Florida’s real estate market is booming, and rental property investing in Florida offers serious wealth-building potential. Whether you’re new to real estate or expanding an existing portfolio, we at Kearns Mortgage Team know the opportunities here are substantial.

This guide walks you through everything you need to know-from market conditions and neighborhood selection to financing strategies and maximizing returns. Let’s build your path to long-term financial success.

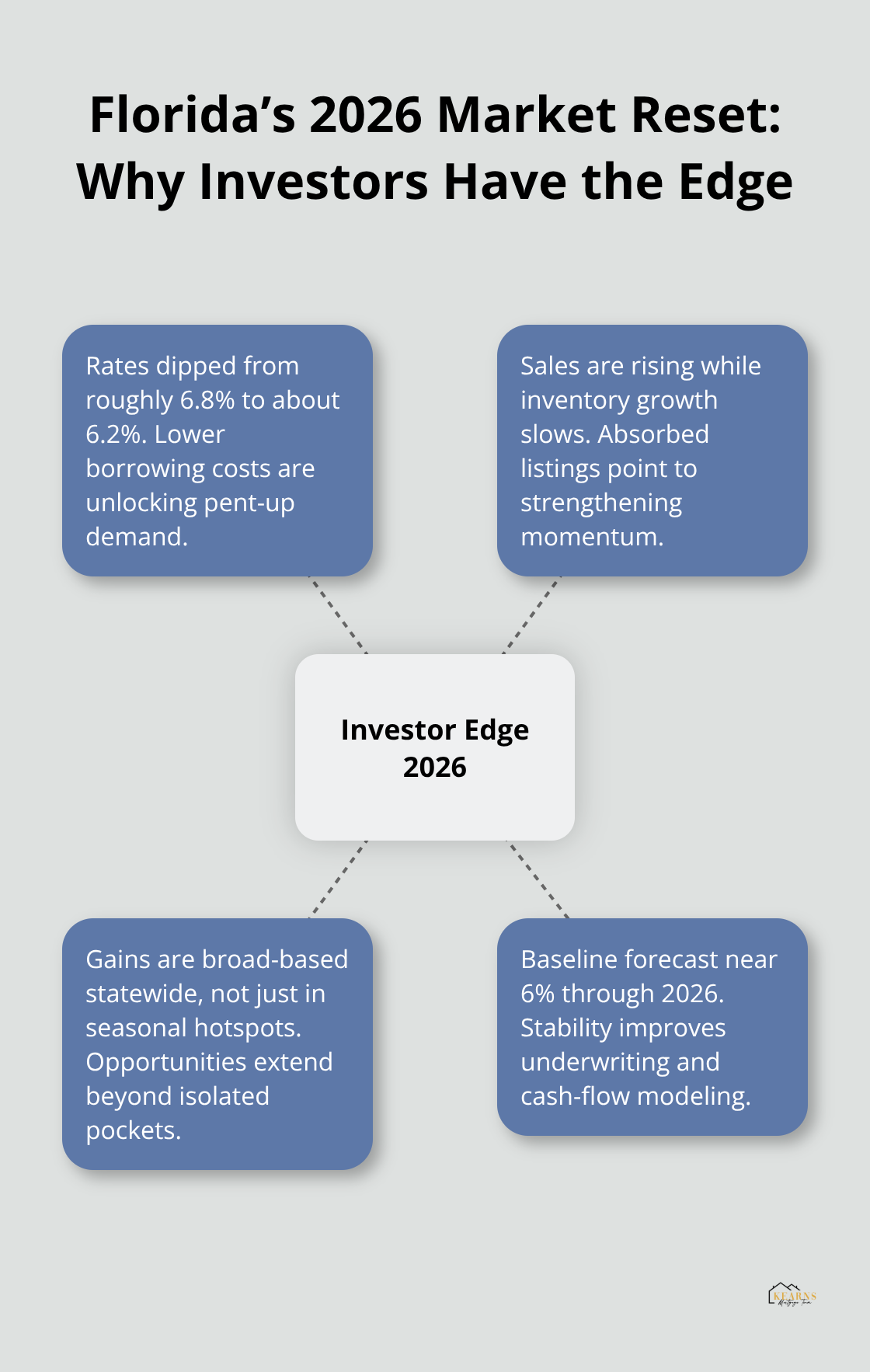

Why Florida’s Market Shifted in 2026

Rate Declines Unlock Investor Opportunity

Florida’s rental market is experiencing a fundamental reset that favors investors willing to act now. Mortgage rates declined from around 6.8% in 2025 to approximately 6.2% recently, according to Florida Realtors Chief Economist Dr. Brad O’Connor. This drop has unleashed pent-up demand across the state. Monthly sales are rising for the first time since 2022, and inventory growth has slowed as listings get absorbed. The improvement isn’t concentrated in a few seasonal hotspots-it’s broad-based across Florida, which means opportunities exist statewide rather than in isolated pockets. Dr. O’Connor’s baseline forecast suggests 30-year fixed rates could hover around 6% for much of 2026, potentially strengthening activity if rates stabilize. This stability lets you model cash flow with confidence instead of guessing about future rate environments.

