Your credit score directly affects your ability to qualify for a mortgage in Tampa. A low score can mean higher interest rates, larger down payments, or outright rejection from lenders.

We at Kearns Mortgage Team know that credit score repair Tampa doesn’t happen overnight, but it’s absolutely possible with the right strategy. This guide walks you through concrete steps to rebuild your credit and move closer to homeownership.

What Actually Determines Your Credit Score

The Five Factors That Build Your Score

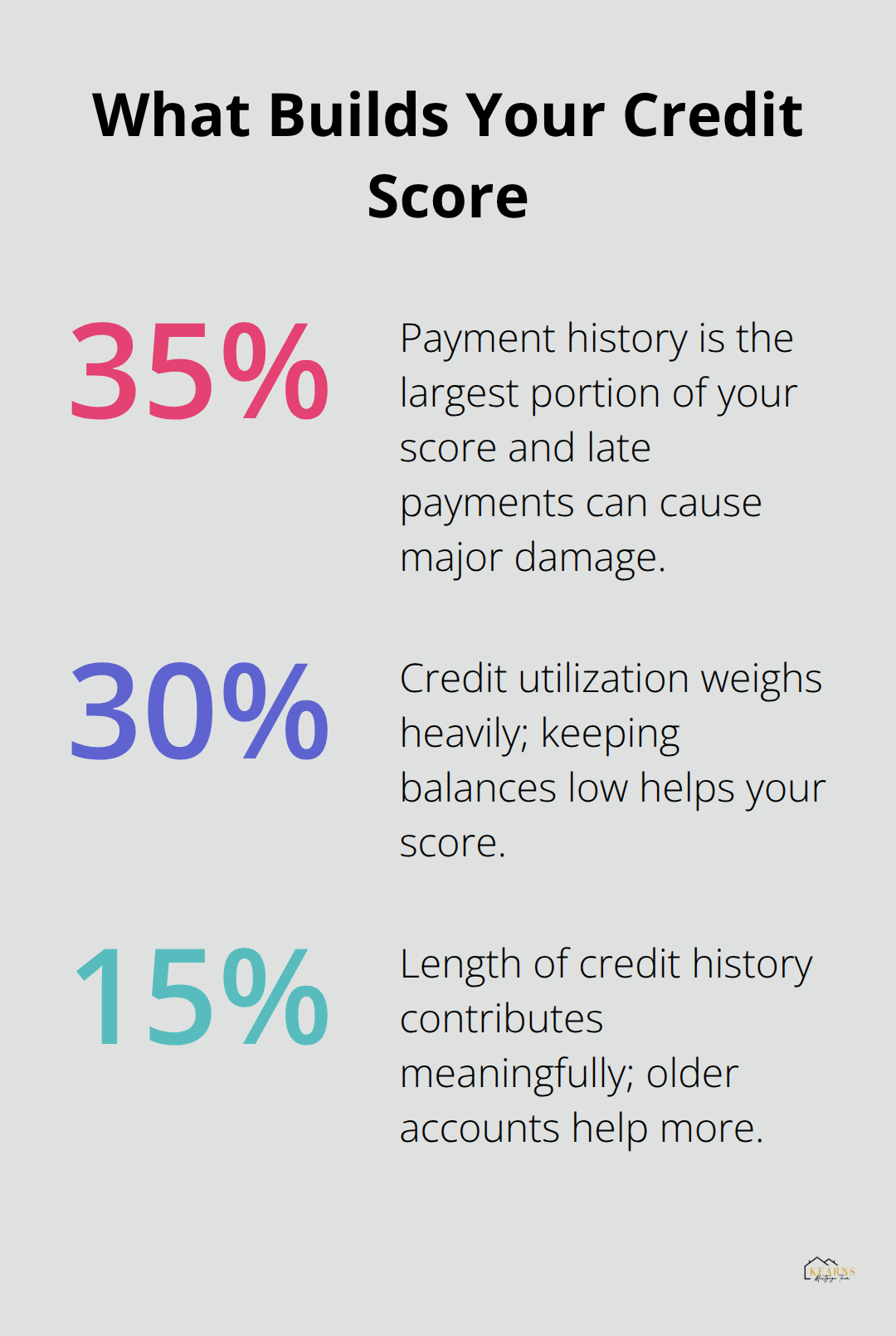

Your credit score is a three-digit number that lenders use to predict how likely you are to repay borrowed money. Scores range from 300 to 850, with higher scores indicating lower risk. The Fair Credit Reporting Act governs how the three major bureaus-Equifax, Experian, and TransUnion-calculate and report these scores. Payment history makes up 35 percent of your score, which means a single late payment can damage it significantly. Credit utilization accounts for 30 percent; try keeping balances under 30 percent of your credit limit, though under 10 percent works even better. The length of your credit history accounts for 15 percent, credit mix for 10 percent, and new inquiries for the remaining 10 percent.

Why Tampa Borrowers Struggle to Qualify

In Tampa’s mortgage market, many lenders require a minimum score of 620 for conventional loans, though some programs accept scores as low as 580. Late payments, collections, charge-offs, and bankruptcies are the primary reasons Tampa borrowers struggle to qualify. A single missed payment stays on your report for up to seven years, but its impact weakens over time. Foreclosures and short sales also damage your score severely and can remain visible for seven years, though lenders increasingly focus on the time elapsed since the event rather than its mere presence on your report.

How Your Score Affects Mortgage Terms

Your credit score directly controls the mortgage terms you’ll receive. A score below 620 typically means you’ll face higher interest rates, larger down payments, or restrictions on loan programs available to you. For example, conventional loans require at least 620, while FHA loans accept 580 and above. The difference between a 580 score and a 700 score can cost you tens of thousands in extra interest over the life of a 30-year mortgage. Tampa Bay mortgage delinquencies have risen to about 5.5 percent of loans 30 or more days past due, up from 3.3 percent a year ago, which means lenders are tightening their standards. This makes credit repair not just helpful but necessary if you want competitive rates and favorable terms.

