Multifamily real estate investments offer something most investors chase but rarely find: predictable income from day one. We at Kearns Mortgage Team have seen firsthand how apartment buildings and multi-unit properties generate wealth faster than single-family rentals.

The difference comes down to numbers. Multiple tenants mean multiple rent checks, lower costs per unit, and built-in protection against market swings. This guide walks you through the strategies that work and the mistakes that cost money.

Why Multifamily Properties Generate Superior Returns

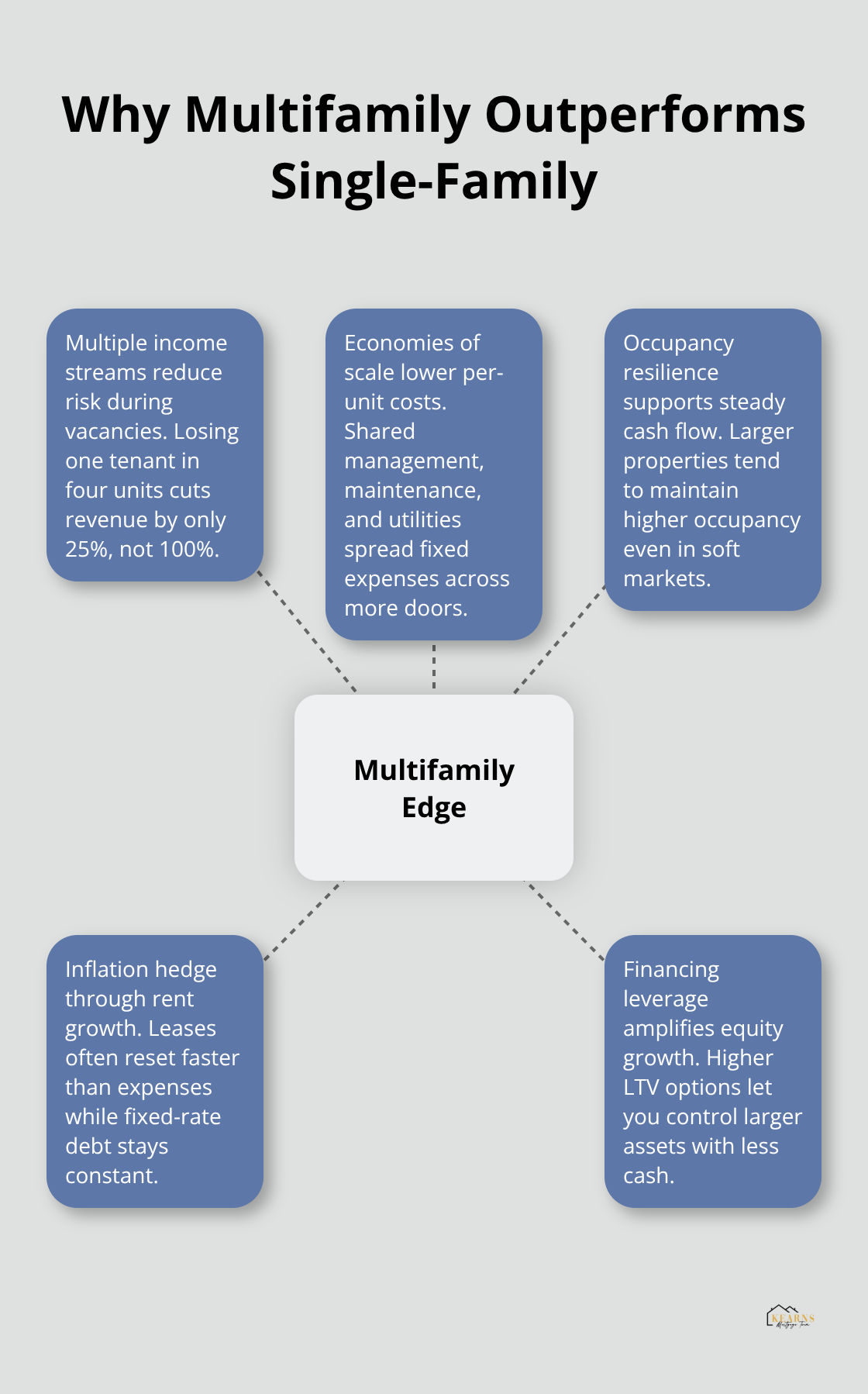

Multiple tenants paying rent simultaneously creates a financial advantage that single-family rentals simply cannot match. When one tenant in a four-unit property moves out, three others continue paying rent and covering your expenses. A single-family landlord loses 100% of income the moment a tenant leaves. This resilience matters during tenant transitions, which typically last 30 to 60 days. According to industry data, multifamily properties maintain occupancy rates around 94.6% even during soft markets, while single-family rentals experience higher vacancy swings.

