Buying your first home in Tampa is within reach, even if you think you can’t afford the down payment. We at Kearns Mortgage Team know that Tampa first-time homebuyer programs can eliminate this barrier entirely.

Federal, state, and local assistance options exist right now. This guide shows you exactly which programs you qualify for and how to apply.

Federal and State Programs That Lower Your Down Payment

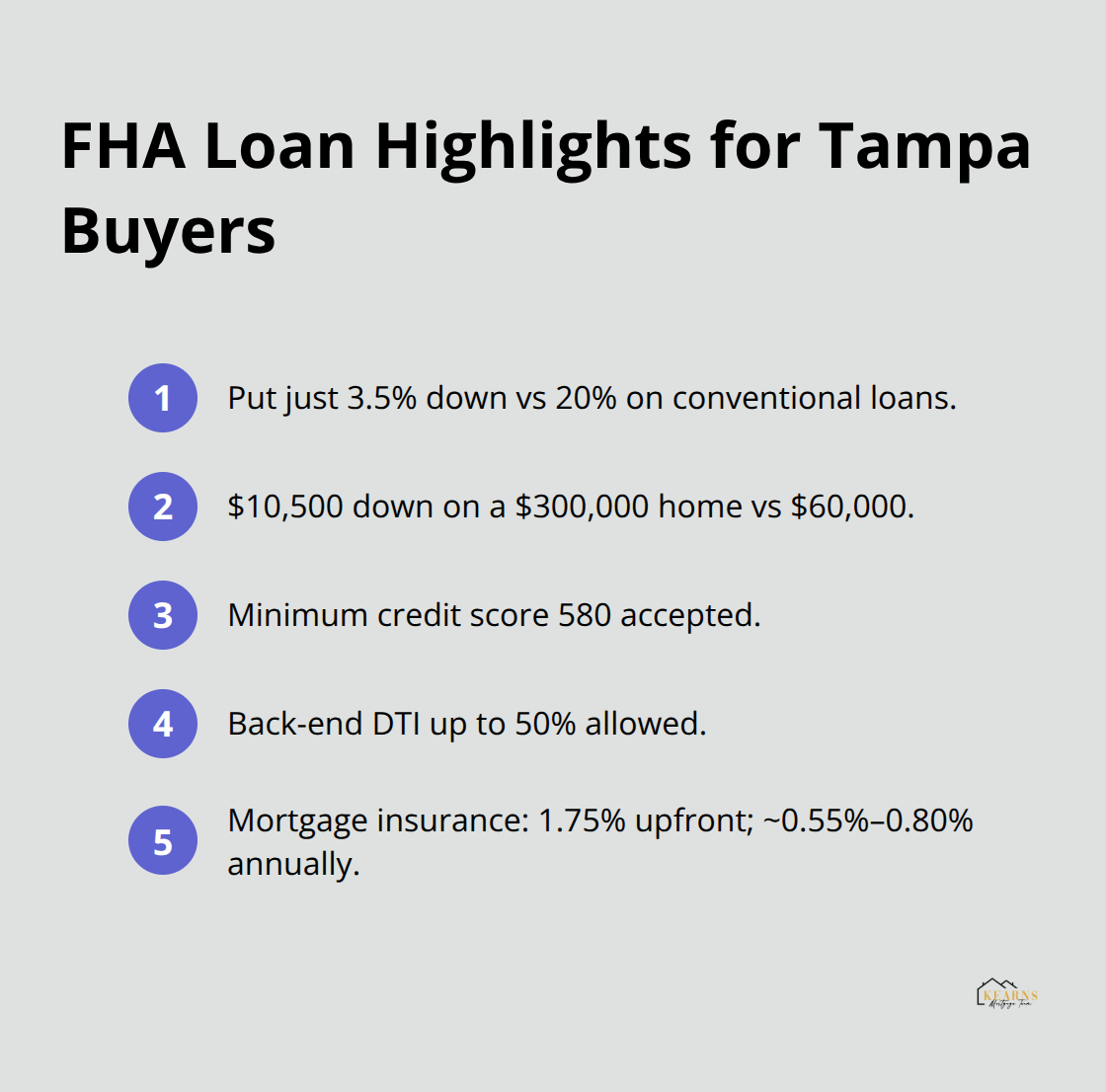

FHA Loans: 3.5% Down Instead of 20%

FHA loans require far less upfront money than conventional mortgages. Most FHA borrowers put down just 3.5 percent of the purchase price, compared to the 20 percent standard for conventional loans. On a $300,000 home in Tampa, that difference means you need $10,500 instead of $60,000. FHA loans accept credit scores as low as 580, making them accessible even if your credit history isn’t perfect.

The Federal Housing Administration insures these loans, which means lenders approve borrowers they’d otherwise reject.

Your debt-to-income ratio can stretch to 50 percent on the back end, giving you more borrowing power. One catch: FHA loans require mortgage insurance premiums, both upfront and annually. The upfront premium runs 1.75 percent of the loan amount, and annual premiums typically range from 0.55 to 0.80 percent depending on your loan-to-value ratio and loan term. Despite this added cost, the lower down payment requirement makes homeownership achievable for Tampa buyers who’d otherwise wait years to save.

VA Loans: Zero Down for Veterans

VA loans eliminate the down payment requirement entirely for eligible military service members and veterans. If you served in the U.S. Armed Forces, you qualify for zero-down financing through the Department of Veterans Affairs, assuming you obtain a Certificate of Eligibility. VA loans also skip the mortgage insurance requirement that plagues FHA borrowers, saving thousands over the loan’s life.

Your VA loan benefit can be used multiple times, and some veterans with full entitlement can use it again after paying off a previous VA loan. Interest rates on VA loans typically run lower than conventional or FHA options because the VA guarantees a portion of the loan to the lender.

USDA Loans: 100% Financing for Rural and Suburban Areas

USDA loans serve rural and suburban areas outside major metropolitan zones, offering 100 percent financing with no down payment required. USDA borrowers must meet income limits for Hillsborough County set by the Rural Development program. USDA loans charge a guarantee fee upfront and an annual fee, but the zero-down structure makes them powerful for qualifying buyers in eligible areas.

Layering Federal Benefits with Local Assistance

All three programs pair with down payment assistance from state and local sources, meaning you can combine federal benefits with additional local grants to cover closing costs or boost your equity position from day one. Tampa and Hillsborough County offer their own programs specifically designed to work alongside these federal options, which we’ll explore next.

