Your credit score is the first thing lenders look at when you apply for a mortgage. A higher score opens doors to better interest rates and loan terms that can save you tens of thousands of dollars over the life of your loan.

We at Kearns Mortgage Team know that improving your credit for a mortgage doesn’t happen overnight, but it doesn’t have to be complicated either. Whether you’re months away from applying or just starting to think about homeownership, the steps you take now will directly impact the mortgage you qualify for.

Why Your Credit Score Matters for Mortgage Approval

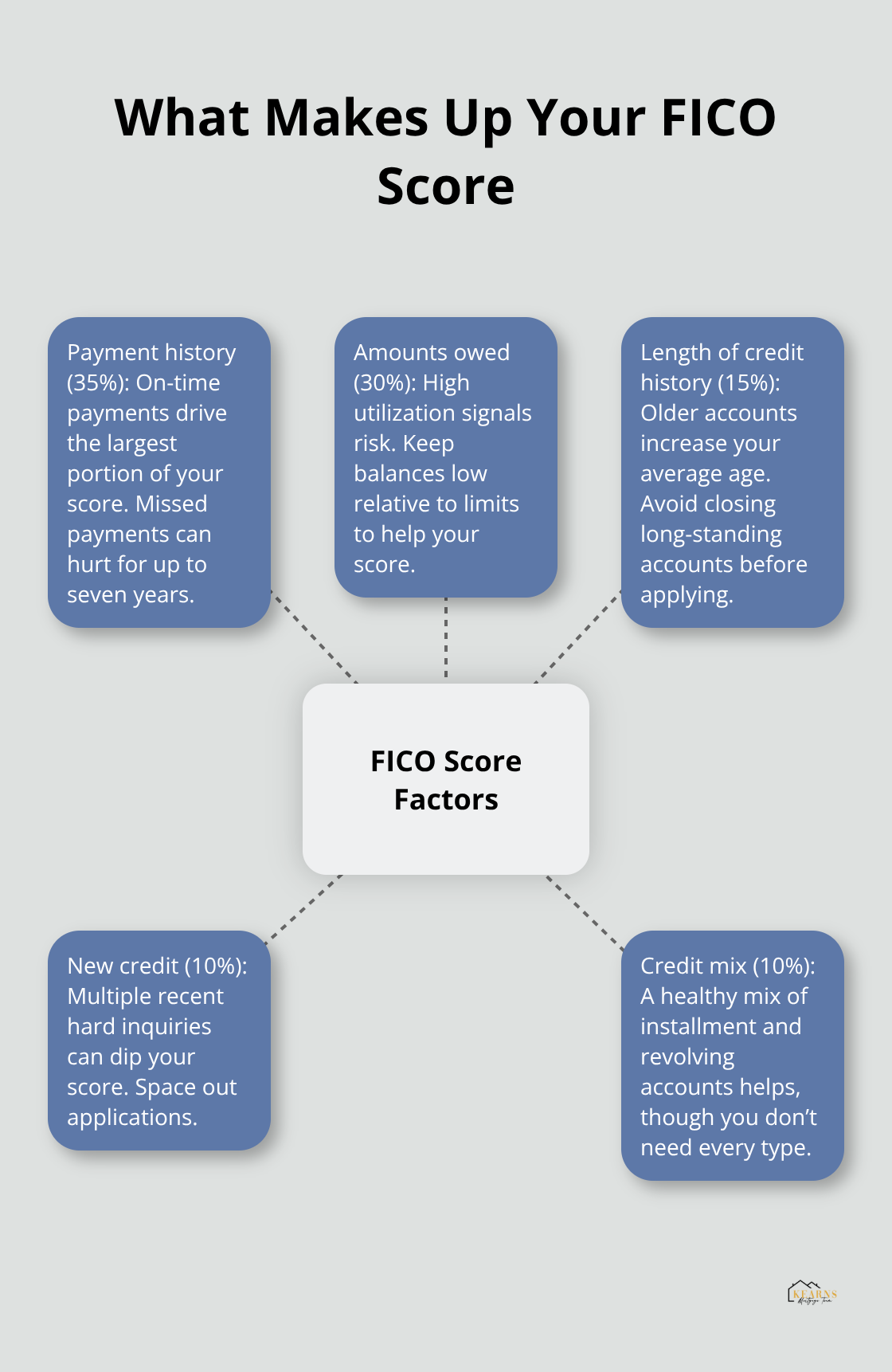

Lenders use your credit score as a risk assessment tool. When you apply for a mortgage, they’re not just looking at a single number-they’re evaluating whether you paid bills on time, how much debt you carry, and how long you’ve managed credit. Payment history accounts for 35 percent of your FICO score, making it the most important factor. A missed payment stays on your report for seven years, so lenders take this seriously. According to Experian, the national average credit score in 2024 was 715, and as of April 2025, borrowers obtaining purchase loans averaged around 737. If your score falls below that range, lenders will view you as higher risk, which directly affects what they offer you.