The math is straightforward: four rent checks provide four income streams instead of one, and losing one tenant represents only a 25% revenue hit rather than total loss.

The Real Cost Advantage of Scale

Expenses per unit drop dramatically as your property grows. A property manager handling a single-family home costs roughly the same as one managing a 12-unit building, yet that cost spreads across 12 units instead of one. Insurance, property taxes, and maintenance contracts all benefit from this same principle. A typical property management fee runs 8-12% of collected rent for single-family homes but only 4-6% for multifamily buildings. Utilities, if owner-paid, cost less per unit when negotiated for multiple meters. Vendors quote lower rates for bulk services like landscaping, pest control, and repairs. Once you reach approximately 70 to 80 units, you can justify on-site property management and maintenance staff, creating a self-contained operation that handles everything in-house. This threshold represents the point where multifamily investing shifts from passive income to a genuine business with predictable overhead.

Inflation as Your Secret Advantage

Rent growth outpaces inflation in most markets, which means your cash flow increases faster than your expenses rise. Between 2020 and 2024, median rent increased approximately 25-30% nationwide while overall inflation ran around 20%. This spread compounds over time. A property that generates $50,000 in annual net operating income today could generate $75,000 within five years if rents climb while expenses remain relatively stable. Unlike bonds or savings accounts, multifamily properties naturally hedge against inflation through rent escalation. Your fixed-rate mortgage payment stays the same while rents climb, widening your margin. Single-family rentals enjoy this same benefit but lack the income stability that multiple units provide.

How Financing Amplifies Your Returns

Strategic leverage transforms multifamily investing into a wealth accelerator. Most multifamily lenders offer loan-to-value ratios between 70-87%, meaning you control a property worth $1 million with only $130,000-$300,000 down (depending on the program). Your tenants’ rent payments service the debt while the property appreciates. If property values rise 3-4% annually-a conservative estimate for stabilized multifamily assets-your equity grows substantially faster than your cash investment. This leverage works in your favor during rising markets and requires careful underwriting during uncertain periods. The combination of multiple income streams plus rent growth creates a wealth-building machine that accelerates as decades pass, positioning you to move toward larger acquisitions and portfolio expansion.

Building Your Path to Scale

Location Strategy: Where Markets Matter Most

Location determines multifamily success more than any other factor, and the data proves it. Properties in high-demand markets with strong job growth, population influx, and limited new construction command higher rents and attract quality tenants. You should analyze employment trends in your target market-look for diversified job sectors rather than single-industry towns, which collapse when that industry falters. Check local vacancy rates through CoStar or similar commercial real estate databases; markets with vacancy rates below 5% typically support rent growth.

School district ratings matter for family housing, while proximity to universities matters for student housing. You want to avoid markets where rent growth has already peaked; enter before the run-up, not after. The most successful investors focus on secondary and tertiary markets where acquisition costs remain reasonable but job growth justifies higher rents-these markets offer better risk-adjusted returns than saturated coastal cities where down payments exceed 25% and cap rates compress below 4%.

