Buying a home in Tampa comes with more than just a down payment-closing costs typically add 2–5% to your purchase price, catching many first-time buyers off guard. We at Kearns Mortgage Team help buyers understand exactly what they’ll pay at closing so there are no surprises on signing day.

Tampa home buying closing costs break down into several categories, each with specific fees and charges you need to know about. This guide walks you through real cost scenarios, negotiation strategies, and practical ways to reduce what you owe at closing.

What Goes Into Your Tampa Closing Costs

Lender fees make up a substantial chunk of your closing costs, often totaling $1,000 to $3,000 depending on your loan amount and lender. The origination fee is typically the largest component, ranging from 0.5% to 1.5% of your loan amount-on a $300,000 mortgage you could pay $1,500 to $4,500 just for this fee alone. Beyond origination, you’ll encounter an application fee (usually $300 to $500), credit report fee ($50 to $100), and appraisal fee ($450 to $700). Underwriting fees add another $300 to $800 to the total. These fees vary significantly between lenders, which is why shopping around for quotes before committing matters more than most first-time buyers realize. A difference of even 0.25% in origination fees translates to $750 on a $300,000 loan, making lender comparison a concrete way to save money.

Title and Property Examination Costs

Title insurance and examination fees typically run $1,000 to $2,500 depending on your purchase price and any complications with the property’s ownership history. The title search itself costs around $200 and involves a title company reviewing 30 years of public records for unpaid taxes, liens, judgments, and filing errors that could affect your ownership. Owner’s title insurance, which protects you against past title defects after closing, costs approximately $3 to $5 per $1,000 of purchase price. On a $300,000 home, that means $900 to $1,500 for owner’s title insurance alone. Closing or settlement fees charged by the title company typically range from $395 to $800 and can be negotiated as part of your purchase agreement. Most first-time buyers overlook that title-related costs are somewhat negotiable, particularly the settlement fee, which represents a reasonable place to push back during negotiations.

Prepaid Amounts and Escrow Reserves

Your lender requires escrow deposits to cover prepaid property taxes, homeowners insurance, and mortgage insurance if applicable, typically totaling $1,000 to $3,000 at closing. Homeowners insurance premiums for the first year usually run $1,800 to $3,000 depending on location, home age, and hurricane risk exposure. Property taxes are prorated between you and the seller based on your closing date; if you close mid-month, you pay taxes for the remaining days of that month plus the following months until your first annual payment. Documentary stamp tax in Florida costs 70 cents per $100 of the sale price-a $300,000 home incurs approximately $2,100 in doc stamps. If your down payment is less than 20%, you’ll also pay private mortgage insurance at closing, which varies based on your loan-to-value ratio and credit profile. These prepaid items represent actual money your lender holds in escrow to pay bills on your behalf, not fees paid to third parties, which is why understanding the distinction helps you budget more accurately.

How Lender Selection Impacts Your Total

Shopping around for lenders directly affects your bottom line at closing. Different lenders charge different origination fees, application fees, and underwriting costs, so comparing loan estimates from multiple sources can save you thousands. The Consumer Financial Protection Bureau notes that service costs listed in loan estimates represent shop-around targets where you can negotiate or find better rates. A lender offering a 0.75% origination fee versus 1.25% saves you $1,500 on a $300,000 loan. Request loan estimates from at least three lenders and compare the exact fees line by line rather than focusing solely on interest rate. This approach reveals which lender offers the best overall value for your specific situation.

Now that you understand what makes up your closing costs, the next section shows you exactly what to expect at different price points across the Tampa market.

