Florida’s real estate market is shifting fast in 2026, and whether you’re buying your first home or expanding an investment portfolio, understanding these changes matters. Interest rates, population trends, and climate considerations are reshaping how people approach property decisions across the state.

At Kearns Mortgage Team, we’ve seen firsthand how quickly buyer priorities evolve. This guide breaks down what’s actually happening in Florida’s market right now and what it means for your next move.

What’s Driving Florida’s 2026 Real Estate Shift

Mortgage Rates Open the Door for Buyers

Mortgage rates have eased to around 6% after sitting near 6.8% in 2024, and this matters more than you might think. Florida Realtors reports that single-family home sales jumped 5.9% year-over-year in January 2026, while pending contracts-homes under contract waiting to close-surged 15.2%. That’s real momentum, not speculation. The data shows six consecutive months of year-over-year gains in pending sales, which means buyer activity accelerates into spring. Lower rates pull buyers off the sidelines. A 1 percentage-point drop in mortgage rates could expand the national buyer pool by roughly 5.5 million households, according to the National Association of Realtors. For Florida specifically, that translates to meaningful competition for properties and faster-moving sales.

If rates continue easing toward 5.5% or lower in 2026, monthly payments drop further, which expands what middle-income buyers can actually afford. Right now, middle-income buyers can afford only about 21% of homes for sale nationally, so any payment relief matters significantly. Lower monthly payments directly translate to purchasing power-something that shifts the entire market dynamic when rates move in the right direction.

Inventory Reaches Historic Levels

Florida’s inventory situation is shifting, and this changes the game for both buyers and investors. New listings hit their highest January level since 2008, according to Florida Realtors. In Central Florida specifically, new listings jumped 59% from December to January, and homes on the market averaged 81 days-the highest this decade. That’s a stark contrast to the tight seller’s market of recent years. Inventory growth has slowed its acceleration, meaning the market absorbs listings more efficiently rather than sitting on excess stock.

This rebalancing favors buyers who now have genuine options and can negotiate better terms. Population growth continues to drive demand, particularly from remote workers and retirees relocating to Florida. However, the incoming supply finally catches up, which means buyers shouldn’t feel pressured into snap decisions anymore.

What This Means for Your Investment Strategy

For investors, this environment rewards selectivity. Cash flow potential exists in emerging neighborhoods where new listings are appearing, but you need to analyze actual rental rates and tenant demand rather than assuming appreciation will carry the deal. The days of passive wealth-building through property appreciation alone are over; your investment thesis must include solid rental income fundamentals.

The shift toward inventory balance creates opportunities for investors willing to focus on neighborhoods with strong rental demand and reasonable entry prices. Properties that generate consistent monthly cash flow (not just future price gains) become the foundation of a resilient portfolio. As we move into the spring buying season, understanding which neighborhoods attract renters and which attract owner-occupants will separate successful investors from those chasing outdated strategies.

What You Need to Know About Buying in Florida Right Now

Understanding Regional Price Variation

Florida’s median home prices sit at $405,000 for single-family homes according to January 2026 data from Florida Realtors, but these numbers mask significant regional variation. Prices in Miami-Dade and Broward counties run substantially higher than inland markets like Polk or Osceola counties, where inventory is fresher and entry points lower. Focus on the specific neighborhood where you want to live rather than anchoring to state averages. Compare what similar properties sold for in the past 30 days, not 6 months ago. Homes on the market average 81 days in Central Florida, which gives you real negotiating room that didn’t exist two years ago. This longer timeframe means sellers increasingly offer concessions like closing cost assistance or repairs, which directly reduces your out-of-pocket expense.

Evaluating Climate Risk and Property Resilience

When you evaluate a property, factor in climate risk honestly. Properties in flood zones cost more to insure and may face future financing restrictions. Get a flood zone determination from FEMA before making an offer, and request a flood insurance quote separately from your homeowners insurance estimate. Properties outside high-risk flood zones typically appreciate more predictably and attract broader buyer pools when you eventually sell. Climate considerations aren’t speculation anymore-they’re financial reality in Florida.

