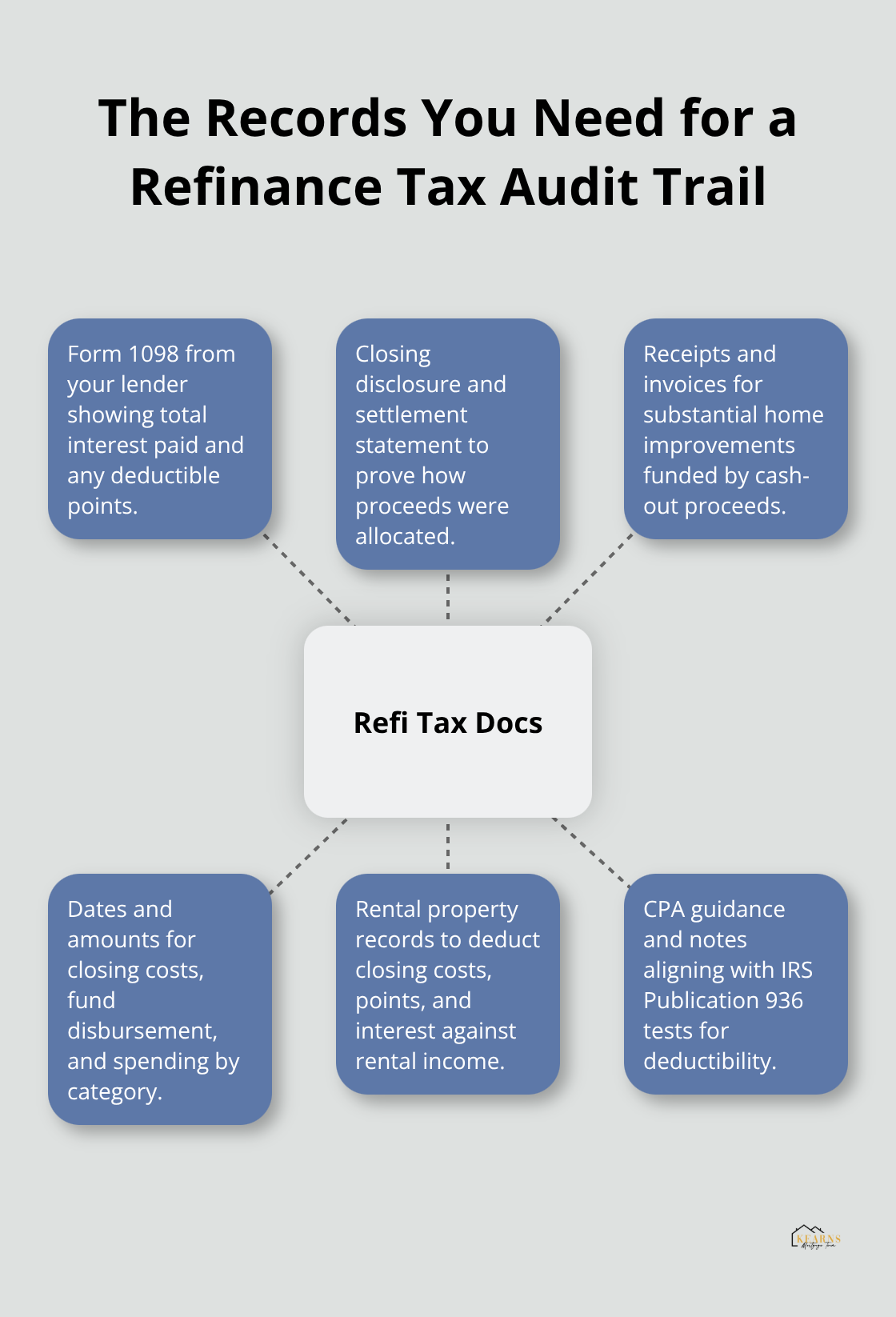

Documentation becomes your best defense against audit risk and missed deductions. The IRS requires you to keep Form 1098 from your lender showing total interest paid and any deductible points. Save your closing disclosure alongside your settlement statement to prove how refinance proceeds were allocated between refinancing existing debt and cash-out funds.

If you used cash-out proceeds for home improvements, maintain receipts and invoices proving those expenses qualify as substantial improvements under IRS standards-kitchen remodels, bathroom renovations, new roofs, and energy-efficient upgrades all qualify, but painting a bedroom or replacing carpet does not.

Track the date you paid closing costs, the date funds were disbursed, and how much you actually spent on each improvement category. When rental property owners refinance, this documentation becomes even more critical because they deduct closing costs and points against rental income, not just spread points over 30 years. A tax professional can help you allocate mixed-use expenses if your refinance funded both home improvements and non-deductible purposes. IRS Publication 936 provides the specific tests for deductibility, but a CPA familiar with your situation can identify deductions you’d miss on your own. This isn’t where you want to guess or estimate.

Final Thoughts

The answer to whether mortgage refinancing is tax deductible depends on your filing status, whether you itemize deductions, your loan balance relative to the debt cap, and how you use refinance proceeds. Most homeowners overestimate tax benefits because they ignore the itemization requirement or assume all closing costs and points qualify for immediate deduction. The real path forward requires you to run break-even math before refinancing and calculate whether your monthly interest savings exceed upfront costs within three to five years.

Start by gathering your current loan documents and requesting a refinance quote with all closing costs and points included. Compare your expected itemized deductions to the standard deduction for your filing status to determine whether you’ll actually benefit from the mortgage interest deduction. If you’re considering a cash-out refinance, track exactly how you’ll use those proceeds because only funds spent on substantial home improvements generate deductible interest on that portion (and a tax professional should review your specific circumstances before you commit).

For rental properties, the math shifts entirely because you can deduct all refinancing costs and interest against rental income immediately. We at Kearns Mortgage Team help homeowners evaluate refinancing from every angle, including tax implications specific to your situation. Ask yourself whether you’ll stay in your home long enough to recoup your costs and whether your new rate meaningfully improves your financial position.