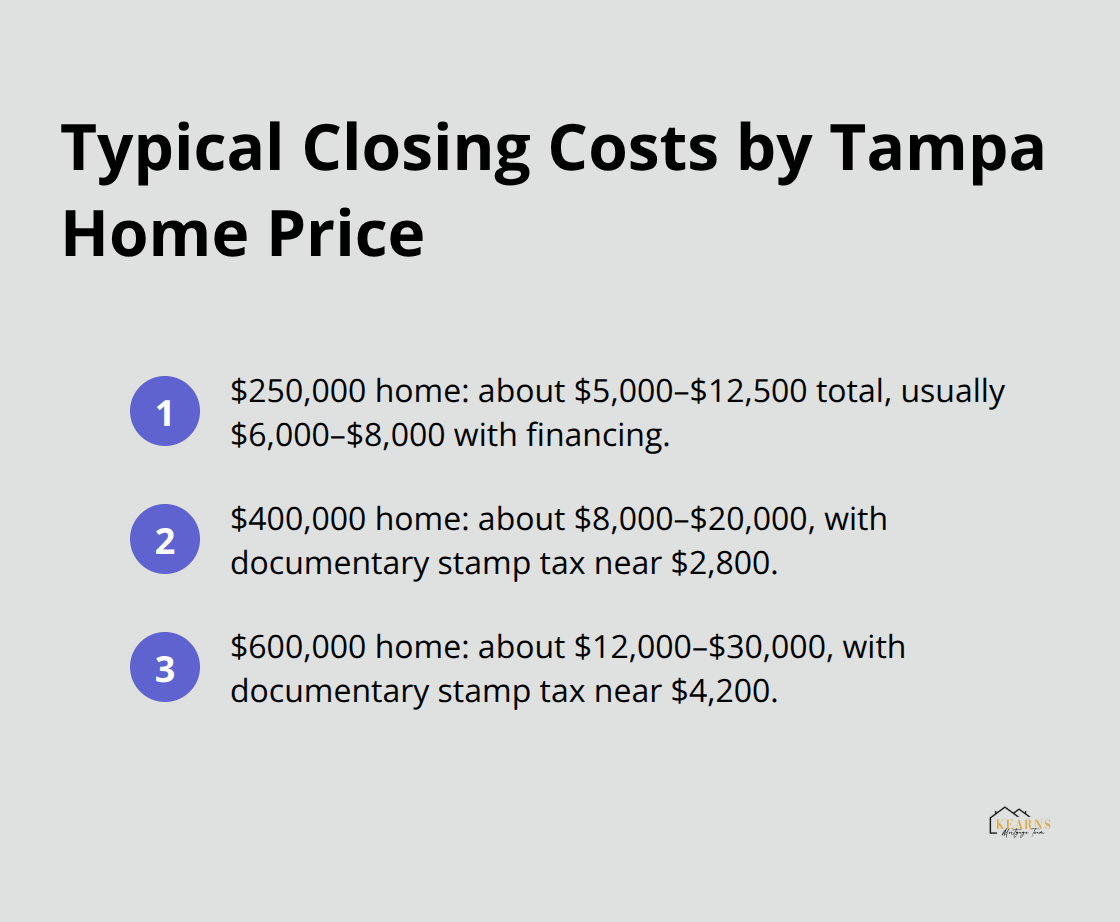

Sample Closing Cost Scenarios by Home Price

A $250,000 home in Tampa typically generates closing costs between $5,000 and $12,500, with most buyers landing around $6,000 to $8,000 for a conventional loan. Your lender fees alone run $1,500 to $2,500, the title package costs $1,000 to $1,500, and prepaid items including homeowners insurance and escrow deposits consume another $2,000 to $4,000. Documentary stamp tax at 70 cents per $100 adds roughly $1,750 to your bill. Property tax proration depends entirely on your closing date, but expect $300 to $600 for a mid-year closing. If you put down less than 20 percent, private mortgage insurance adds another $500 to $1,200 depending on your loan-to-value ratio. The reality most first-time buyers miss is that the 2 percent floor applies mainly to cash purchases or significant down payments-you’ll realistically hit 3 to 4 percent for a financed purchase on a $250,000 home.

The $400,000 Home Reality

A $400,000 purchase price pushes your closing costs into the $8,000 to $20,000 range, and this is where lender selection becomes genuinely impactful. Lender fees scale similarly at $1,500 to $3,000, but title insurance jumps to $1,200 to $2,000 because it’s calculated on the purchase price.

Documentary stamp tax reaches approximately $2,800, and your escrow deposits for insurance and taxes climb to $2,500 to $4,500. The difference between a lender charging 0.75 percent origination versus 1.25 percent suddenly costs you $2,000 instead of $1,500. At this price point, negotiating seller concessions becomes genuinely worthwhile-asking the seller to cover $3,000 to $5,000 in closing costs is standard practice in a balanced market and saves you real money without extending the negotiation timeline significantly.

The $600,000 Home and Scaling Costs

A $600,000 home generates $12,000 to $30,000 in closing costs, with the upper range reflecting properties with more complex title histories or those in higher-risk hurricane zones requiring additional insurance reserves. Lender fees reach $2,000 to $4,000, title insurance alone costs $1,800 to $3,000, and documentary stamp tax totals approximately $4,200. Your escrow deposits for insurance and taxes can exceed $5,000, particularly if you close early in the year when prepaid amounts run highest. At this price point, the difference between lenders becomes substantial-0.5 percent origination fee variation equals $3,000 on a $600,000 loan. Higher-priced properties in areas like Davis Islands or South Tampa often carry additional county recording fees and special assessments that inflate the final bill, making a detailed loan estimate from your lender absolutely non-negotiable before proceeding. Negotiating seller concessions covering 2 to 3 percent of the purchase price is realistic and expected in competitive situations.

How Price Point Changes Your Negotiation Strategy

The higher your purchase price, the more leverage you have to negotiate closing costs with sellers and lenders. On a $250,000 home, asking for $2,000 in seller concessions represents less than 1 percent of the sale price and often meets resistance. On a $600,000 home, that same $2,000 request represents just 0.33 percent and sellers typically accommodate it without hesitation. Lender fee differences also compound at higher price points-a 0.5 percent origination fee variation costs $1,500 on a $300,000 loan but $3,000 on a $600,000 loan, making your comparison shopping efforts yield substantially larger savings. These price-point realities shape how aggressively you should negotiate and which fees warrant your attention during the closing process.

