Growing a business in Tampa often means finding the right financing to fuel expansion. Commercial mortgage loans in Tampa FL offer business owners a practical path to acquire property, secure capital, and build lasting assets.

We at Kearns Mortgage Team understand that navigating commercial financing can feel overwhelming. This guide walks you through everything you need to know about qualifying, the benefits, and what makes commercial mortgages work for Tampa businesses.

How Commercial and Residential Loans Work Differently in Tampa

Commercial mortgage loans operate on fundamentally different underwriting principles than residential mortgages, and understanding this distinction matters for Tampa business owners. Lenders evaluate commercial properties primarily on cash flow and property performance rather than your personal income alone. This means a strong rent roll, solid operating statements, and consistent tenant leases carry more weight than your salary or W-2s. Tampa commercial lenders typically require a personal financial statement, schedule of real estate owned, and credit scores, but the property itself becomes the central focus of approval.

Down Payments and Loan-to-Value Ratios

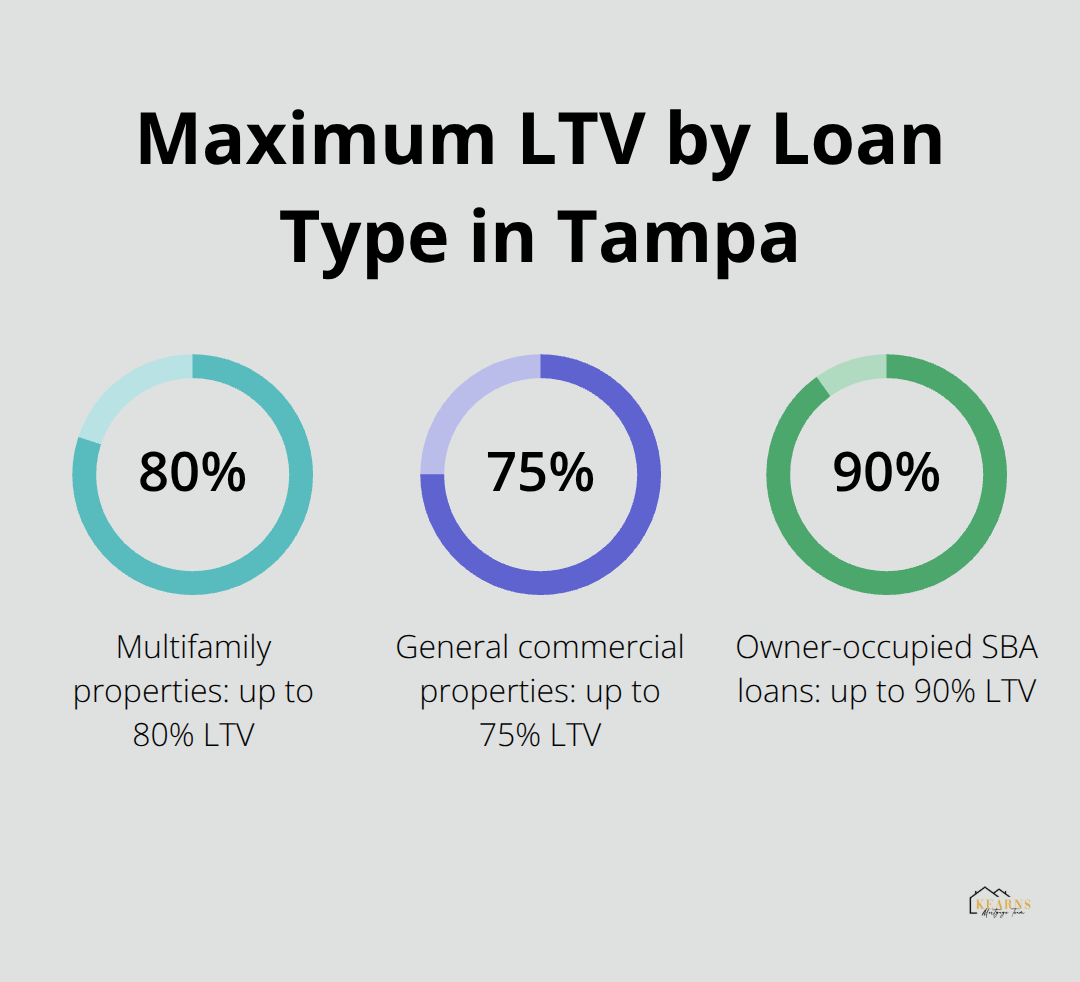

You’ll notice commercial loans demand larger down payments than residential mortgages. Apartments generally require 20 to 25 percent down, while other commercial properties typically require 25 to 30 percent. The loan-to-value ratios reflect this reality: multifamily properties max out at 80 percent LTV, general commercial at 75 percent, and owner-occupied SBA loans can reach 90 percent LTV. These requirements protect lenders while giving you skin in the game, which strengthens your commitment to the property’s success.

