Investment properties can generate significant income, but financing them works differently than buying a primary home. Lenders impose stricter requirements, higher down payments, and more rigorous understandings of your financial situation.

We at Kearns Mortgage Team help investors navigate how to finance an investment property with clarity and confidence. This guide walks you through loan types, qualification standards, and strategies to maximize returns while managing risk.

Financing an Investment Property: Loan Types and Lender Selection

What Loan Options Work Best for Investment Properties

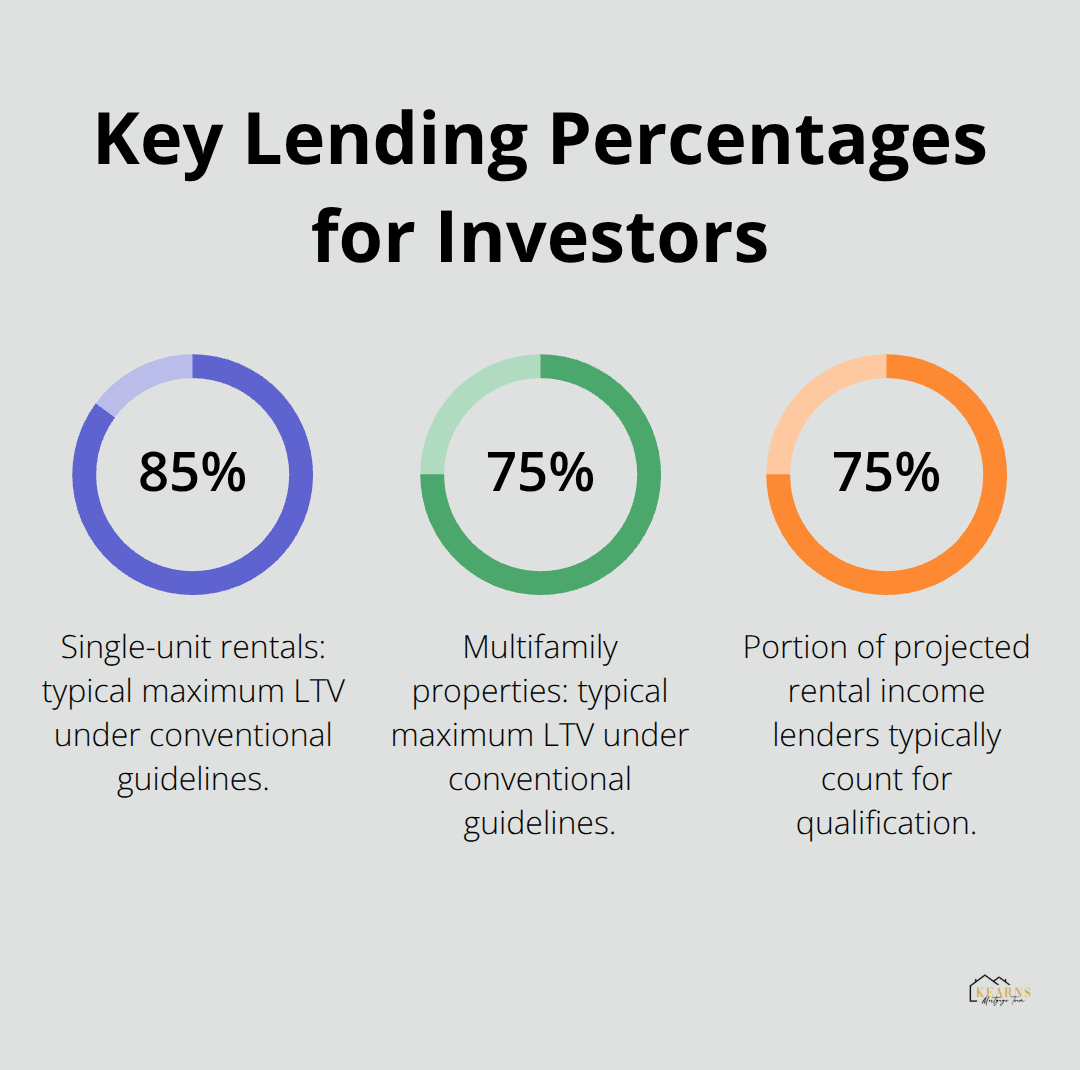

Conventional loans dominate investment property financing because they allow up to 85% loan-to-value on single-unit rentals and 75% on multifamily properties, according to Fannie Mae and Freddie Mac guidelines. This means you’ll typically need 15-25% down, with most lenders capping at 80% LTV since private mortgage insurance isn’t available for investment properties. The trade-off is real: investment property rates run 0.5-0.75 percentage points higher than owner-occupied loans. At a 60% loan-to-value ratio, you’ll face a risk-based pricing adjustment around 1.125% of the loan amount; at 80% LTV, that jumps to roughly 4.125%, effectively pricing in the lender’s perception of default risk.

Fixed-rate mortgages offer predictability, but adjustable-rate mortgages start lower and can work if you plan to sell or refinance before rates reset. Hard money loans from private lenders serve a specific purpose: bridge financing for flips or properties that won’t qualify conventionally, though you’ll pay 8-15% interest and 2-4 points upfront. Seller financing bypasses traditional underwriting entirely, letting the property owner act as lender with negotiable terms and faster closings, but you’ll need strong legal counsel to protect yourself against default complications.

How Investment and Primary Residence Financing Differ

Lenders scrutinize investment properties with a lens focused on cash flow sustainability, not just your personal creditworthiness. They want to see a Debt Service Coverage Ratio of at least 1.2, meaning the property’s net operating income must cover 120% of annual mortgage payments. For primary residences, lenders count 100% of your employment income; for rentals, they typically count only 75% of projected rental income to account for vacancies and collection risk.

Your debt-to-income ratio must stay around 36-43% for investment properties, compared to 43-50% for owner-occupied homes, leaving less room for other debts. You’ll also need six months of mortgage payment reserves sitting in the bank, and for larger loans or higher-risk profiles, lenders demand twelve months. Documentation requires more depth: expect requests for two years of tax returns, proof of property management experience, and detailed rent estimates or existing leases. The underwriting process takes 30-45 days instead of the typical 21 days for primary mortgages. Credit score minimums hover around 620-640, but stronger scores below 680 often require that 25% down payment, whereas 680+ opens doors to 15% down options.