Local Tampa and Hillsborough County Programs

City of Tampa’s Dare to Own the Dream Program

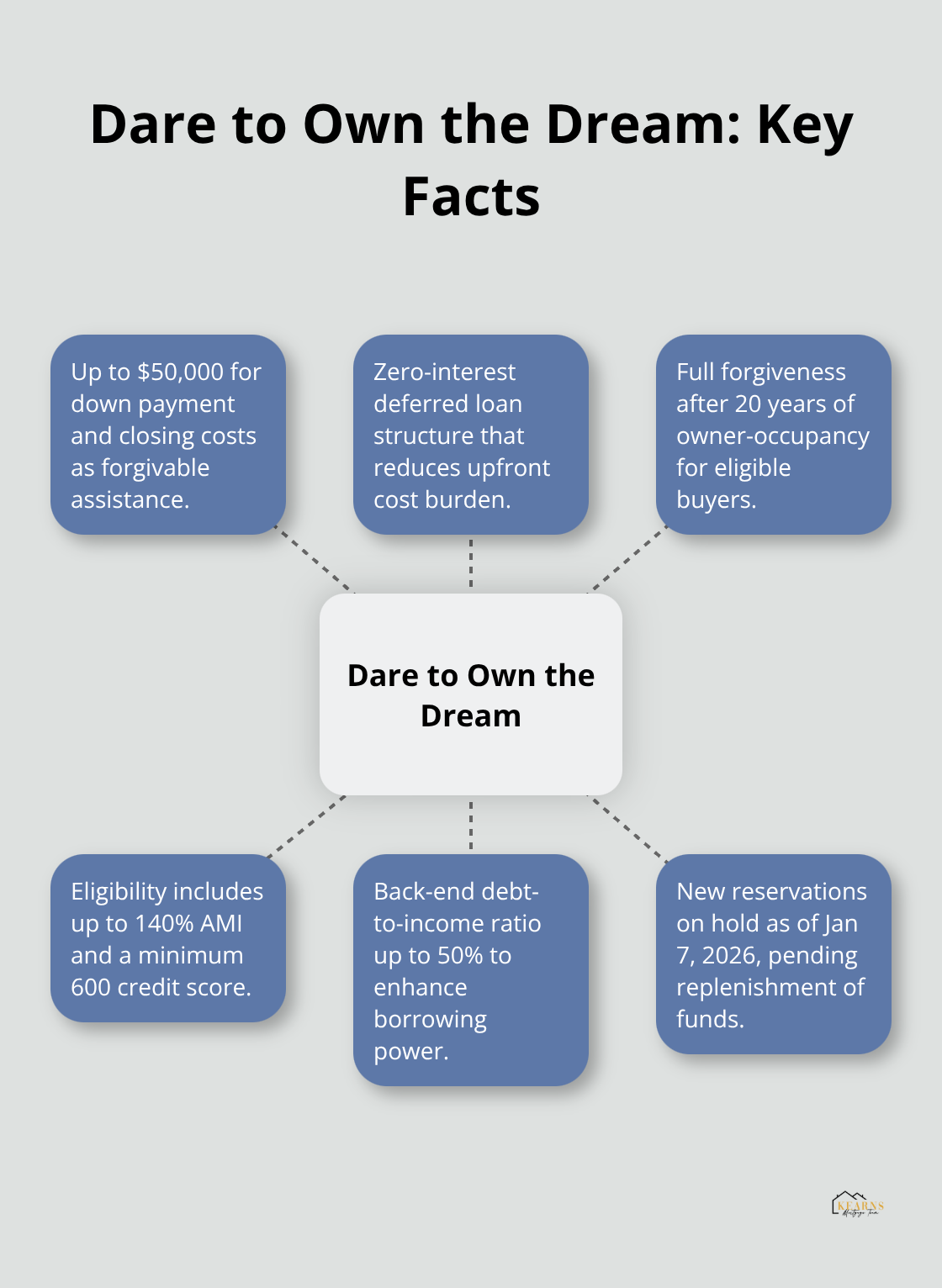

The City of Tampa’s Dare to Own the Dream program provides up to $50,000 in forgivable down payment and closing cost assistance for eligible buyers. This zero-interest deferred loan forgives completely after 20 years of owner-occupancy, meaning you build equity without repaying a dime if you stay in the home. Income limits cap out at 140 percent of area median income depending on household size, and you’ll need a credit score of at least 600 to qualify.

The back-end debt-to-income ratio maxes at 50 percent, giving you real borrowing power. Priority goes to extremely low, very low, low, and moderate-income households, which influences your assistance amount. Contact the City of Tampa’s Housing and Community Development office at 813-274-7954 to confirm current availability. New reservation packages were placed on hold as of January 7, 2026 due to funding constraints, though the city plans to resume accepting applications once state and federal funds replenish.

Hillsborough County Housing Finance Authority Programs

The Hillsborough County Housing Finance Authority administers two distinct down payment assistance options: the Home Sweet Home Hillsborough Program and the Affordable Income Subsidy Grant. Both programs deliver assistance as a zero-interest second mortgage specifically for down payment and closing costs on your primary residence. These programs target first-time buyers throughout Hillsborough County, including Tampa, and work seamlessly with FHA, VA, and conventional financing. Contact a participating loan officer through the Housing Finance Authority by calling 813-425-5959 or emailing sue@ehousing.cc to discuss your specific situation and review the current Approved Lenders List.