Current Tampa Rates and Market Conditions

Current Tampa rates as of January 2026 show multifamily loans at 5.11 percent up to 80 percent LTV, commercial real estate loans at 6.17 percent up to 75 percent LTV, and business real estate loans at 5.97 percent up to 90 percent LTV. These rates reflect the property’s debt service coverage ratio, location, and your experience as a borrower. Tampa’s commercial real estate market spans apartments, office, retail, industrial, self-storage, and hospitality sectors, each with distinct financing pathways. The 2025 Tampa market outlook projects investment sales could rise up to 10 percent, with cap rate compression across most sectors. Industrial properties saw the sharpest compression at 30 basis points, followed by retail at 24 basis points and multifamily at 17 basis points. Self-storage remains particularly strong in Florida, which holds the third-highest number of facilities nationally according to the Self Storage Association.

Loan Structure and Flexibility

Minimum loan size for Tampa commercial financing sits at 1.5 million dollars, which eliminates smaller deals but allows lenders to focus resources on substantial projects. Amortization extends up to 30 years with fixed-rate terms commonly available for 5, 7, or 10 years, giving you flexibility in structuring repayment around your business projections. Office space has faced headwinds from remote work trends but continues to attract financing in urban centers. Understanding which property type you’re financing shapes everything from approval timelines to the specific documentation lenders require.

Rate Drivers and What Affects Your Quote

Your Tampa commercial mortgage rate depends on multiple interconnected factors that go well beyond a simple credit score. Property type, location within Tampa, LTV, debt service coverage ratio, debt yield, borrower net worth, liquidity, credit rating, and your real estate experience all influence pricing. Lower-risk profiles typically yield better rates, so demonstrating strong property fundamentals and substantial personal reserves strengthens your negotiating position. Higher deficits and ongoing tariff policy changes keep rates elevated, meaning long-term borrowers benefit from locking in fixed terms now rather than betting on future rate drops. Rate-locking practices vary by lender: some lock at application, some at commitment, and others only before closing, so clarifying this policy upfront prevents surprises at the closing table.