Securing the Right Financing Strategy

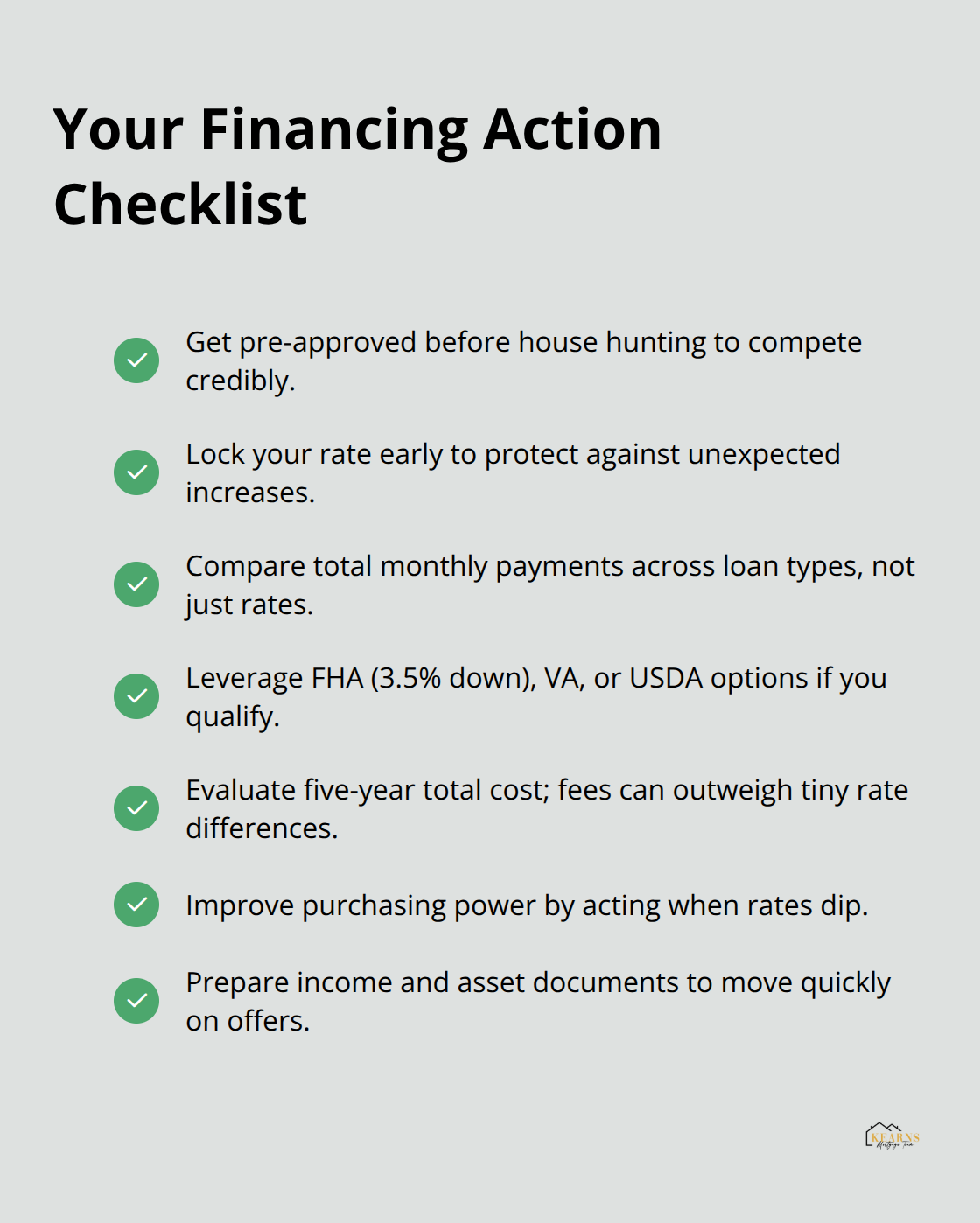

Your financing strategy determines whether you actually win a property in this market. Mortgage rates around 6% mean a 1 percentage-point drop expands your purchasing power by roughly $40,000 on a $300,000 loan. Get pre-approved before house hunting, not after finding something you like.

A pre-approval letter shows sellers you’re serious and gives you 30 days to lock your rate, protecting you if rates climb unexpectedly. Middle-income buyers nationally can afford only about 21% of homes for sale, according to the National Association of Realtors, so every dollar of purchasing power matters.