Taking Action: Pull Your Reports and Dispute Errors

The path forward starts with pulling your free annual credit reports from AnnualCreditReport.com and reviewing each one carefully for errors or fraud. You’re entitled to one free report per year from each bureau, plus additional free reports if adverse action is taken against you. Disputes in writing with the bureau and the creditor, sent via certified mail with copies kept for your records, can remove items that don’t belong on your report. Under federal law, credit bureaus must investigate disputes within 30 days (or up to 45 days if you provide additional information). This step alone has helped many Tampa borrowers improve their scores before applying for a mortgage, and it positions you to move forward with confidence as you address the remaining factors in your credit profile.

How to Actually Fix Your Credit Right Now

Dispute Errors on Your Credit Report First

Disputing errors on your credit report is the fastest win available to you, and it costs nothing. Pull your reports from AnnualCreditReport.com and read them line by line for inaccuracies, fraud, or items that don’t belong to you. The Fair Credit Reporting Act requires bureaus to investigate your dispute within 30 days, or up to 45 days if you provide additional information. Send your dispute in writing via certified mail to both the bureau and the creditor listed on the account, keeping copies for yourself. Many Tampa borrowers find that 10 to 15 percent of their negative items disappear after a successful dispute because bureaus fail to verify the debt or the creditor doesn’t respond.

Pay Down Your Balances Aggressively

Once you’ve cleared errors, focus immediately on paying down your balances. Credit utilization makes up 30 percent of your score, so reducing what you owe relative to your limits produces fast results. If you carry a $5,000 balance on a $10,000 card, you’re at 50 percent utilization, which hurts your score significantly. Drop that balance to $3,000 and you jump to 30 percent utilization, which lenders prefer to see. Going lower to 10 percent or under accelerates improvement even more.

Set up automatic payments to prevent missed due dates, since payment history accounts for 35 percent of your score and a single late payment can undo months of progress. If your monthly bills feel unmanageable, contact your creditors directly to negotiate a payment plan. Many creditors will work with you rather than watch an account go delinquent because they recover more money from a structured arrangement than from collections. Keep these negotiated agreements in writing and follow them precisely.