Your Credit Score and Credit Report Are Not the Same

Your credit score and credit report serve different purposes, though lenders examine both. Your credit report is a detailed history of your borrowing and payment behavior, pulled from Equifax, Experian, and TransUnion. Mortgage lenders typically use a tri-merge report that combines data from all three bureaus. Your credit score is a three-digit number calculated from that report. The composition breaks down as follows: payment history 35 percent, amount of debt 30 percent, length of credit history 15 percent, new accounts 10 percent, and credit mix 10 percent. You can access your actual credit reports free at AnnualCreditReport.com.

Credit score apps like Credit Karma help with monitoring, but they don’t show what lenders see. Lenders use FICO scoring models, and they typically rely on the middle score when three are available. Errors on your report directly hurt your score, so disputing inaccuracies is one of the fastest wins you can achieve.

How Your Score Translates to Real Dollars

The relationship between credit score and mortgage rate is direct and measurable. As of January 2026, borrowers with a score around 700 faced rates of approximately 6.58 to 6.62 percent on a 30-year conventional mortgage, translating to roughly $1,792 monthly on a $350,000 loan. Those with scores between 760 and 780 qualified for rates around 6.28 to 6.38 percent, lowering monthly payments to approximately $1,729 to $1,748. That’s a difference of $44 to $63 per month, which compounds to over $15,800 in savings across 30 years. Even small improvements matter-crossing from 718 to 720 can push you into a better rate tier.