Capital Sources and Pre-Approval Process

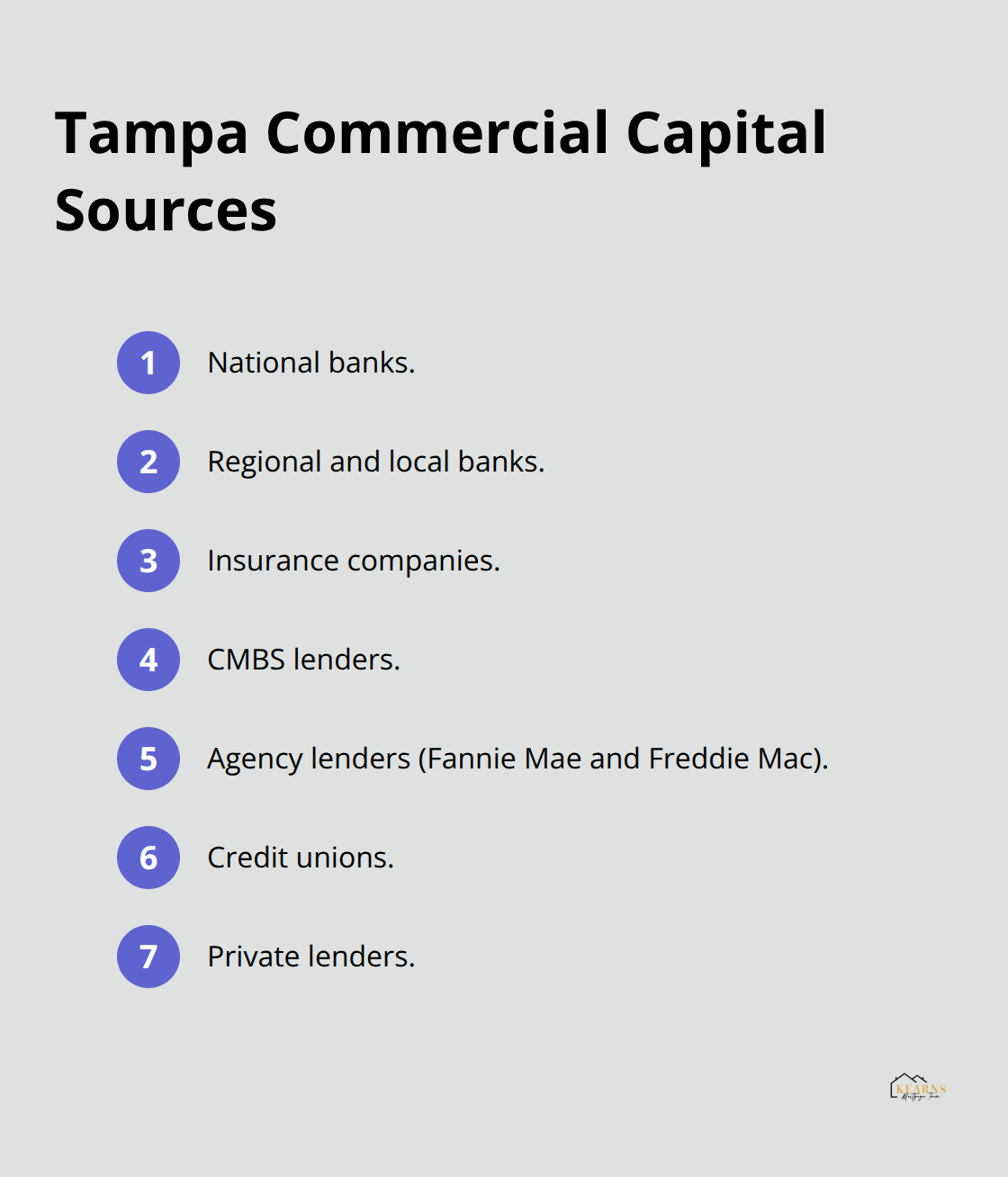

Tampa lenders draw from multiple capital sources including national banks, regional and local banks, insurance companies, CMBS, agency lenders like Fannie Mae and Freddie Mac, credit unions, and private lenders. This diversity means shopping your deal across different lender types can uncover significantly better terms.

Most Tampa commercial lenders offer 24-hour pre-approvals at no cost with no obligation and no upfront application fees, allowing you to test your borrowing power without financial commitment. Typical closings happen within about 45 days once you enter the formal approval process. With these rate drivers and capital sources in mind, the next step involves understanding what documentation lenders actually need from you to move forward with your application.

Why Commercial Mortgages Build Real Business Wealth

Commercial mortgage loans in Tampa don’t just fund a purchase-they fundamentally reshape how your business builds wealth over time. When you finance a property through a commercial mortgage rather than renting, every payment builds equity that stays with your company. A Tampa business owner financing a $2 million property at 6.17 percent over 10 years accumulates substantial ownership stake while locking in predictable costs. Rent, by contrast, climbs with market conditions and landlord decisions, leaving no residual asset for your business. This equity accumulation compounds significantly over the 5, 7, or 10-year fixed-rate terms available in Tampa’s market.

Tax Advantages That Reduce Your Real Costs

Commercial real estate financing unlocks tax advantages that residential borrowing cannot match. Interest payments on commercial mortgage interest deductions become fully deductible business expenses, reducing your taxable income dollar-for-dollar. Property depreciation also generates deductions that shelter income without requiring cash outlay-a benefit residential homeowners cannot claim. Operating expenses tied to the property (maintenance, utilities, property taxes, insurance) become deductible business costs when you own rather than rent. Tampa business owners who understand these tax mechanics often find that commercial financing costs less in real terms than the rent they would otherwise pay, because the mortgage interest and depreciation shield significant income from taxation.

Capital Access Without Diluting Ownership

Securing a commercial mortgage preserves complete ownership and control of your business. Unlike equity investors or venture capital, which demand ownership stakes and decision-making authority, a mortgage lender has no claim on your operations or profits beyond the agreed-upon payments. This distinction matters enormously for Tampa entrepreneurs building long-term enterprises. You retain 100 percent of business growth, profit, and exit value while using borrowed capital to acquire the real estate that houses your operations. The minimum loan size of $1.5 million in Tampa means serious borrowers access meaningful capital without the complications of smaller lenders or predatory terms. With amortization extending to 30 years, monthly payments remain manageable even on substantial loan amounts, preserving cash flow for operations, payroll, and growth investments. The ability to lock fixed rates now protects your business from future rate volatility-a critical advantage given that higher deficits and tariff policy changes continue keeping rates elevated. A business that secures a 5-year fixed rate today avoids the risk of refinancing into a higher-rate environment in 2031.