Build Positive Credit History Through Strategic Accounts

Building positive credit history takes discipline but delivers real results within 60 to 90 days. If you lack recent positive payment history, a secured credit card reports to all three bureaus and shows lenders you can manage credit responsibly. Secured cards require a cash deposit (typically $500 to $2,500), which becomes your credit limit. Use it for one small recurring charge like a streaming subscription, set it to auto-pay in full each month, and let it report on time every single month. After 12 to 18 months of perfect payments, many issuers convert the secured card to an unsecured card and return your deposit.

The authorized user strategy can work if you’re added to an account with a long, clean payment history and low balance, but it backfires if the primary user misses payments. Space out any new credit applications by at least six months to avoid multiple hard inquiries, which temporarily lower your score for about 12 months. Close as many new accounts as you open to keep your total number manageable, but protect your oldest account even if you never use it, since credit history length accounts for 15 percent of your score and older accounts help you more than newer ones.

Your credit repair progress now positions you to explore mortgage options that match your improving financial profile. The next chapter examines how lenders evaluate your rebuilt credit and which loan programs work best for Tampa borrowers at different stages of credit recovery.

Mortgage Qualification During Credit Repair

Timeline for Credit Score Improvement

Credit improvement doesn’t happen in a straight line, and the timeline varies based on what’s on your report. If you dispute inaccurate items, you could see score increases within 30 to 45 days once the bureaus investigate and remove errors from your file. Paying down balances produces faster results than almost anything else, with many borrowers seeing 10 to 50 point improvements within one or two billing cycles as credit utilization drops. The Federal Trade Commission notes that negative information generally stays on your report for seven years, but its impact weakens significantly after two to three years, especially if you build positive payment history in the meantime.

Collections accounts that are paid in full still remain on your report for the full seven years, though some lenders weight recent delinquencies more heavily than older ones. If you had a bankruptcy, Chapter 7 stays visible for ten years while Chapter 13 typically falls off after seven years, but mortgage eligibility after bankruptcy is possible depending on the loan program and time elapsed. Most Tampa borrowers see meaningful score movement within 60 to 90 days of consistent on-time payments and reduced balances, positioning them to qualify for better loan terms well before their credit reaches pristine condition.