Population Growth and Job Creation Drive Rental Demand

Population growth and job creation remain the real drivers here. Florida continues attracting remote workers and people relocating from higher-cost states, which sustains rental demand year-round. Tourism adds another layer-Pensacola alone saw 651,800 visitors and 905,362 airline passengers in January 2025, with vacation rental room rates up 8.7% to $164.84 per night. That’s not theoretical demand; that’s actual money flowing into short-term rental pockets.

The Two-Tier Buyer Dynamic Strengthens Rental Markets

Affordability constraints are pushing equity-rich homeowners into rental markets while first-time buyers account for only about 21% of purchases nationally. This two-tier dynamic means strong rental tenant demand. The spring buying season typically brings heightened activity, so timing your acquisitions and lease-up strategies around this cycle gives you better occupancy rates and pricing power. Migration and job growth will continue shaping which markets perform best, but the overall momentum is unquestionably upward heading into the second half of 2026. With this tailwind at your back, the next step is identifying which specific Florida neighborhoods and cities will deliver the strongest returns for your portfolio.

Where to Invest and How to Finance Your Florida Rental Portfolio

Miami, Orlando, Tampa, and Jacksonville Lead the Market

Florida’s strongest rental markets reward investors who match property selection to financing strategy. Miami leads in liquidity and pricing power, with condo transaction volume reflecting a 2.3% drop month-over-month in recent months and median condo prices around $620,000. RentCafe ranked Miami as the most competitive rental market in early 2025, meaning rents rise faster when supply tightens. Orlando attracts relocations aggressively-Redfin named it among the top moving-to metros in late 2024 and early 2025, with February 2025 median home prices around $415,000, making entry affordable while demand stays strong. Tampa offers solid cash-flow mechanics: March 2025 median rent was $2,145 monthly on typical single-family homes priced near $450,000.

Jacksonville delivers the best entry-level returns-February 2025 median sale prices hovered around $300,000 while rents averaged $1,641 monthly, creating favorable cash-flow dynamics for conservative investors.

Secondary Markets: Pensacola, Fort Lauderdale, and Gainesville

Pensacola benefits from tourism intensity; January 2025 brought 651,800 visitors and vacation rental room rates up 8.7% to $164.84 nightly, signaling short-term rental upside. Fort Lauderdale combines Miami proximity with strong rental interest at March 2025 average rents near $2,700 on median home values around $513,000. Gainesville’s student-housing engine-fueled by the University of Florida-creates stable rental income; Redfin data shows median home prices jumped from about $227,000 in February 2023 to $275,500 in February 2024, a 21.3% surge reflecting steady tenant demand. The practical move: pair high-demand short-term rental markets like Miami and Orlando with affordable steady-cash-flow markets like Jacksonville and Pensacola to balance risk across your portfolio.

DSCR Loans vs. Conventional Investment Financing

Financing structures determine whether your rental investment produces cash flow or depletes reserves monthly. DSCR loans (debt service coverage ratio) qualify based on property income rather than personal income, making them ideal for building multi-property portfolios without hitting personal debt-to-income limits. These loans typically require 20-25% down, accept credit scores as low as 660-680 (though 780+ secures better rates), and work on properties with 1-9 units. Rates currently range around 7-8.5% depending on credit and down payment size. Conventional investment property loans demand 15% down for single-family rentals and 25% for 2-4 unit properties, with stricter debt-to-income calculations-typically capped at 45-50% after lenders use 75% of the property’s market rent to offset mortgage payments. As of late 2025, conventional investment rates sit about 0.5-0.875% higher than primary residence rates.