Financing Strategy: Structuring Leverage for Maximum Returns

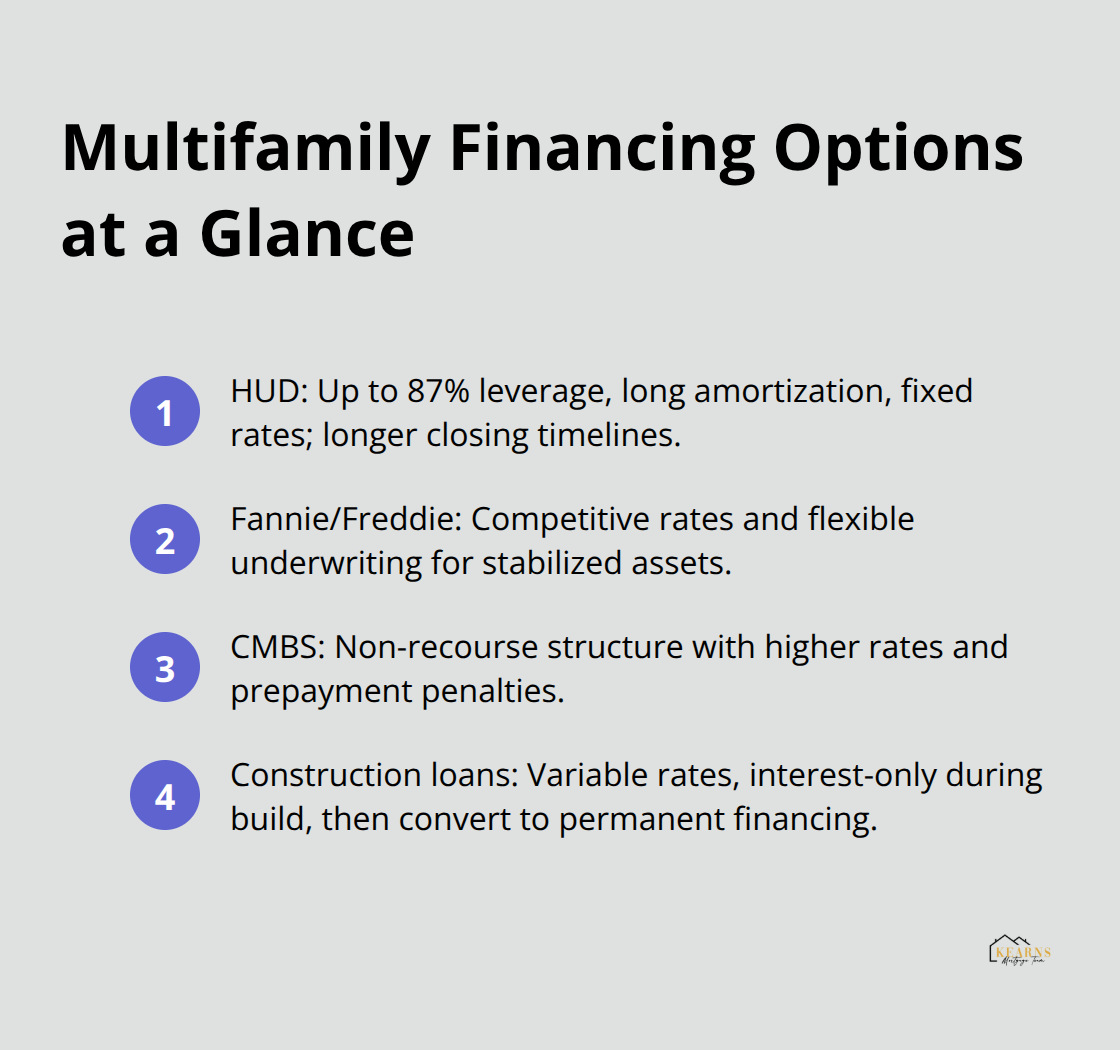

Financing strategy directly controls your return on equity, which means the right loan structure matters more than the perfect property. HUD loans through the Federal Housing Administration offer leverage up to 87% with fixed rates and 35- to 40-year amortization, though expect six-month closings. Fannie Mae and Freddie Mac multifamily loans typically deliver lower rates than conventional financing for stabilized assets, with more flexible underwriting than traditional banks. CMBS loans provide non-recourse financing, meaning lenders cannot pursue your personal assets if the deal underperforms, but rates run 0.75-1.5% higher and prepayment penalties restrict refinancing flexibility.

Construction loans carry variable rates and interest-only payments during the build phase, usually lasting 12 to 36 months before conversion to permanent financing. The Debt Service Coverage Ratio must exceed 1.25 for most lenders, so model your cash flow conservatively and plan for 5-7% vacancy even in strong markets.