Finding the Right Lender for Your Situation

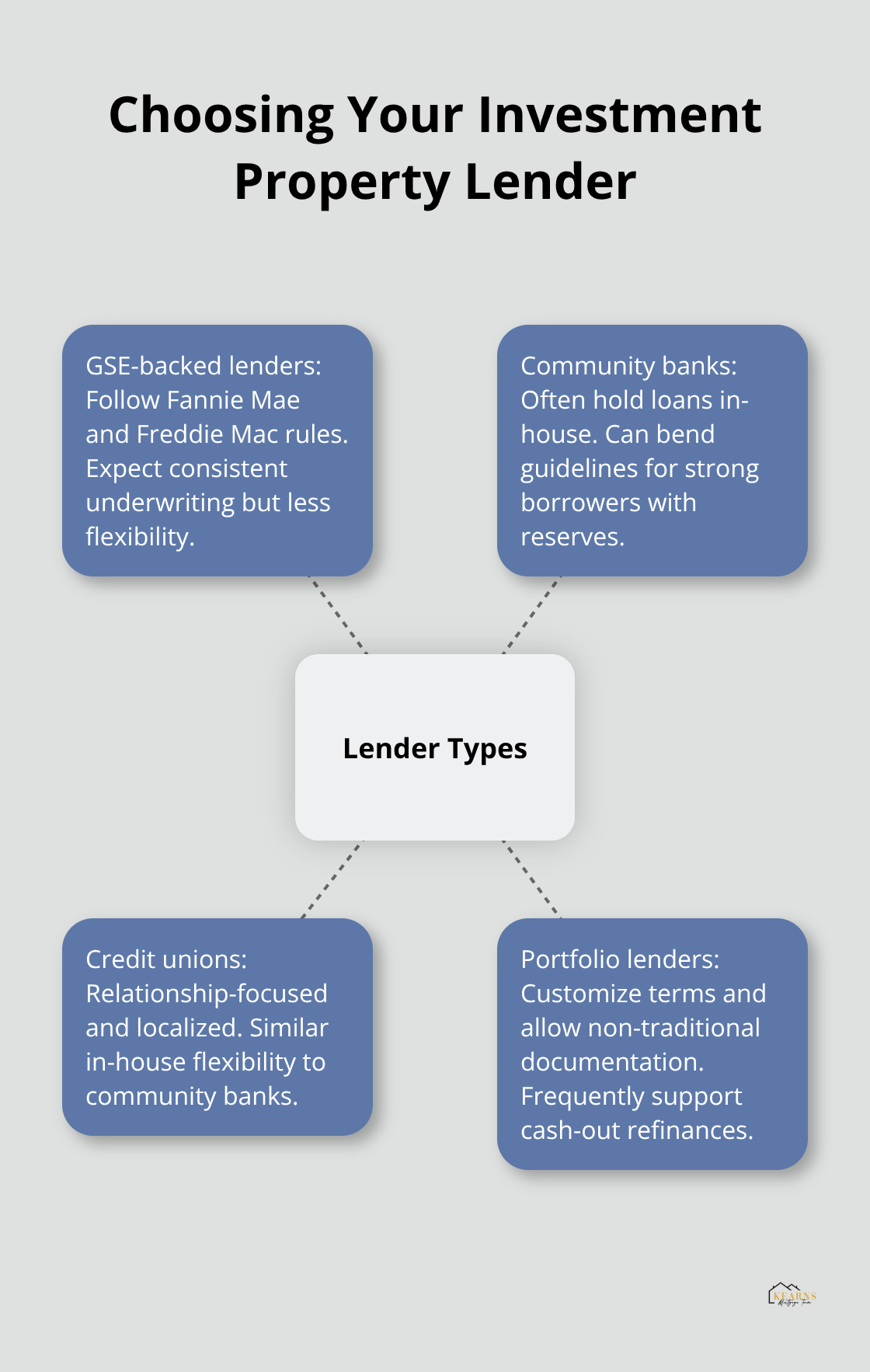

Not all lenders treat investment properties equally. Large banks and GSE-backed lenders follow rigid Fannie Mae and Freddie Mac rules, which means consistency but less flexibility. Local community banks and credit unions often hold loans in-house rather than selling them, giving loan officers authority to bend guidelines for strong borrowers with multiple properties or significant reserves. Portfolio lenders pride themselves on customization, allowing cash-out refinances, non-traditional income documentation, and terms tailored to your portfolio’s maturity.

If you’re buying a duplex, triplex, or fourplex and living in one unit, you can finance it as a primary residence, dramatically easing down payment and reserve requirements. This house-hacking strategy opens conventional financing at 3-5% down rather than 20%, though you must genuinely occupy one unit for at least one year. Shopping across five to seven lenders reveals rate differences of 0.5-1.0 percentage points, translating to thousands in savings over the loan term. Ask each lender about their investment property volume, typical turnaround time, and whether they service loans in-house or sell them.

Building Your Lender Relationship

The lender relationship matters as much as the rate: you’ll benefit from someone who understands your long-term portfolio goals and can guide you through future refinances or acquisitions. A mortgage professional who specializes in investment properties can help you evaluate which loan structure aligns with your timeline and risk tolerance. They’ll also explain how different down payments, reserve amounts, and credit profiles affect your approval odds and final rate. With the right lender in your corner, you’ll move forward with confidence into the financial qualification process.