Cash Flow Math and Real-World Numbers

A $300,000 Jacksonville rental with 25% down ($75,000) and DSCR financing at 7.8% on $1,641 monthly rent produces approximately $350 monthly cash flow before reserves-enough to cover maintenance and vacancy without tapping personal income. Property management and tenant screening directly impact that cash flow. Screen tenants aggressively by verifying employment, pulling credit reports, and checking rental history; bad tenants destroy returns faster than any market downturn. Management fees typically run 8-12% of collected rent, but quality managers identify lease violations early, coordinate maintenance efficiently, and maintain occupancy rates that keep vacancy below 6%.

Florida’s Landlord-Friendly Lease Environment

Florida’s landlord-friendly environment-no statewide rent control and relatively flexible lease termination-lets you adjust rents annually as market conditions shift, which matters enormously when inflation or local job growth pushes comparable rents upward. This flexibility transforms your portfolio from a static income stream into a dynamic asset that captures market appreciation. With the right property in the right market and the right financing structure locked in, your next challenge involves protecting that investment through smart maintenance and strategic tax planning.

How to Lock in Profits While Protecting Your Investment

Set Rental Rates That Attract Quality Tenants

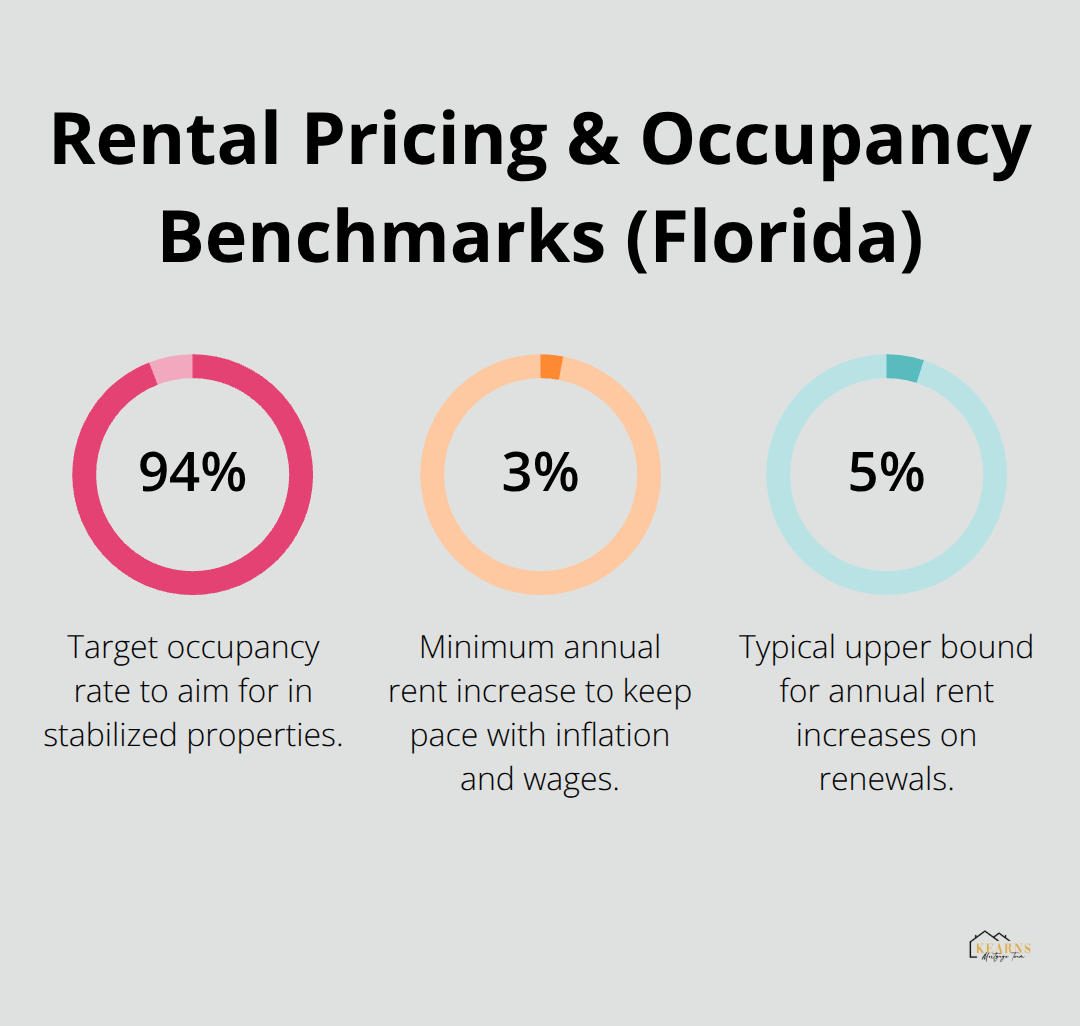

Rental rates in Florida move with local market conditions, and setting them too low costs you thousands annually while setting them too high invites vacancy that costs even more. Research comparable rental rates in your specific neighborhood on platforms like Zillow and Apartments.com, then price within the 75th percentile rather than at the absolute market peak. This approach attracts quality tenants faster while maintaining occupancy rates above 94 percent. Tampa’s March 2025 median rent of $2,145 monthly on single-family homes reflects what the market will bear there, but a property one mile away might command $1,895 depending on walkability, schools, and proximity to job centers.