Your Score Opens or Closes Loan Options

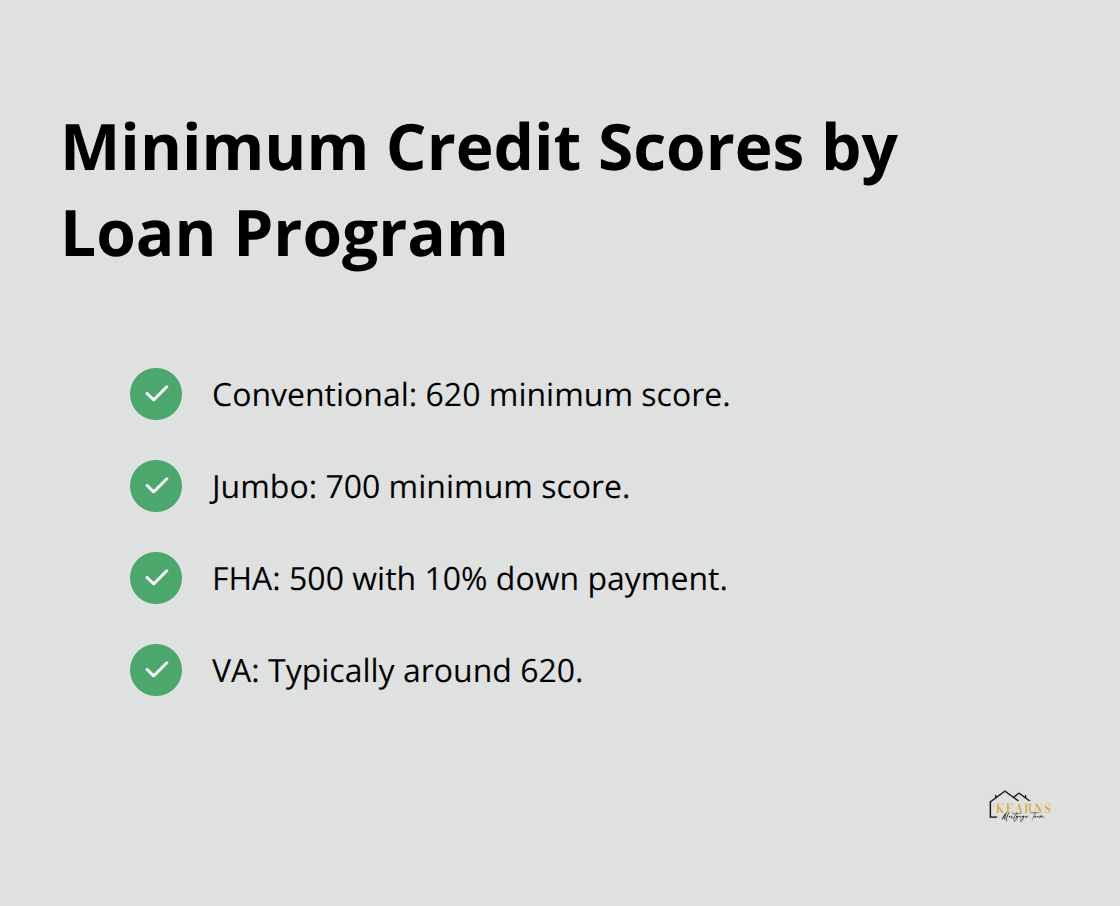

Your score determines which loan programs you can access. Conventional loans require a minimum 620, jumbo loans demand 700, FHA can work with scores as low as 500 with a 10 percent down payment, and VA loans typically start around 620. A higher score also improves your debt-to-income ratio flexibility, allowing lenders to approve you for larger loan amounts and sometimes waiving fees. Your score determines access to loan types, down payment requirements, and whether you’ll pay private mortgage insurance or mortgage insurance premiums.

These rate differences and loan options show why your next steps matter. The improvements you make now directly shape what you’ll qualify for when you’re ready to apply.

Quick Wins to Boost Your Credit Score

Lower Your Credit Utilization Immediately

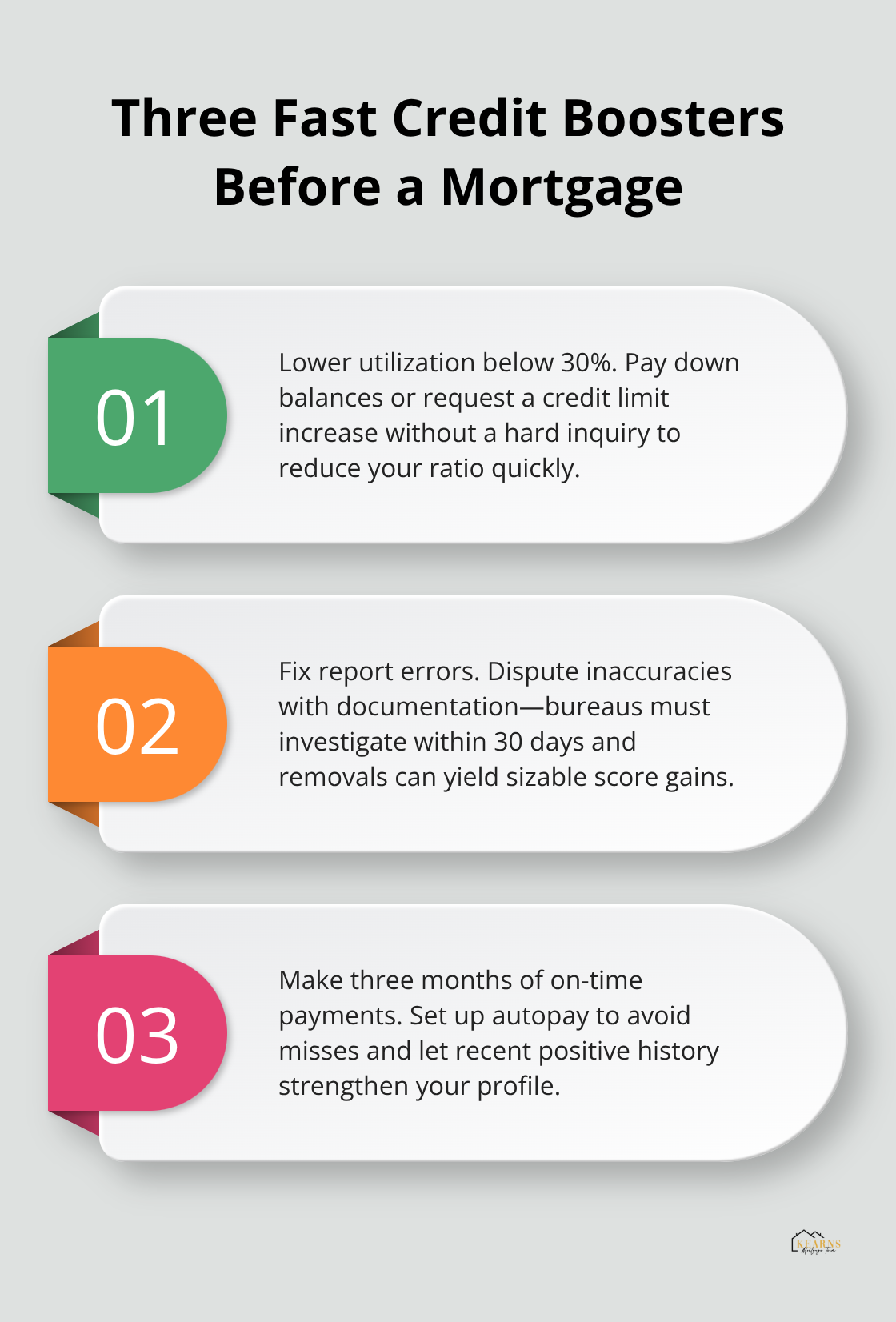

The fastest path to a higher credit score involves three concrete actions that show results within weeks rather than months. Credit utilization-the percentage of available credit you’re using-is the second-largest factor in your FICO score at 30 percent, and it responds immediately to your efforts. If you carry a $5,000 balance on a credit card with a $10,000 limit, you’re at 50 percent utilization. Lenders prefer to see this below 30 percent. Paying down that balance to $3,000 instantly improves your score because the calculation updates as soon as the creditor reports the change. This happens faster than waiting for payment history improvements.

