A low credit score doesn’t have to stop you from buying a home. We at Kearns Mortgage Team know that many people assume bad credit makes homeownership impossible, but that’s simply not true.

Multiple loan programs exist specifically for borrowers in your situation. This guide walks you through real options, practical steps to strengthen your application, and how to get a mortgage with bad credit.

What Bad Credit Really Means to Lenders

Bad credit doesn’t have a single definition that all lenders agree on. The FICO score range of 300 to 579 is typically labeled subprime or poor credit, while scores between 580 and 669 fall into fair credit territory. However, this numerical categorization misses what actually matters to mortgage lenders. A score of 550 tells a different story than a score of 579, and lenders know it. What concerns them most is your payment history over the last two years. If you missed payments three years ago but paid everything on time since then, many lenders will view you as lower risk than someone with a recent missed payment, even if both have the same credit score. Fannie Mae and Freddie Mac removed their official minimum credit score requirement for conventional loans as of November 2025, meaning approval now depends on your overall credit risk profile rather than hitting a magic number. This shift reflects what smart lenders have always known: credit scores are a snapshot, not a destiny.

Payment Patterns Matter More Than You Think

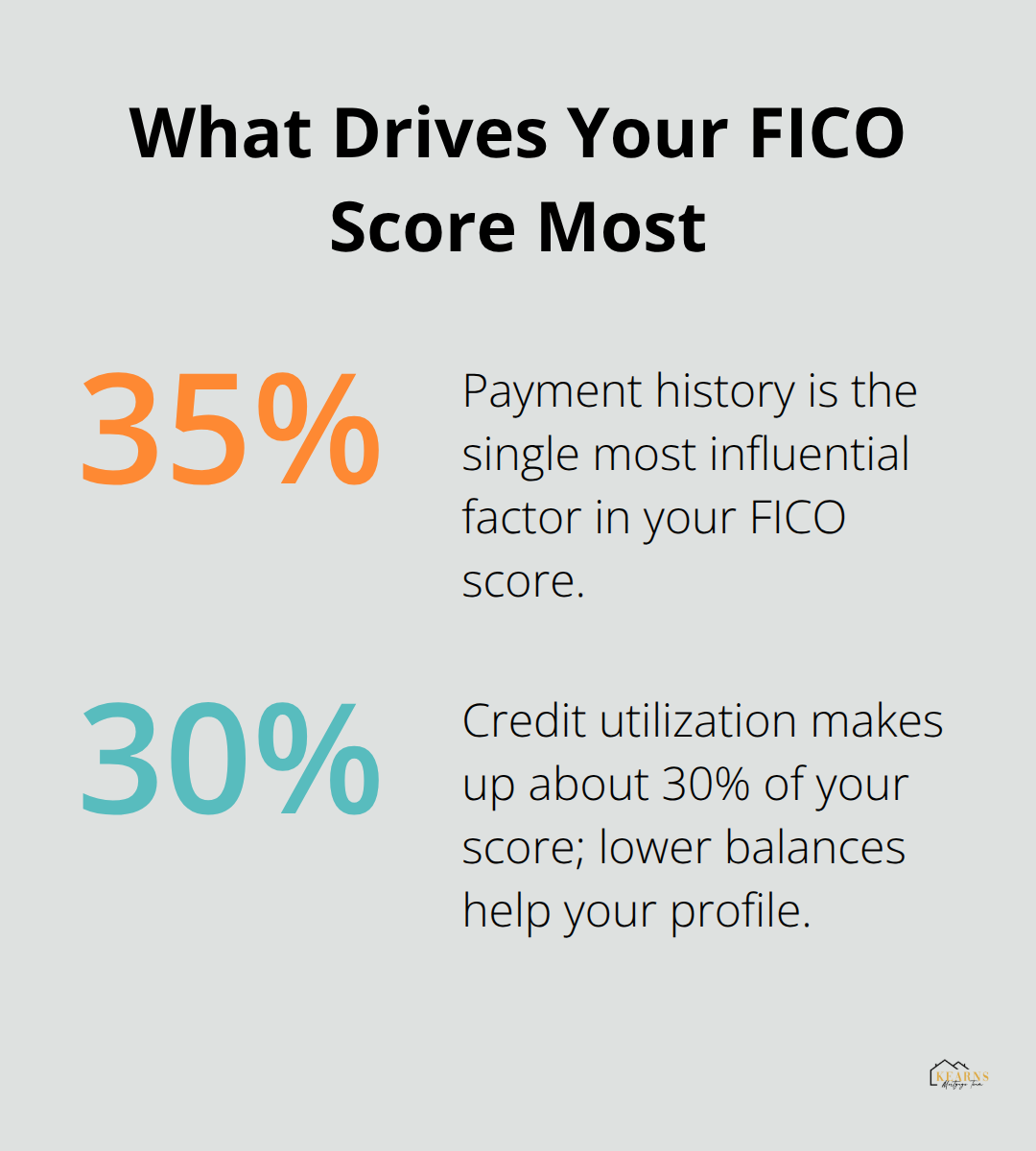

Lenders scrutinize what you’ve done recently far more than what happened years ago. According to FICO, payment history accounts for approximately 35 percent of your credit score, making it the single most influential factor. If you’ve made on-time payments for the past 12 months, you’re already demonstrating the behavior lenders care about most.

The second factor is credit utilization at about 30 percent of your score. If you’re carrying credit card balances above 30 percent of your available credit limits, paying those down before applying for a mortgage can noticeably improve your position.

Why Your Score Alone Doesn’t Determine Approval

Many borrowers with bad credit believe they need a perfect score to qualify, but that’s incorrect. Lenders regularly approve applicants whose scores sit in the 580 to 620 range through FHA, VA, or conventional programs. What separates approvals from denials is often a combination of factors: a reasonable down payment, manageable debt-to-income ratio, stable employment, and proof that recent financial behavior has improved.

Building Your Full Financial Picture

Lenders want evidence you can handle a mortgage payment, and they’ll look at rent payment history, utility payments, and other obligations to build that picture if your credit report alone doesn’t tell the full story. Your employment stability, savings reserves, and the size of your down payment all carry weight in the decision. These elements work together to show lenders that you pose an acceptable risk, regardless of past credit struggles. Understanding this reality opens doors that many borrowers assume are permanently closed.