Financial Requirements and Qualification Process

Down Payment: Your First and Most Important Hurdle

Lenders evaluate investment property applicants through a different financial lens than primary home buyers, and understanding exactly what they measure saves you time and money. Down payment matters most because it directly signals your commitment and reduces lender risk; conventional investment loans require 15% down on single-unit properties, with most lenders capping at 80% loan-to-value since private mortgage insurance doesn’t exist for rentals. If you finance a duplex, triplex, or fourplex and occupy one unit, you can drop that to 3.5% down by qualifying as owner-occupied, but you must genuinely live there for at least one year. This house-hacking strategy opens doors that traditional investment financing keeps closed, making it worth serious consideration if your portfolio goals allow it.

Cash Reserves and Credit Score Standards

Cash reserves rank second in importance, and lenders won’t budge here: you need six months of mortgage payments sitting in the bank before closing, or twelve months if your loan exceeds conventional limits or your financial profile shows any weakness. This isn’t negotiable across most lenders, and it’s why many first-time investment property buyers face denial despite strong credit-they simply don’t have the reserves saved. Your credit score minimum hovers around 620-640 according to Fannie Mae and Freddie Mac guidelines, but that’s only the floor; scores below 680 typically force you into the 25% down category, while 680 and above unlock 15% down options. The difference between these tiers translates to tens of thousands of dollars over a 30-year loan, so strengthening your credit before application pays real dividends.

Debt-to-Income Ratio and DSCR Requirements

Debt-to-income ratio caps at 36-43% for investment properties, compared to 43-50% for primary residences, which means you have tighter constraints on other debts like car loans, student loans, and credit cards. Calculate your back-end DTI by adding all monthly debt payments (including the new mortgage) and dividing by gross monthly income; if you sit at 45% before the investment property loan, you won’t qualify because that new mortgage will push you over the limit. The Debt Service Coverage Ratio separates serious lenders from the rest, and this metric determines whether your property’s income actually covers its debt. Lenders require DSCR of at least 1.2, meaning net operating income must cover 120% of annual mortgage payments; if your property generates $5,000 per month in rent and your mortgage costs $4,000 monthly, your DSCR hits 1.25, which passes approval. This conservative approach protects both you and the lender, but it means your property must produce genuine cash flow above the mortgage payment to qualify.

Documentation, Timelines, and Income Calculation

Documentation requirements take 30-45 days because lenders demand two years of personal tax returns, two years of business tax returns if self-employed, current pay stubs, bank statements showing your reserves, a rent estimate or actual lease agreement, and proof of property management experience if you claim landlord income. Underwriting timelines stretch longer than primary mortgages precisely because of this documentation depth, so plan for 45 days minimum from application to closing rather than the typical 21 days. Most lenders count only 75% of projected rental income toward qualifying income according to Fannie Mae guidelines, accounting for vacancy risk and collection losses; if your lease shows $5,000 monthly rent, lenders count $3,750. Shopping five to seven lenders reveals rate differences of 0.5-1.0 percentage points, translating to tens of thousands over a 30-year loan; ask each lender about their investment property volume, turnaround time, and whether they service loans in-house or sell them to secondary markets.

Strengthening Your Application Before Submission

A mortgage professional who specializes in investment properties can help you strengthen your application before submission-whether that means timing your application after your business year closes to show stronger financials, paying down consumer debt to improve DTI, or saving additional reserves to exceed minimum requirements and secure better terms. These strategic moves often make the difference between approval and rejection, or between a competitive rate and one that eats into your returns. With your financial foundation solid, you’re ready to explore how to analyze the actual property’s performance and build a portfolio strategy that maximizes returns while managing risk.