Non-Profit Housing Counseling and CRA Assistance

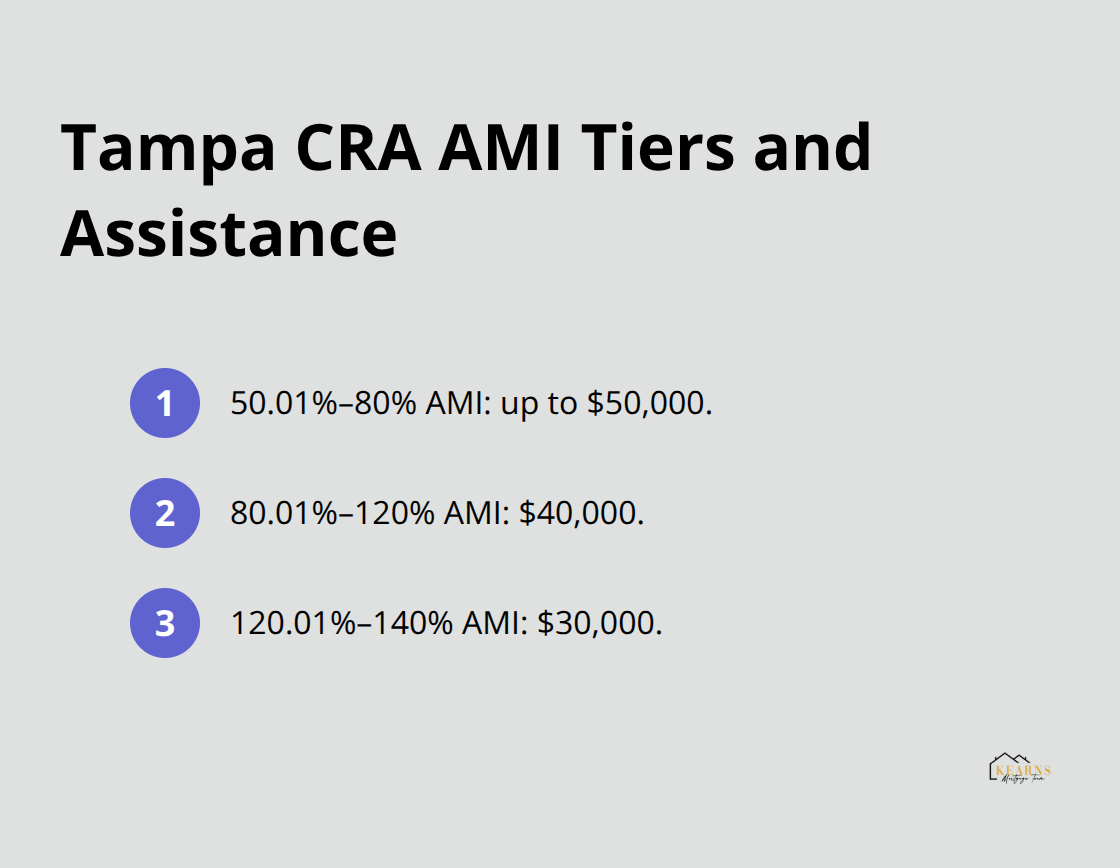

Non-profit housing counseling agencies like Housing and Education Alliance, REACH, Solita’s House, and Tampa Bay Neighborhood Housing Services offer grants and forgivable loans alongside education services. The Tampa CRA Down Payment Assistance Program delivers forgivable second-lien loans up to $50,000 for purchases within designated community redevelopment areas (Channel District, Downtown, East Tampa, and Ybor City). This program requires a minimum $1,000 personal investment and offers full forgiveness after 20 years of owner-occupancy with no monthly payments and zero interest. Income eligibility ranges from 50.01 to 140 percent of area median income, with higher assistance amounts for lower-income households.

Start with the Housing Finance Authority or your local housing counseling agency to understand which programs match your income, credit profile, and target property location. Each program has specific lender networks and application processes that vary based on your circumstances and the property you’re purchasing. Understanding your eligibility across these local options positions you to maximize your down payment assistance before moving forward with your mortgage application.