Real Loan Programs That Work With Bad Credit

FHA Loans: The Most Accessible Path

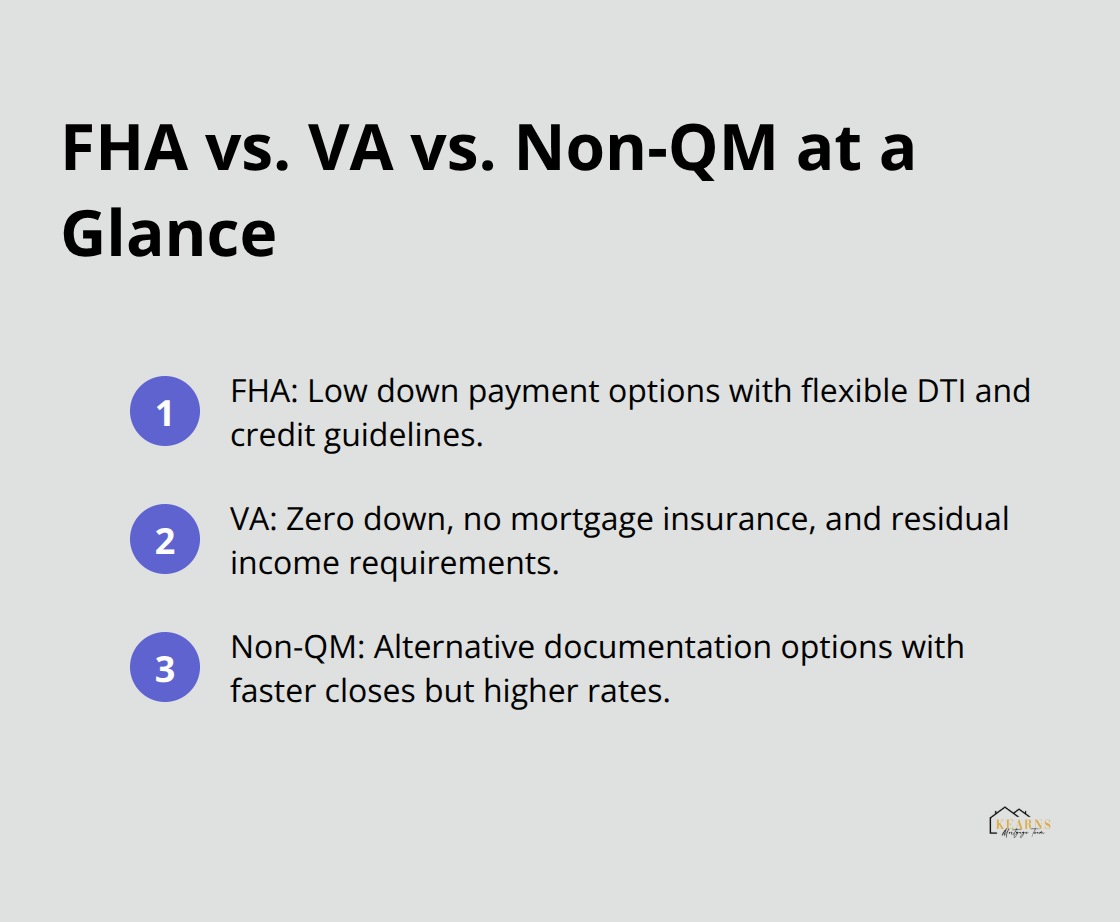

FHA loans stand out as the most practical choice for borrowers with credit scores between 500 and 619. The Federal Housing Administration insures these loans, which means lenders take on less risk and can approve applicants they’d otherwise reject. If your score sits at 580 or above, you can put down just 3.5 percent and qualify for a mortgage that conventional lenders would deny outright. Scores between 500 and 579 require a 10 percent down payment, but approval remains possible.

The trade-off is mortgage insurance, which stays on your loan for its entire life if your down payment falls below 10 percent. For someone with bad credit, this insurance cost is worth paying because it gets you into homeownership while you rebuild your financial profile. FHA loans also come with flexible debt-to-income requirements. Most lenders accept a housing expense ratio around 38 percent of your gross monthly income, with total debt-to-income around 45 percent. This flexibility matters enormously when you’re working with limited finances.

VA Loans: Zero Down Payment for Veterans

VA loans eliminate the down payment requirement entirely if you served in the military and received an honorable discharge. Unlike FHA loans, VA loans carry no mortgage insurance premium, which saves you thousands over the loan’s life. The VA doesn’t set an official minimum credit score, though most lenders expect around 620. However, veterans with scores as low as 580 have qualified by showing 12 months of on-time rent or mortgage payments and sufficient residual income to handle the payment.

VA loans also feature lower closing costs and allow seller contributions toward your expenses. The VA funding fee applies to most loans, but even with this fee, your total cost remains lower than an FHA loan with mortgage insurance.

Non-QM Loans: When Traditional Programs Don’t Fit

Non-QM loans represent a third path for borrowers whose income doesn’t fit traditional employment patterns or whose credit damage runs too deep for FHA approval. These loans accept bank statements, investment income, or rental history as proof of ability to pay. Interest rates run higher than conventional or FHA loans (sometimes 1 to 3 percentage points above standard rates), but they open doors for self-employed borrowers, freelancers, and those with recent delinquencies.

