VA loan approval doesn’t have to be complicated. We at Kearns Mortgage Team have helped countless veterans navigate this process, and we know exactly where delays happen and how to prevent them.

The right preparation makes all the difference. This guide gives you the VA loan approval tips and checklists you need to move through certification faster and get closer to homeownership.

What Makes You VA Loan Eligible

Get Your Certificate of Eligibility First

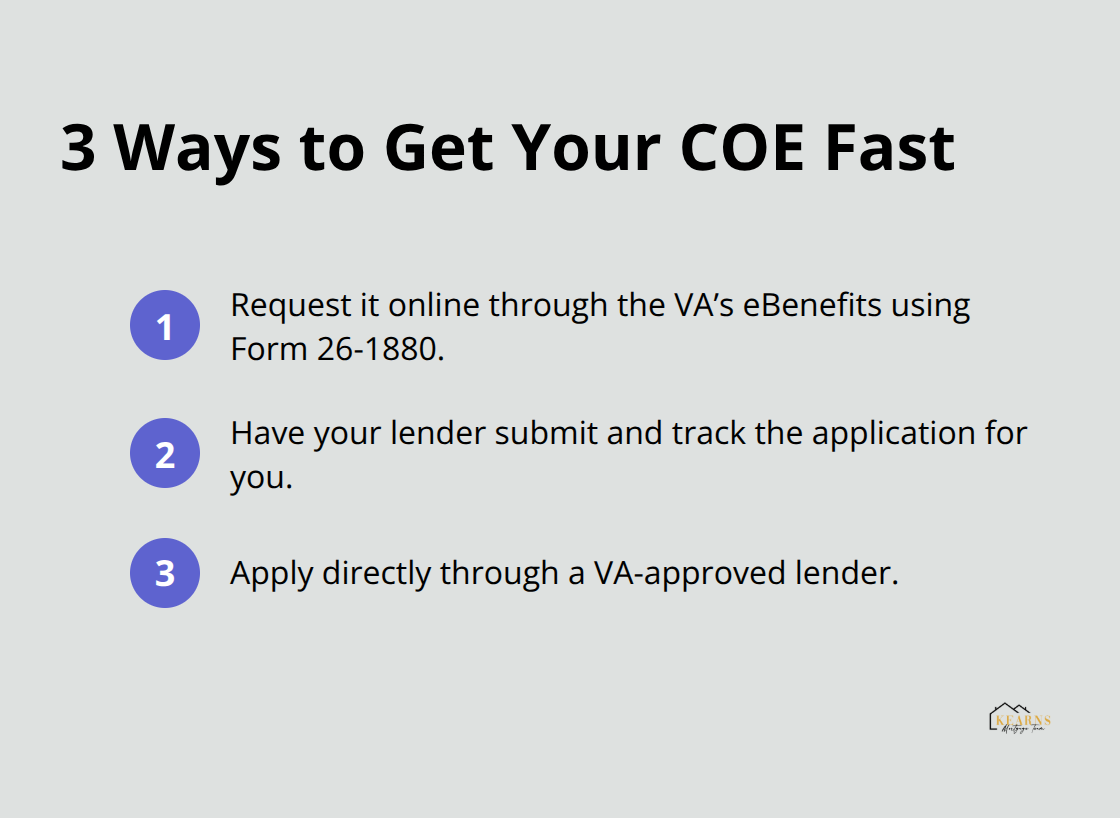

Your Certificate of Eligibility forms the foundation of your VA loan application, and obtaining it early removes one of the biggest bottlenecks in the approval process. You can obtain your COE in three ways: request it online through the VA’s eBenefits portal using Form 26-1880, have your lender submit the application for you, or apply directly through a VA-approved lender. The fastest approach involves having your lender handle it, since they submit it immediately and monitor its status throughout your application.

Your COE proves to lenders that you meet the VA’s basic service requirements, and without it, nothing moves forward. According to the VA, keeping an active COE on hand before you even start shopping eliminates weeks of waiting later.

Verify Your Service Record and Discharge Status

Your service record determines your eligibility more than anything else. If you served 24 continuous months of active duty from the Gulf War period to now, you qualify automatically. If you were discharged earlier due to hardship, medical conditions, a service-connected disability, or government convenience, the VA may still approve you even with less time in uniform. National Guard and Reserve members need either 90 days of non-training active-duty Title 10 service or six creditable years in the Selected Reserve with honorable discharge. Your discharge status matters significantly-an other-than-honorable, bad conduct, or dishonorable discharge typically disqualifies you unless you successfully pursue a discharge upgrade or VA Character of Discharge review. Gather your DD-214 or Statement of Service now rather than waiting until you apply.