How to Cut Your Closing Costs Before Signing Day

Closing costs represent real money leaving your pocket, and the strategies that work depend entirely on your price point and market timing. The most effective approach combines three concrete actions: comparing lender fees line by line, negotiating seller concessions tied to your offer, and identifying first-time buyer assistance that reduces your burden. None of these strategies require luck or timing-they require preparation and willingness to ask for what you want.

Comparing Lenders Delivers Measurable Savings

Your lender choice directly determines $1,500 to $4,000 of your closing costs, yet most first-time buyers contact only one or two lenders before committing. Request loan estimates from at least three lenders and compare origination fees, application fees, underwriting charges, and appraisal costs line by line. The Consumer Financial Protection Bureau identifies service costs in loan estimates as legitimate shop-around targets where real negotiation happens. A lender charging 0.75 percent origination versus 1.25 percent saves you $1,500 on a $300,000 loan-that’s a $1,500 difference for making three phone calls. On a $600,000 loan, that same fee variation equals $3,000. Request quotes on the same loan amount and terms so comparisons remain apples-to-apples. Some lenders offer origination fee credits in exchange for a higher interest rate; calculate the long-term cost of that trade-off before accepting it. Title insurance shopping matters less because Florida regulates title insurance rates, but settlement fees charged by title companies range from $395 to $800 and warrant negotiation during your offer stage. Ask your real estate agent to include a request for the seller to cover settlement fees as part of your purchase contract-this costs the seller nothing if they’ve already committed to a specific title company.

Seller Concessions Reduce Your Out-of-Pocket Cash

Negotiating the seller to cover closing costs requires strategic timing within your offer rather than requesting it at closing. On a $250,000 home, asking for $2,000 in seller concessions (0.8 percent) often meets resistance in competitive markets. On a $400,000 home, requesting $3,000 to $5,000 (0.75 to 1.25 percent) represents standard practice and sellers typically accommodate it without extending negotiations. On a $600,000 home, negotiating 2 to 3 percent of the purchase price in seller concessions is realistic and expected when properties sit on the market. Include concession requests within your initial offer rather than raising them after inspection-sellers evaluate concessions as part of the overall deal and respond more favorably. Concessions can cover lender fees, title insurance, documentary stamp taxes, or escrow deposits. Specify exactly which fees the seller covers rather than requesting a lump sum, because this clarity prevents disputes at closing. FHA loans allow sellers to contribute up to 6 percent toward closing costs, conventional loans with 10 percent down permit 6 percent seller concessions, and conventional loans with 20 percent down allow 3 percent-knowing your loan program’s limits prevents you from requesting something your lender won’t accept.

First-Time Buyer Programs Offset Real Costs

Florida and Hillsborough County offer first-time homebuyer assistance programs that reduce closing costs through grants or down payment assistance, yet most buyers never investigate them. The State Housing Finance and Development Authority administers programs offering grants up to $15,000 for closing costs and down payments, though income limits apply. Contact your local community development office or nonprofit housing organizations to identify programs matching your income and purchase price. Some programs require homebuyer education courses, which cost $50 to $150 but qualify you for assistance worth thousands. VA loans eliminate closing costs entirely for eligible veterans-the VA guarantees the loan and lenders typically waive origination fees for VA borrowers, saving $1,500 to $3,000 at closing. If you’re a veteran, this advantage alone makes VA loans worth exploring even if conventional financing initially seemed appealing. Credit unions sometimes offer closing cost assistance or reduced fees for members, so check whether you qualify for membership at a local Tampa credit union. First-time buyer programs rarely advertise aggressively, which means your real estate agent or mortgage professional becomes your best resource for uncovering them.

Final Thoughts

Understanding Tampa home buying closing costs removes the guesswork from your purchase and puts you in control of your finances at closing. Closing costs scale predictably with your home price, ranging from $5,000 on a $250,000 purchase to $30,000 on a $600,000 home, and these costs aren’t fixed-lender selection alone saves you $1,500 to $3,000, seller concessions reduce your out-of-pocket expenses by thousands more, and first-time buyer programs can offset closing costs entirely if you qualify. Your mortgage professional becomes invaluable because they understand which fees are negotiable, which lenders offer competitive rates for your specific situation, and which assistance programs match your income and loan type.

Request loan estimates from multiple lenders immediately-this single action typically saves buyers $1,500 to $3,000 and takes just a few phone calls. Include seller concession requests in your initial offer rather than waiting until later in the process, because sellers respond more favorably when concessions are part of the overall deal structure. Investigate first-time buyer assistance programs through your local community development office or nonprofit housing organizations, as these programs can eliminate a significant portion of your Tampa home buying closing costs.

We at Kearns Mortgage Team help first-time buyers navigate these decisions by providing personalized guidance, competitive rates, and transparent cost breakdowns before you commit to anything. Contact Kearns Mortgage Team to discuss your specific situation and get a detailed closing cost estimate tailored to your purchase price and loan program.