Competitive Advantage Through Owned Real Estate

Tampa commercial real estate ownership creates competitive advantages that renters cannot match. Owned properties provide collateral for future business financing, equipment loans, or working capital lines that would be unavailable to companies without hard assets. Property appreciation in Tampa real estate market builds net worth independently of business performance, with moderate annual appreciation of 3–5% expected in prime zip codes. If your business encounters a temporary downturn, owned real estate retains value and can be refinanced or sold to stabilize operations. Renters facing similar challenges have no comparable asset to leverage. This appreciation creates wealth multiplication that pure business operations alone rarely achieve.

Understanding how commercial mortgages transform your financial position sets the stage for the next critical question: what does the actual approval process look like, and what documentation do Tampa lenders require from you to move forward?

Getting Approved for a Commercial Mortgage in Tampa

Documentation That Lenders Actually Review

Qualifying for a commercial mortgage in Tampa requires presenting lenders with specific financial documentation that proves both your creditworthiness and the property’s income potential. Lenders request your personal financial statement, a schedule of real estate owned, and your credit scores upfront, but here’s where commercial lending diverges sharply from residential: they care far more about what the property generates than what you earn personally. You’ll need the subject property’s rent roll showing current tenants and lease terms, detailed operating statements for the past two to three years, and copies of actual leases. This documentation reveals whether the property produces enough cash flow to service the debt comfortably.

A debt service coverage ratio above 1.25 significantly strengthens your application, meaning the property’s annual net operating income covers the annual debt service by at least 25 percent. Lenders examine this metric ruthlessly because it predicts whether you’ll actually make payments when business cycles turn downward. If your property generates $500,000 in annual net operating income, lenders want annual debt service around $400,000 or less. This isn’t theoretical-it directly determines your maximum loan amount and interest rate.

How DSCR and Property Performance Drive Your Rate

Stronger DSCR numbers unlock lower rates, sometimes by 50 basis points or more compared to borderline applicants. Tampa’s minimum loan size of $1.5 million means lenders dedicate serious underwriting resources to your deal, so expect thorough scrutiny. Gather two to three years of operating statements, tax returns, and lease documents before approaching lenders. Many Tampa business owners waste time submitting incomplete applications that get rejected, then reapply weeks later. Having everything organized upfront accelerates the 24-hour pre-approval process and demonstrates professionalism that lenders reward.