Operations and Management: Building the Business

Property managers operating at scale handle daily operations and tenant relations, which frees you to focus on acquisition and capital formation. Once you manage 70 to 80 units across multiple properties, hire on-site staff for maintenance and leasing rather than relying entirely on third-party management. This threshold is where multifamily investing transforms from a passive income play into an active business that generates substantial cash flow while building long-term wealth. Your operational decisions at this stage directly impact whether you can scale further or plateau at your current size.

Where Underwriting Fails and How to Protect Yourself

Validate Rental Income with Real Market Data

The gap between projected cash flow and actual cash flow destroys multifamily deals more than any other factor. Most investors overestimate rental income by 10-15% and underestimate expenses by 20-30%, creating a false picture of profitability. Start with a rental market analysis that compares similar properties in your exact location, not neighboring markets or different building types. A four-unit property in one neighborhood may rent for $1,400 per unit while identical units two miles away command only $1,200 because of school districts, highway proximity, or crime rates. Use CoStar, Zillow rental data, or local property management companies to validate rents before you make an offer. Conservative projections assume 5-7% vacancy even in strong markets because tenant turnover happens regardless of economic conditions. If you project 100% occupancy with $100,000 annual rent, your actual operating income likely runs closer to $93,000 to $95,000.

Account for True Operating Expenses

Expenses require the same ruthless accuracy as income projections. Property taxes vary dramatically by location, and recent reassessments often spike your costs. Insurance costs approximately $0.50 to $1.50 per square foot annually depending on location and building age. Maintenance and repairs consume 2-5% of annual rents, but aging buildings or those in harsh climates run higher. A roof replacement costs $15,000 to $30,000 for a typical multifamily property, and this expense arrives unpredictably. Set aside capital reserves equal to 5-10% of monthly rent specifically for major replacements rather than discovering mid-year that your cash flow evaporated. Property management fees range from 8-10% of monthly rent, and if you self-manage, factor in your time at an hourly rate because self-management is not free labor.

Navigate Market Cycles and Timing

Economic cycles separate successful investors from those who get trapped in underwater deals. Markets that supported 6% cap rates in 2022 now require 7-8% cap rates as interest rates climbed and property values adjusted. A property that seemed profitable at $2 million purchase price becomes a burden if comparable properties now sell for $1.6 million. Avoid chasing markets at peak pricing; instead, analyze whether rents have already appreciated faster than typical historical growth rates. If rents jumped 20% in the past two years, expect slower growth ahead and model conservatively. Interest rate sensitivity matters intensely because multifamily properties depend on refinancing or sale to realize gains. Rising rates compress property values immediately because buyers demand higher cap rates to compensate for higher borrowing costs.

Inspect Properties and Assess Deferred Maintenance

Property vetting requires walking the neighborhood at different times and speaking with current tenants about management responsiveness. Review maintenance records for the past three years to identify patterns. A property with deferred maintenance looks cheap until you calculate the actual cost of catching up. Roof condition, HVAC systems, plumbing, and foundation issues determine whether you inherit a cash-flowing asset or an ongoing expense nightmare. These structural and mechanical components represent your largest capital expenditure risks, so hire a qualified inspector to assess their remaining useful life before you commit capital.