Comparing Your Options

The key difference between these programs is speed and cost. FHA loans process relatively quickly and come with moderate costs. VA loans cost less overall but require military service verification. Non-QM loans close faster than some alternatives but carry higher rates.

Your situation determines which program makes sense, and exploring which fits your financial circumstances helps you move forward with confidence.

Strengthen Your Application Before You Apply

Clean Up Your Credit Report First

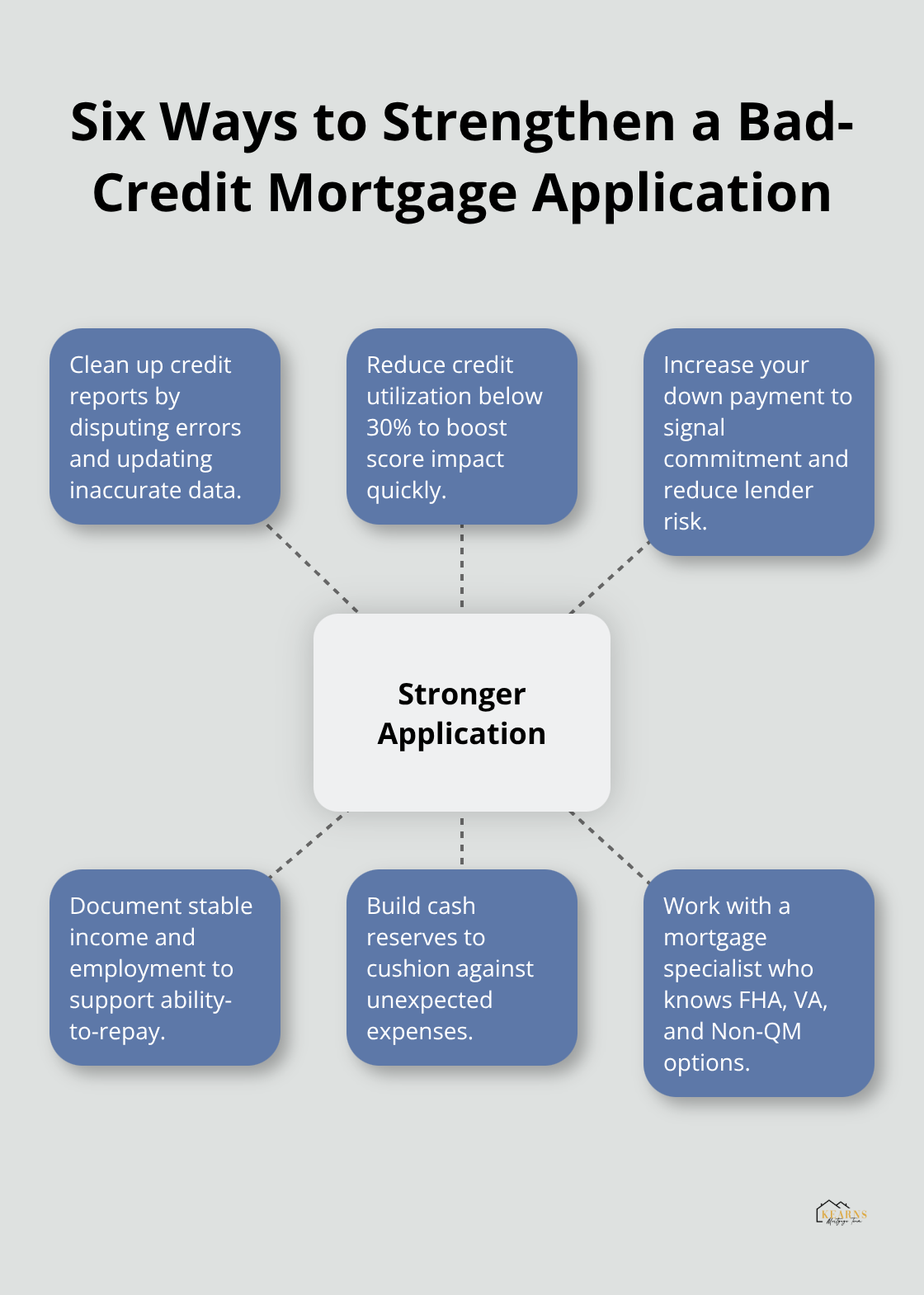

You have the legal right to access reports from all three bureaus through AnnualCreditReport.com, and roughly one in four Americans find errors on their reports according to the Federal Trade Commission. These errors cost you points you don’t deserve to lose. Look for accounts you don’t recognize, incorrect payment statuses, or duplicate entries. If you find mistakes, dispute them directly with the bureau. This takes 30 to 60 days but can raise your score meaningfully. Errors like a late payment marked as current or an account showing as open when you closed it are worth fighting.

Reduce Your Credit Utilization

Once you’ve cleaned your report, shift focus to your debt levels. Credit utilization-the percentage of available credit you’re actually using-accounts for 20 to 30 percent of your FICO score. If you’re carrying balances above 30 percent of your credit limits, paying those down before applying for a mortgage moves the needle faster than almost anything else. A person with a 650 score and 15 percent utilization looks substantially better to lenders than someone with a 650 score and 80 percent utilization. You don’t need to pay everything off, just get it below that 30 percent threshold. This single step often improves approval odds without requiring you to wait months for your score to naturally recover.

Increase Your Down Payment

Your down payment becomes your biggest negotiating tool when credit is weak. Lenders view a 10 percent down payment fundamentally differently than 3 percent, even on the same FHA loan. A larger down payment signals commitment, reduces the lender’s risk, and can qualify you for better terms despite your credit history.

If you can save an extra 5 to 10 percent beyond the minimum, do it before applying. The math works in your favor: spending three months saving an additional 5 percent down payment often results in lower interest rates and approval odds that exceed what you’d get from waiting six months for your credit score to improve naturally.