The Appraisal Process and What It Means for Your Loan

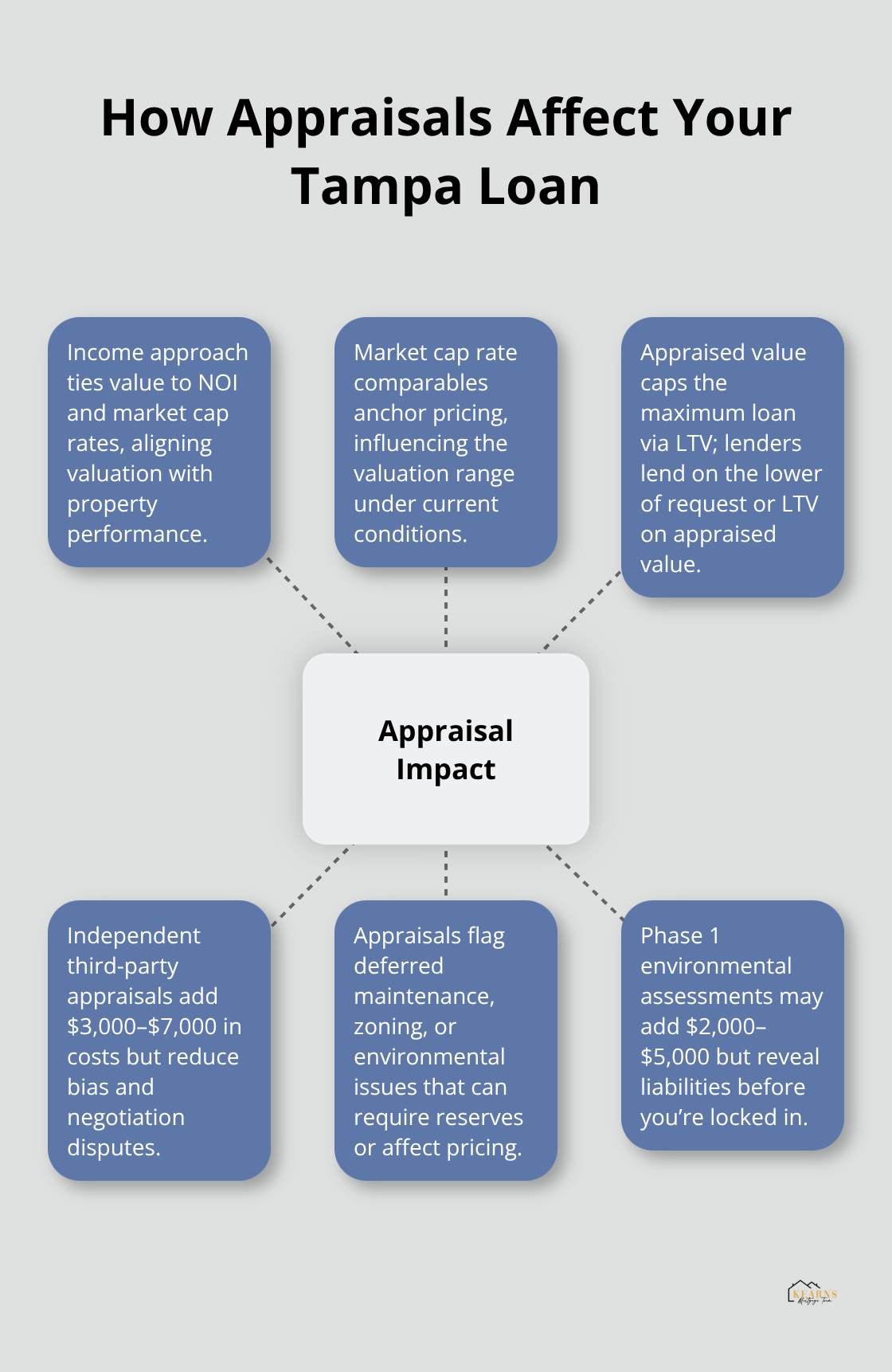

Property appraisals in Tampa commercial lending follow a different methodology than residential valuations and directly impact your loan amount. Lenders employ the income approach, comparing your property’s net operating income to similar properties’ cap rates in your market. If comparable Tampa office buildings trade at 6.5 percent cap rates and your property generates $300,000 NOI, the appraisal typically supports a $4.6 million valuation. This matters enormously because your maximum loan amount depends on the lower of your requested amount or the appraised value multiplied by your LTV.

A property appraising at $3 million with 75 percent LTV allows $2.25 million in financing, regardless of how much you hoped to borrow. Third-party appraisers cost $3,000 to $7,000 depending on property complexity, and lenders order these independently-you cannot influence the outcome. This is actually beneficial because it removes subjective negotiation from the equation.

The appraisal also identifies deferred maintenance, zoning issues, or environmental concerns that might require reserves or affect pricing. Some Tampa commercial properties carry Phase 1 environmental assessments that can add $2,000 to $5,000 to your closing costs but reveal hidden liabilities before you’re locked into a mortgage.

Working with Local Tampa Lenders

Working with experienced Tampa lenders who understand local market comparables accelerates appraisal timelines and prevents delays from unrealistic appraisal expectations. Once your financial documentation is complete and the property appraises, lenders move to underwriting and final approval, which typically closes within 45 days from formal application. Loan products, terms, and availability are subject to credit approval, so ensure all documentation meets lender standards before submission.

Final Thoughts

Commercial mortgage loans in Tampa FL represent a strategic decision that separates businesses building lasting wealth from those stuck in perpetual rent cycles. You acquire a tangible asset, lock in predictable costs through fixed-rate terms, and accumulate equity that strengthens your balance sheet year after year. Tax deductions on interest and depreciation reduce your real borrowing costs, while property appreciation builds net worth independent of business performance.

The path forward starts with honest assessment of your business needs and financial position. You need two to three years of operating statements ready to present, documented debt service coverage above 1.25, and preparation for a 20 to 30 percent down payment depending on property type. Tampa’s minimum loan size of $1.5 million means serious capital is available, but lenders expect serious documentation in return.

We at Kearns Mortgage Team provide expert guidance and personalized mortgage solutions designed to make the financing process clear and achievable. Contact our team to explore whether commercial mortgage loans in Tampa FL align with your business growth goals. What would your business look like in five years if you owned the property you operate from rather than renting it?