How to Evaluate Property Performance and Build Your Investment Strategy

Calculate Cash Flow to Determine True Profitability

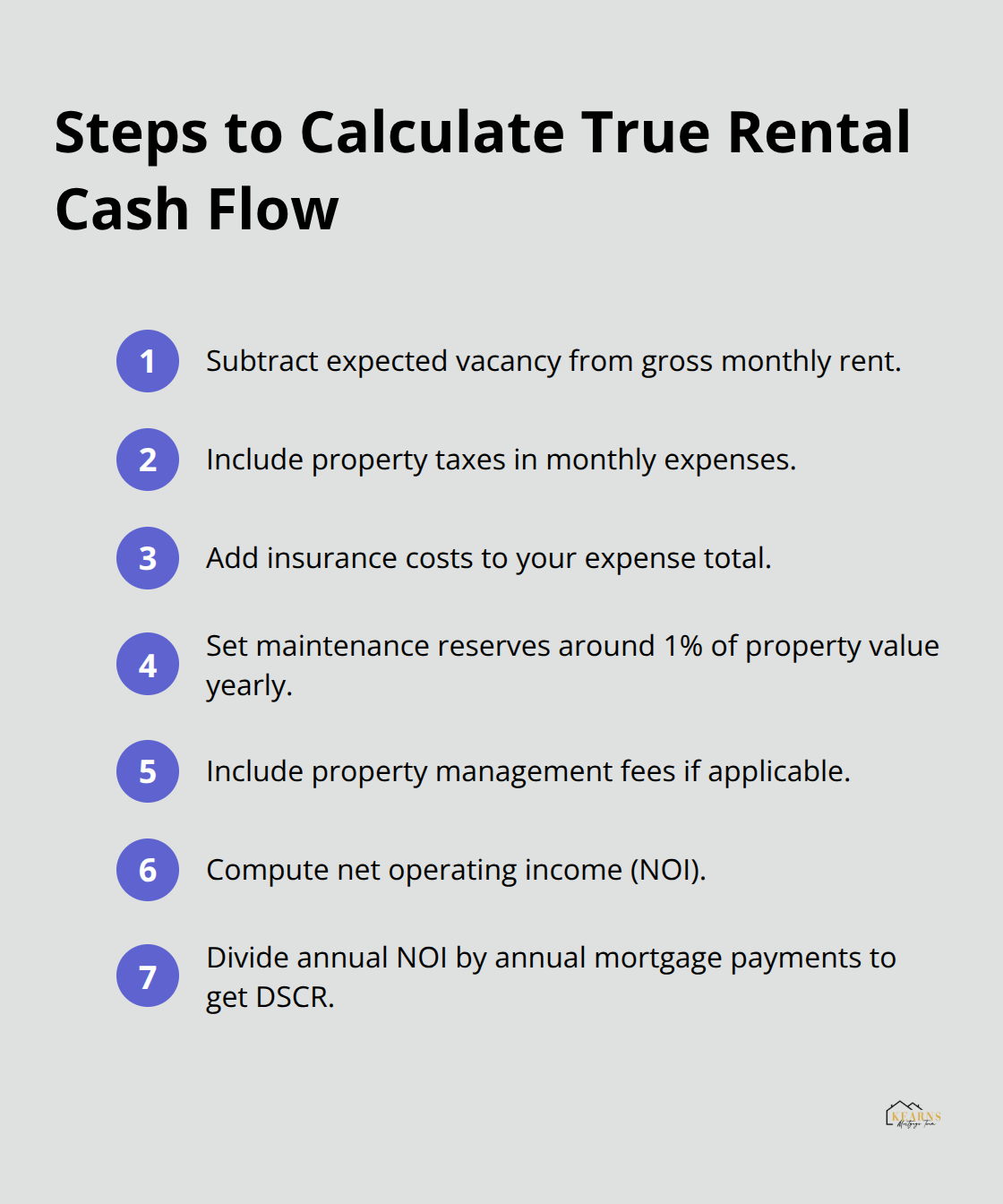

Property cash flow determines everything in real estate investing, and most beginners underestimate how much expenses eat into rental income. After you secure financing, calculate the actual numbers: take gross monthly rent, subtract vacancy loss (typically 5-10% annually), subtract property taxes, insurance, maintenance reserves (1% of property value yearly according to industry standards), and property management fees if you hire someone. What remains is net operating income, which you divide by your annual mortgage payment to calculate DSCR.