Conventional loans typically offer the best rates right now, but if you’re a first-time buyer with limited down payment funds, FHA loans allow 3.5% down and may cost less upfront than saving for 10% or 20% down. VA and USDA loans offer zero-down options if you qualify. The wrong loan type costs you thousands in interest over 30 years. Compare actual monthly payments across loan types, not just interest rates. A loan with a slightly higher rate but lower closing costs sometimes costs less over five years than a low-rate loan with expensive fees.

Moving Fast in a Competitive Market

Florida Realtors data shows six consecutive months of year-over-year gains in pending sales, meaning competition remains real even with improved inventory. Lock your rate early in the process, and don’t assume rates will drop further just because they’ve eased to 6%. If you find the right property at the right price, securing financing quickly separates successful buyers from those who hesitate and lose deals. With spring buying season approaching and pending contracts accelerating, your next decision point arrives sooner than you might expect.

Investment Opportunities in Florida’s Shifting Market

Target Neighborhoods Where Rental Demand Stays Strong

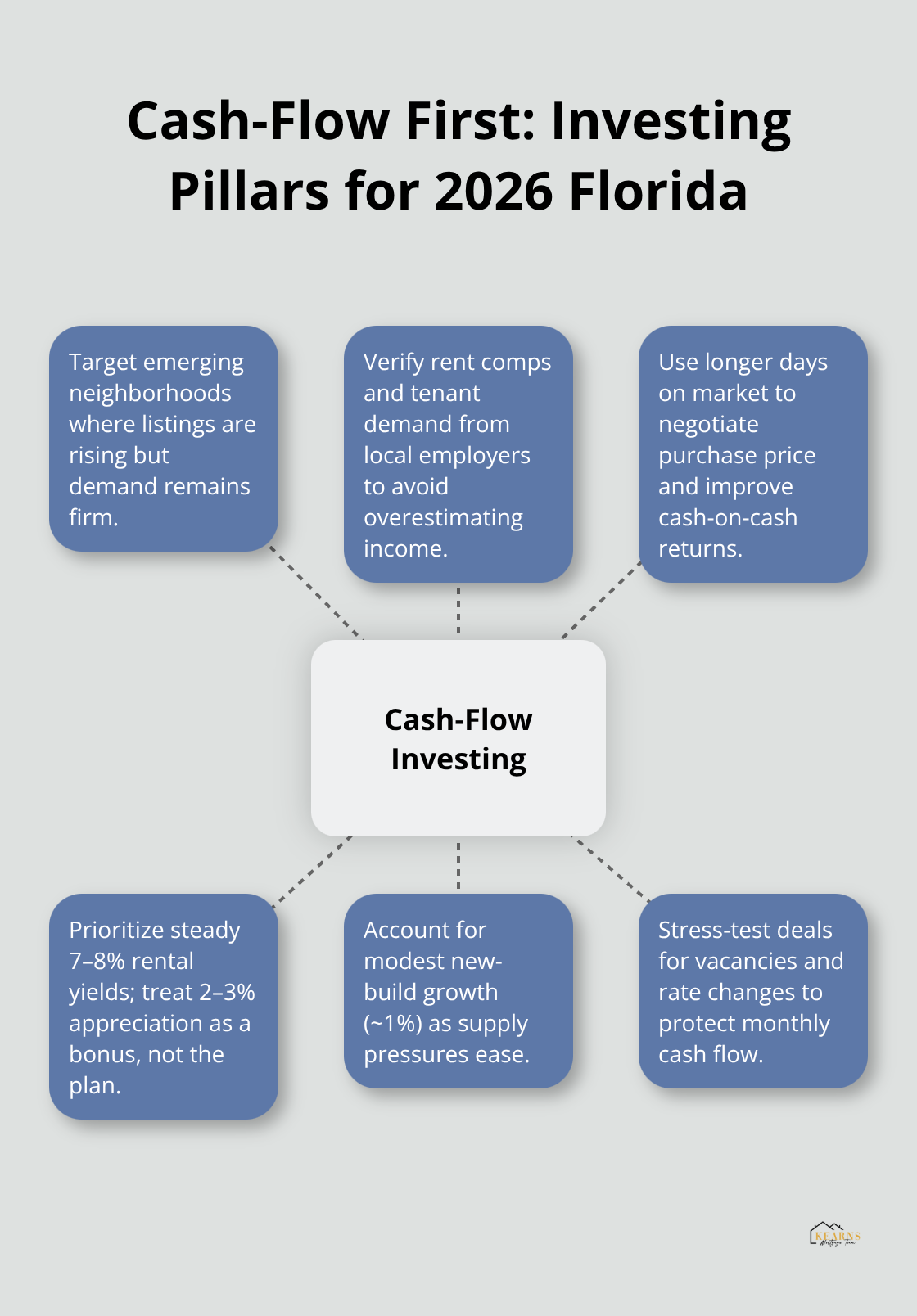

Florida’s rental market strength in 2026 depends entirely on which neighborhoods you target and what tenant demand actually looks like on the ground. Central Florida exemplifies this perfectly. January 2026 brought 59% more new listings month-over-month, yet pending contracts jumped 24% in the same period, according to Orlando Regional Realtor Association data.

This tells you something critical: buyers move faster than sellers list, which means rental demand remains robust in neighborhoods where inventory is still tight.

Metropolitan areas like Tampa, Miami, and Jacksonville continue attracting remote workers and retirees, but the incoming supply finally gives you options beyond overpriced properties in saturated neighborhoods. Try emerging areas where new listings appear but rental demand hasn’t collapsed yet. Properties averaging 81 days on market in Central Florida create opportunities to negotiate better purchase prices, directly improving your cash-on-cash returns. If you purchase at 15% below asking price in a neighborhood with stable 7–8% annual rental yields, your actual return compounds faster than someone overpaying in a hot market.

Focus on Cash Flow Over Appreciation

Long-term appreciation in Florida remains modest at roughly 2–3% annually according to forecasts from the National Association of Realtors, which means counting on price gains alone will disappoint you. The real wealth-building happens through monthly cash flow from tenants, not speculation on future sale prices. Properties in neighborhoods with strong employer presence-tech hubs in Tampa, healthcare corridors in Jacksonville, hospitality areas near theme parks-attract renters consistently regardless of market cycles.