Eligibility Requirements and Application Process

Income Limits Determine Your Qualification

Income limits form the hard floor for every Tampa first-time homebuyer program, and they vary dramatically depending on household size and which program you choose. The City of Tampa’s Dare to Own the Dream program caps household income at 140 percent of area median income, which translates to roughly $94,000 for a single person and $134,000 for a family of four based on HUD’s 2025 income limits for the Tampa area. The Tampa CRA Down Payment Assistance Program uses a tiered approach: buyers earning 50.01 to 80 percent of AMI receive up to $50,000, those at 80.01 to 120 percent AMI get $40,000, and buyers at 120.01 to 140 percent AMI receive $30,000. Hillsborough County’s Housing Finance Authority programs follow HUD guidelines for first-time buyers, though they don’t publicly specify exact income thresholds.

Credit Scores and Debt-to-Income Ratios

Credit scores matter less than many assume. The Dare to Own the Dream program requires only 600, making it accessible to buyers with past credit challenges. Hillsborough County programs typically demand 620 to 640, still well below the 700-plus scores conventional lenders prefer. Your debt-to-income ratio-the percentage of gross monthly income devoted to debt payments-determines real borrowing capacity. Most Tampa programs allow a maximum back-end DTI of 50 percent, meaning your total monthly debt payments including your new mortgage cannot exceed half your gross income. This 50 percent threshold differs sharply from conventional lending, which caps DTI at 43 percent. That extra 7 percentage points translates to tens of thousands in additional borrowing power for qualified buyers.

Documentation Requirements and Timelines

Documentation requirements separate serious applicants from window shoppers, and lenders move fast when paperwork is complete. You’ll need two years of tax returns, recent pay stubs covering the last 30 days, bank statements showing asset reserves, and a valid government ID. Most programs require proof of homebuyer education completion through an approved counselor-courses typically run four to eight hours and cost between $50 and $150. The City of Tampa Housing and Community Development office at 813-274-7954 confirms eligibility before you invest time in applications.

Application Timelines and Current Status

Timeline pressure is real: the Dare to Own the Dream program halted new reservations on January 7, 2026 due to funding constraints, though the city plans to reopen applications when state and federal funds arrive. Hillsborough County’s Housing Finance Authority at 813-425-5959 processes applications continuously but can take 30 to 45 days from submission to approval. The Tampa CRA Down Payment Assistance Program requires working with approved housing counseling agencies-Housing and Education Alliance, REACH, Solita’s House, or Tampa Bay Neighborhood Housing Services-which adds one to two weeks to the timeline.

Moving Forward with Your Application

Start the conversation with a participating lender immediately; they identify missing items faster than you will and guide you through the exact sequence lenders demand. Don’t wait for perfect documentation (most lenders work with you to complete items as you locate them). Contact the appropriate program office or housing counseling agency based on your income level and target property location to confirm current availability and next steps.

Final Thoughts

You now understand which Tampa first-time homebuyer programs match your income, credit profile, and timeline. Pull your credit report, calculate your household income, and identify which properties you’re targeting to determine your best options. The City of Tampa’s Dare to Own the Dream program works best if you earn under 140 percent of area median income and plan to stay in your home for at least 20 years, while the Tampa CRA Down Payment Assistance Program only applies to purchases within specific redevelopment zones.

Common application mistakes cost buyers thousands in delays or rejections. Submitting incomplete documentation forces lenders to chase you for missing items, extending timelines by weeks, and overstating income or hiding existing debts gets applications denied and damages your credibility with future lenders. The Dare to Own the Dream program halted new reservations on January 7, 2026, and funding constraints affect availability across all programs, so start conversations now rather than waiting until you’ve found your dream home.

Contact Kearns Mortgage Team to review your specific situation and identify your best path forward across Tampa first-time homebuyer programs. Our team knows which lenders participate in each program and how to layer federal, state, and local assistance for maximum impact. We offer free consultations to position you for success.