Work With a Mortgage Specialist

Once you’ve improved your report, reduced your debt, and saved aggressively, connect with a mortgage specialist who understands bad credit lending. Not all loan officers have equal experience with FHA, VA, or Non-QM programs. A specialist can assess your specific situation, identify which program fits your finances, and structure your application to emphasize your strengths rather than your weaknesses. The difference between working with a generalist and a specialist in bad credit mortgages often determines whether you get approved or denied. A specialist knows which lenders are actively approving applicants in your score range, which documentation helps your case, and whether your situation calls for FHA, VA, or a Non-QM approach.

Final Thoughts

Bad credit doesn’t lock you out of homeownership, and the programs we’ve covered-FHA loans, VA loans, and Non-QM mortgages-exist specifically because lenders understand that credit scores don’t tell the whole story about your ability to pay a mortgage. Start by pulling your credit reports from AnnualCreditReport.com and disputing any errors you find, then pay down your credit card balances to below 30 percent of your limits. These steps cost you nothing but time and discipline, yet they dramatically improve your approval odds when you apply for a mortgage with bad credit.

Your situation is unique, and how to get a mortgage with bad credit depends on your specific circumstances-someone with a 550 score and military service has different options than a self-employed borrower with a 600 score. A person who can save 15 percent down faces different approval timelines than someone putting down 3.5 percent. This is why working with a mortgage specialist matters, as they assess your full financial picture and match you with the right program rather than forcing you into a one-size-fits-all solution.

We at Kearns Mortgage Team understand bad credit lending because we work with borrowers in your exact situation every day. Connect with us for a free consultation to explore your options without pressure or obligation, and let our team review your credit report, calculate your debt-to-income ratio, and show you exactly which path makes sense for your goals. Homeownership is within reach-the question isn’t whether you can qualify, but whether you’re ready to take the steps that make it happen.