If a property generates $5,000 monthly rent but costs $1,200 in taxes, $400 in insurance, $300 in maintenance reserves, and $500 in management fees, your NOI sits at $2,600 monthly or $31,200 yearly. With a $48,000 annual mortgage payment, your DSCR lands at 0.65, which means the property loses money monthly and no lender will finance it. Flip this scenario: if the same property rents for $6,500, your NOI climbs to $3,100 monthly, producing a 1.29 DSCR that clears the 1.2 minimum and produces positive cash flow.

Use Cap Rate Analysis as Your Profitability Shorthand

Cap rate equals NOI divided by purchase price; a $300,000 property with $31,200 NOI has a 10.4% cap rate, while the same property with $37,200 NOI has a 12.4% cap rate. Markets vary wildly: high-cap-rate markets like Memphis or Louisville often yield 8-12%, while coastal markets like San Francisco typically produce 3-5%. Your job involves matching your risk tolerance to the market; higher cap rates mean stronger cash flow but often signal less price appreciation, while lower cap rates suggest appreciation potential but tighter margins today. A mortgage professional who specializes in investment properties helps you model these scenarios before you commit capital, showing how different down payments, interest rates, and holding periods affect your returns.

Build a Focused Portfolio Strategy

Building a diversified portfolio prevents the catastrophe of depending on a single property’s performance, but most beginner investors get this wrong by spreading too thin across too many markets instead of focusing strategically. Start with one to three properties in a single market where you understand local conditions, property management availability, and tenant demand, then expand once you’ve proven your operational skills and built cash reserves. The real estate community on r/realestateinvesting frequently discusses whether 20% down is always necessary, and experienced investors consistently agree it depends on your cash flow: if a property produces strong positive cash flow at 20% down, you build equity faster; if it barely cash flows at 20% down, putting 25-30% down destroys your returns by tying up capital that could finance a second property. This is counterintuitive but true: a second property producing 8% annual returns on your down payment beats paying extra principal on your first property earning you 3% through principal paydown. The math works because leverage amplifies returns when properties cash flow positively.

Monitor Portfolio Metrics Over Individual Property Performance

Track your portfolio’s combined DSCR, vacancy rates across all properties, and tenant quality metrics rather than obsessing over individual property performance; a portfolio with three properties averaging 1.35 DSCR can weather one property hitting 0.95 DSCR during a vacancy or major repair. A mortgage professional who specializes in investment properties helps you model portfolio growth across multiple acquisition timelines, showing how each property’s financing structure affects your overall returns and risk profile as your portfolio scales.

Final Thoughts

Financing an investment property demands discipline, clear financial metrics, and honest assessment of cash flow. Start by calculating your DSCR, verifying your DTI, confirming adequate reserves, and assessing whether a property produces positive cash flow after all expenses. Too many first-time investors chase appreciation while ignoring the monthly reality that their property loses money, which guarantees stress and eventual failure.

Your next step depends on your current financial position. If your credit score sits below 680, spend the next six months paying down consumer debt and building credit history before applying; if you have strong credit but limited reserves, start saving aggressively now rather than stretching yourself thin at closing. If you’re considering house-hacking by purchasing a duplex and living in one unit, that strategy works and deserves serious evaluation because it dramatically improves your financing terms.

We at Kearns Mortgage Team help you navigate how to finance an investment property with personalized guidance tailored to your portfolio goals, risk tolerance, and timeline. Contact Kearns Mortgage Team to discuss your investment property goals with someone who specializes in this space and can model different scenarios before you commit capital. What specific financial hurdle feels most challenging for your investment property goals right now?