Raise rents annually by 3-5 percent as leases renew; Florida’s landlord-friendly environment with no statewide rent control allows you to capture inflation and local wage growth without legal friction. This discipline compounds dramatically over a decade-a $2,000 monthly rent that grows 4 percent annually reaches $2,960 by year ten, creating an extra $11,520 in cumulative revenue compared to holding rates flat.

Leverage Tax Deductions to Improve After-Tax Returns

Tax deductions directly reduce your taxable income and dramatically improve after-tax returns that most investors ignore when calculating true profitability. Depreciation deductions on residential rental property span 27.5 years, meaning you write off roughly 3.6 percent of the property’s structure value annually without spending cash. A $300,000 rental with $240,000 in depreciable structure value generates $8,727 in annual depreciation deductions that shelter rental income from taxation. Mortgage interest, property taxes (typically 1.8 percent of value or higher in Florida), insurance premiums, management fees, maintenance repairs, and vacancy losses all qualify as deductible operating expenses. A $375,000 Tampa-area rental with 20 percent down at 7.5 percent financing produces roughly $2,098 in monthly principal and interest payments, where the interest portion-approximately $1,875 in year one-becomes a direct tax deduction. Partner with a CPA who specializes in real estate investment rather than a general tax preparer; cost segregation studies accelerate depreciation timing and boost early cash flow, though the analysis costs $3,000–$8,000 upfront.

Build Maintenance Reserves and Protect Long-Term Value

Maintenance reserves demand discipline that separates successful landlords from those eroding equity. Budget 5–10 percent of annual rental revenue for maintenance and repairs. A $2,145 monthly rent generates roughly $12,870 annually, meaning you should reserve $1,287–$1,435 monthly for eventual roof repairs, HVAC replacements, and appliance failures that inevitably arrive. Maintain at least two months of total expenses in a dedicated savings account as a financial cushion against unexpected vacancy or major repairs; this prevents forced sales or personal debt when market conditions shift temporarily. Upgrade kitchens, bathrooms, and curb appeal systematically rather than reactively-these improvements command 5–10 percent rent premiums and reduce tenant turnover, which costs $2,000–$4,000 per vacancy cycle in lost rent and marketing expenses.

Screen Tenants Aggressively to Protect Cash Flow

Property management and tenant screening directly impact your cash flow and long-term returns. Screen tenants aggressively by verifying employment, pulling credit reports, and checking rental history; bad tenants destroy returns faster than any market downturn. Management fees typically run 8–12 percent of collected rent, but quality managers identify lease violations early, coordinate maintenance efficiently, and maintain occupancy rates that keep vacancy below 6 percent. This investment in professional management protects the cash flow you worked to establish through smart pricing and tax planning.

Final Thoughts

Building a rental property portfolio in Florida requires three core commitments: selecting markets with genuine economic momentum, financing strategically to preserve cash flow, and protecting your investment through disciplined management and tax planning. Rate stability around 6% through 2026, broad-based market improvement across the state, and strong population growth create a window for investors willing to act with clarity rather than emotion. Your success in rental property investing Florida hinges on matching property selection to financing structure.

DSCR loans eliminate personal income verification and let you scale beyond the conventional four-property threshold, while competitive rates and flexible terms reward investors building multi-unit portfolios. Jacksonville’s $300,000 entry prices paired with $1,641 monthly rents deliver immediate cash flow, Miami’s liquidity attracts investors seeking appreciation, and Tampa’s job market sustains rent growth. The strategy isn’t picking one market-it’s building across complementary markets that balance risk and returns.

Rental property investing also demands attention to the mechanics that separate profitable landlords from those bleeding cash monthly. Screen tenants rigorously, maintain 5-10% maintenance reserves, and raise rents annually by 3-5% as leases renew. We at Kearns Mortgage Team offer personalized guidance on loan options including Non-QM and conventional structures designed specifically for investment property investors, and a free consultation lets you explore which financing path aligns with your portfolio vision without obligation.