Screen Tenants to Protect Cash Flow

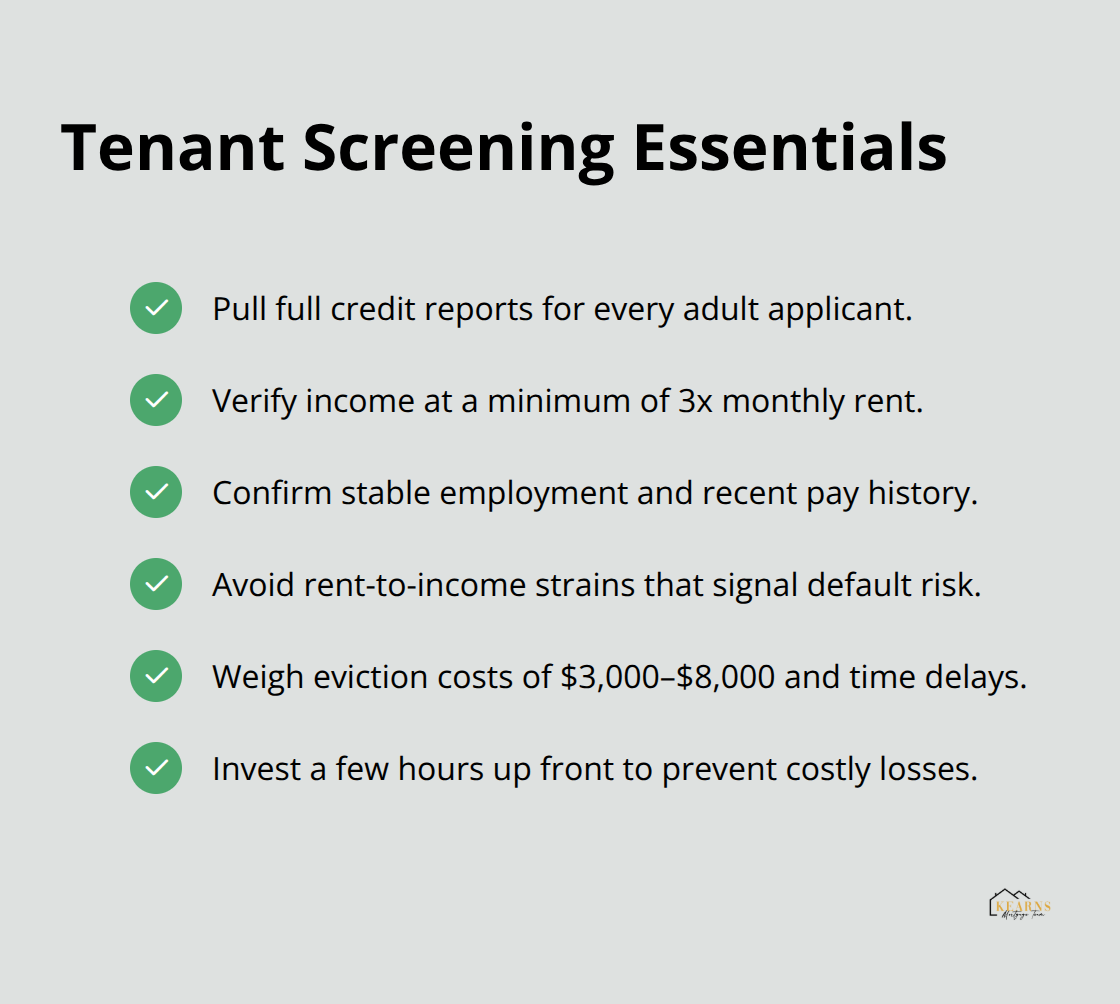

Tenant quality directly impacts your income stability and operational stress. Screen tenants using credit reports, income verification requiring minimum 3x rent monthly income, and employment history checks. A tenant earning $2,400 monthly should not rent a $1,200 unit because they lack financial cushion for emergencies and default risk spikes. Evictions cost $3,000 to $8,000 in legal fees and lost rent, plus months of court delays in many states. Spending three hours on tenant screening saves you tens of thousands in losses later.

Final Thoughts

Multifamily real estate investments succeed when you combine disciplined underwriting with realistic market expectations. The properties that generate wealth share three characteristics: multiple income streams that cushion vacancy losses, operating expenses that decline per unit as scale increases, and rent growth that outpaces inflation over time. You now understand why a four-unit property outperforms a single-family rental and why reaching 70 to 80 units transforms your operation from passive income into a genuine business.

Your next move depends on where you stand today. If you own single-family rentals, analyze whether converting that capital into a small multifamily property makes sense for your market and timeline. If you start fresh, begin with 10 to 20 unit properties to learn operations before scaling toward larger complexes. Either path requires honest cash flow modeling, conservative rent projections validated against actual market data, and capital reserves for the maintenance surprises that always arrive.

The financing decision shapes your entire return profile. Government-backed programs like HUD loans offer leverage up to 87% with fixed rates, while Fannie Mae and Freddie Mac deliver competitive rates for stabilized assets. We at Kearns Mortgage Team help investors navigate these financing options and structure loans that align with your cash flow projections and long-term portfolio goals. What market or property type aligns with your current financial position and investment timeline?