One Reddit user documented a jump from 550 to 690 in two years through systematic debt reduction while maintaining on-time payments, proving that focused effort compounds. You don’t need to eliminate all revolving debt, just reduce your credit card balances below 30% of your limits. If you’re close to your limits, contact your card issuer and request a credit limit increase without a hard inquiry; this expands your available credit and lowers your utilization ratio instantly.

Fix Errors on Your Credit Report

Errors on your credit report directly sabotage your score, yet most people never check. Pull your reports from Equifax, Experian, and TransUnion at AnnualCreditReport.com and examine them carefully for accounts you don’t recognize, incorrect payment statuses, or duplicate entries. Disputing inaccuracies on your credit report takes about 15 minutes per error, and the bureaus must investigate within 30 days. Removing a false late payment or a fraudulent account can jump your score 50 to 100 points.

Establish Three Months of Perfect Payments

Simultaneously, commit to three consecutive months of on-time payments starting immediately. This matters because payment history carries the most weight at 35 percent of your score. Set up automatic payments for at least the minimum amount on every account-credit cards, loans, utilities, everything.

Late payments stay on your report for seven years, so one missed payment now costs you for years. After three months of perfect payments, lenders see you as lower risk, and your score begins climbing.

These quick wins create momentum, but your credit profile needs deeper reinforcement to withstand the scrutiny of mortgage underwriting.

Strategic Long-Term Steps to Strengthen Your Credit Profile

Use Secured Credit Cards to Build History

A secured credit card works by requiring you to deposit cash as collateral, typically between $200 and $2,500, which becomes your credit limit. This tool matters because it creates a tradeline that reports to all three bureaus, extending your credit history length, which accounts for 15 percent of your FICO score. The card issuer holds your deposit in a savings account while you use the card normally, making small purchases and paying the balance in full each month. After 6 to 12 months of perfect payments, many issuers graduate you to an unsecured card and return your deposit. This approach works especially well if you’re rebuilding after past mistakes or have a thin credit file.

Treat the secured card exactly like any other card-never miss a payment, keep utilization below 30 percent, and don’t close it once upgraded. Closing accounts shortens your average account age and raises your utilization ratio, both of which harm your score.

Stop Opening New Accounts Before You Apply

Every new credit application triggers a hard inquiry that temporarily lowers your score by a few points, and new accounts lower your average account age. If you open three new credit cards in six months while preparing for a mortgage, lenders see someone taking on additional risk right before borrowing $300,000. Instead, work with what you have and resist the urge to improve your profile by adding accounts.

Monitor Your Credit Quarterly for Errors and Fraud

Check your actual credit reports from Equifax, Experian, and TransUnion quarterly, not monthly, because checking your own reports causes no hard inquiry and helps you spot fraud or errors before they sabotage your application. If you find an error, dispute it immediately through the bureau’s website or by mail, providing documentation that supports your claim. The bureaus must investigate within 30 days and remove unverified information. This systematic approach-secured cards for those who need them, zero new accounts, and quarterly monitoring-positions your credit to withstand mortgage underwriting without last-minute surprises.

Final Thoughts

The work you do to improve credit for mortgage approval translates directly into tangible savings and expanded options when you apply. A score improvement of just 40 points can lower your monthly payment by $44 to $63 and save you over $15,000 across 30 years. More importantly, a stronger credit profile unlocks access to loan programs you might not qualify for today and positions you to negotiate better terms with lenders.

Before you meet with a mortgage professional, take action on what you’ve learned here. Pull your credit reports from all three bureaus, dispute any errors you find, and commit to three months of perfect on-time payments. Pay down your credit card balances below 30 percent utilization, and if you have a thin credit history, open a secured credit card and use it responsibly. Avoid opening new accounts or applying for new credit in the months leading up to your mortgage application-these steps cost nothing and require only consistency.

Your path to homeownership starts with financial preparation, and that preparation begins with your credit. When you’re ready to take the next step, connect with our team for a free consultation and discover which loan options align with your financial goals and timeline.