Builders expect only 1% growth in single-family construction in 2026, so the supply shortage that supported appreciation for years is finally easing. Your investment thesis must include solid fundamentals: actual rental rates in the neighborhood, tenant demand from local employers, and realistic vacancy rates. Properties that produce $2,000 monthly rent on a $300,000 purchase price (with a $250,000 mortgage) generate real cash flow immediately, not theoretical gains years from now.

Adapt Your Strategy to Market Maturity

This shift toward income-focused investing separates successful investors from those chasing vanishing appreciation strategies as Florida’s market matures. New investors cannot rely on old playbooks that worked when supply was scarce and prices climbed automatically. The market has changed, and your approach must change with it. Properties that generate consistent monthly income become the foundation of a resilient portfolio in 2026 and beyond.

Final Thoughts

Florida’s real estate outlook for 2026 shows a market that has shifted from scarcity to balance, and that transformation changes everything about how you approach buying or investing. Mortgage rates around 6% have pulled buyers off the sidelines, pending contracts climb month-over-month, and inventory finally gives you genuine options instead of forcing rushed decisions. For buyers, this means you can negotiate better terms, compare properties across neighborhoods, and avoid overpaying out of desperation. For investors, the appreciation-driven playbook of recent years no longer works-your focus must shift to properties that produce solid monthly cash flow from day one.

Single-family home sales jumped 5.9% year-over-year in January 2026, while new listings hit their highest January level since 2008, and homes averaging 81 days on market in Central Florida give you real negotiating power. Middle-income buyers can afford only about 21% of homes for sale nationally, so every dollar of purchasing power matters when you compete for properties. If rates continue easing toward 5.5% or lower, your monthly payments drop further, which expands what you can actually afford.

Your next move depends on getting your financing strategy right from the start, whether you’re a first-time buyer exploring FHA options or an investor analyzing cash flow potential. At Kearns Mortgage Team, we help you compare loan types, lock favorable rates, and understand exactly what you can afford before you start house hunting through personalized mortgage solutions including Conventional, VA, FHA, and USDA loans tailored to your specific situation. What property generates the monthly income you need, and can you afford this payment if rates climb another half-point?