How Lenders Evaluate Your Credit Repair Progress

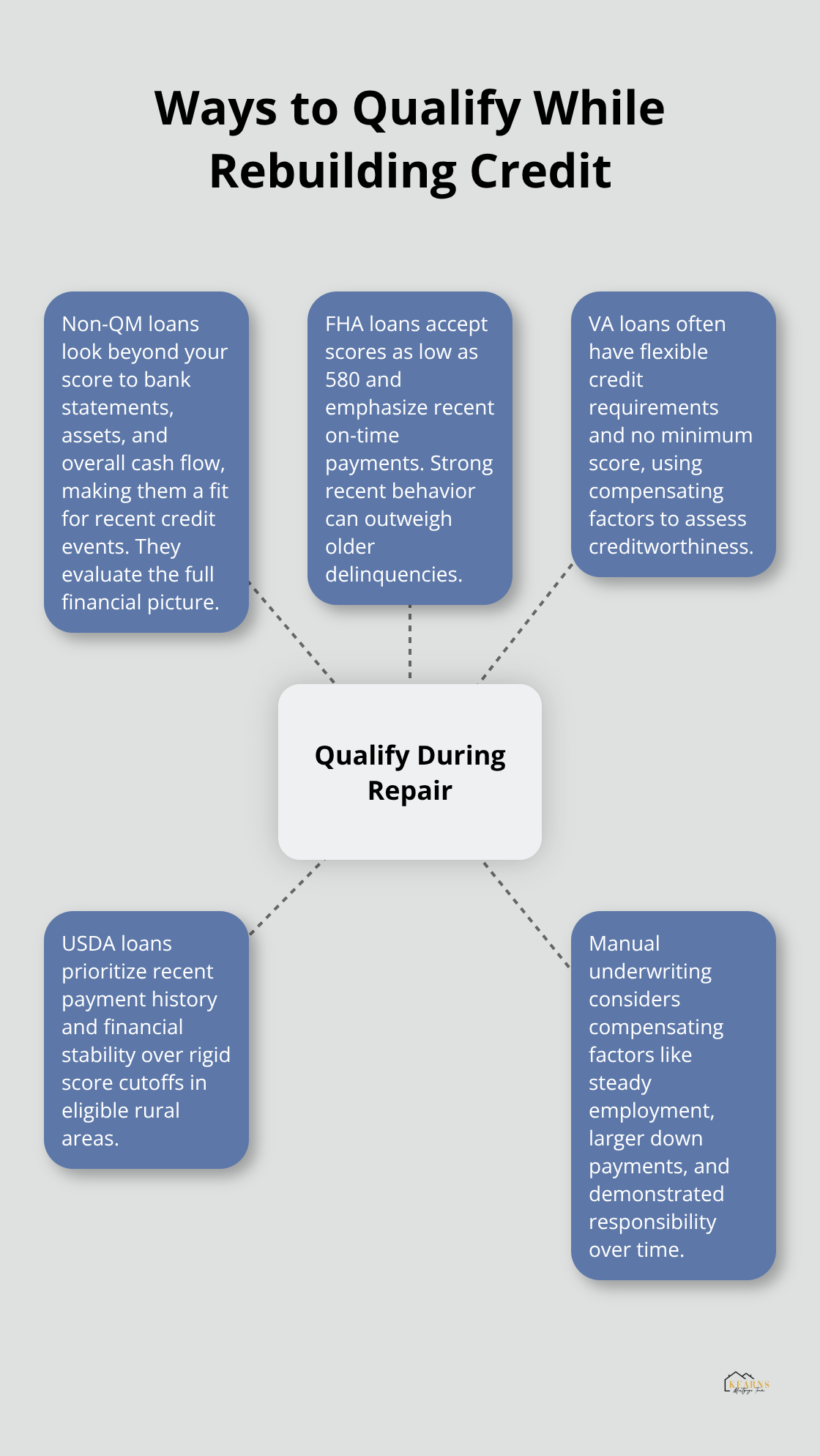

Lenders evaluate credit repair progress differently depending on their underwriting philosophy. Banks rely heavily on automated underwriting systems that apply rigid score thresholds, which can make credit repair feel like a pass-fail test. Manual underwriting considers compensating factors like stable employment history, substantial down payment, and demonstrated financial responsibility over time, meaning your improving credit combined with other strengths can qualify you for a mortgage even if your score hasn’t reached conventional lending minimums.

Loan Programs That Work During Credit Repair

Non-QM loans specifically look beyond the credit score to examine your full financial picture, including bank statements showing consistent deposits, assets on hand, and overall cash flow, making them ideal for borrowers with recent credit events who are actively rebuilding. FHA loans accept scores as low as 580 and focus on your recent payment behavior rather than your distant past, so if you’ve made on-time payments for the last 12 months despite an older delinquency, you’re a stronger candidate than your score alone suggests.

VA loans for eligible military borrowers often have more flexible credit requirements and no minimum score requirement, evaluating creditworthiness through compensating factors. USDA loans in eligible rural areas of Florida similarly prioritize recent payment history and overall financial stability over a specific score threshold. The key is understanding that your credit score is one data point, not your entire financial story, and working with a lender who will present your full picture to underwriters rather than letting an algorithm make the final decision.

Final Thoughts

Credit score repair in Tampa works when you follow a structured approach and stay committed to the process. The steps outlined in this guide-disputing errors, paying down balances, and building positive payment history-address the actual factors lenders evaluate. Your credit score isn’t permanent, and the damage from past mistakes fades over time, especially when you demonstrate consistent financial responsibility moving forward.

The path to homeownership doesn’t require a perfect credit score. Many Tampa borrowers qualify for mortgages while still rebuilding, particularly when working with lenders who evaluate your complete financial picture rather than relying solely on automated systems. FHA loans, Non-QM programs, and other flexible options exist specifically for borrowers in your situation, and understanding which loan program matches your current credit profile makes all the difference.

Start by pulling your free credit reports from AnnualCreditReport.com this week and reviewing them carefully for errors. Dispute anything inaccurate, then focus on reducing your credit card balances to below 30 percent of your limits. We at Kearns Mortgage Team offer free consultations to map your personalized path to homeownership, regardless of where your credit currently stands, and our team understands Tampa’s market well enough to connect you with loan programs designed for borrowers rebuilding credit.

What specific credit repair step feels most urgent for your situation right now?