Understand Income and Credit Score Expectations

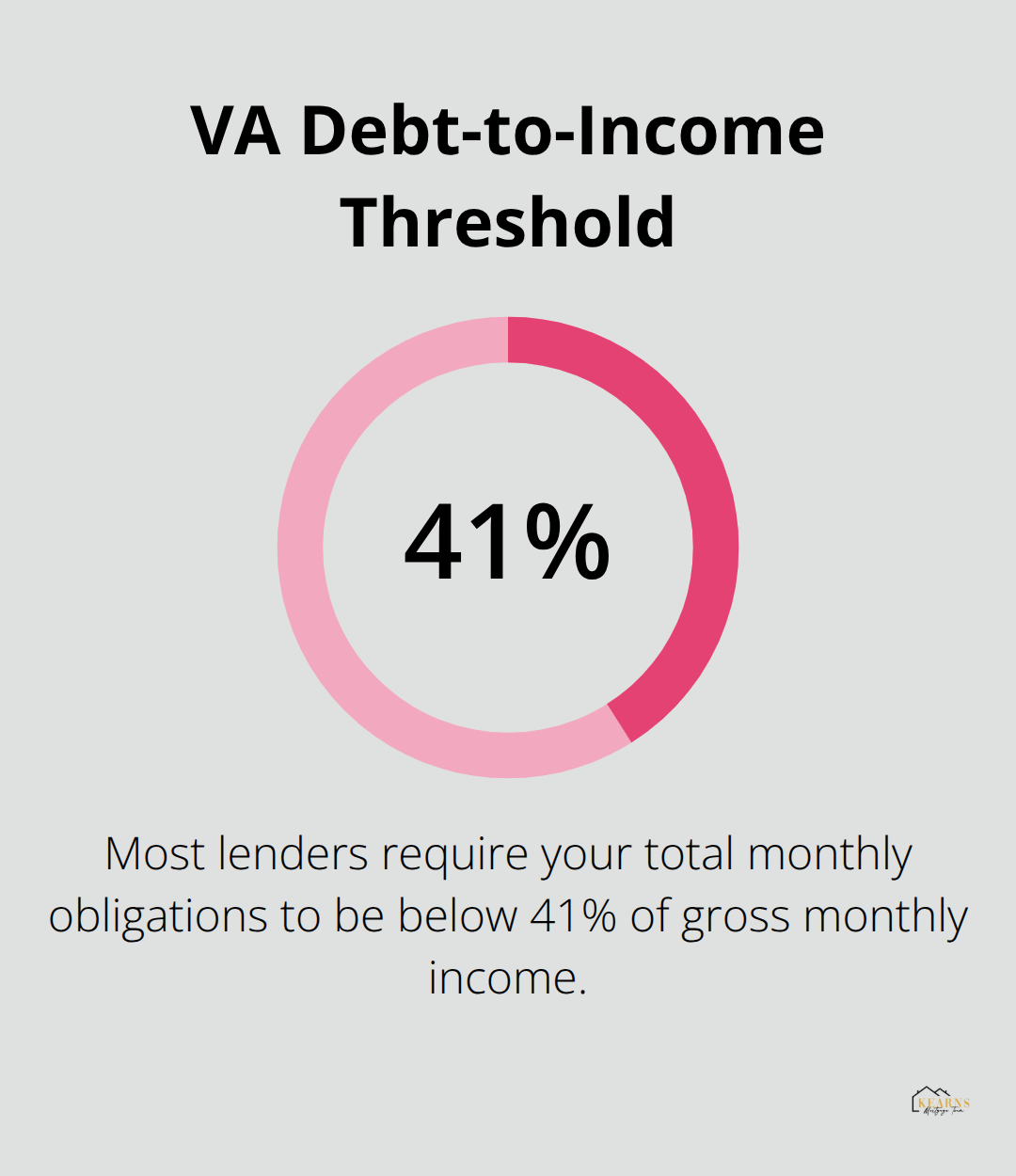

Income and credit scores are secondary factors that lenders evaluate, but they’re not dealbreakers like eligibility is. Most VA lenders work with credit scores as low as 580 to 620, though scores above 740 get you better interest rates. Your income needs to cover your housing payment plus existing debts, with most lenders requiring a debt-to-income ratio below 41 percent (meaning your total monthly obligations shouldn’t exceed 41 percent of your gross monthly income).

These financial factors matter, but your service record and discharge status carry far more weight in the approval decision. With your eligibility confirmed and your financial picture clear, you’re ready to compile the specific documents your lender will request.

Document Preparation for VA Loan Success

Gathering the right documents before you submit your application is the single fastest way to avoid delays. Lenders request specific paperwork to verify your identity, income, employment history, and financial stability, and having everything ready means your application moves through underwriting without stalling for missing items. Print or scan every page of your financial documents in full clarity-lenders reject incomplete or illegible submissions and request them again, which costs you weeks. Incomplete documentation can slow your application, so treat document preparation as seriously as your eligibility verification.

Military Service Documentation

Your military service documentation forms the first foundation. Gather your DD-214 or Statement of Service immediately, as lenders use this to confirm your service dates and discharge status match your COE. If you have a VA disability award letter, include it because it strengthens your eligibility verification and can support income claims if you receive disability compensation. For proof of identity, bring a government-issued driver’s license or passport for all applicants on the loan.

Income and Employment Records

Compile two years of W-2 statements and your most recent pay stubs to establish your income history and current employment status. If you are self-employed, supply two years of federal tax returns, 1099 forms, and any Schedule E documentation for rental or commission income. Your lender will request bank statements from checking, savings, and retirement accounts-print every single page, not just a summary, because lenders verify liquid assets available for down payment and closing costs.

Additional Financial and Legal Documents

If you have a divorce decree showing alimony or child support obligations, include it. If you have filed bankruptcy, provide your discharge letter and full bankruptcy history. Having these documents ready before submission helps keep your approval moving forward, and many lenders will not even schedule your closing without them.

Organize and Submit as a Complete Package

Gathering complete financial records upfront allows underwriters to begin work on your file promptly. This approach transforms your application from reactive to proactive, positioning you ahead of other applicants who submit documents piecemeal. With your documentation organized and ready, you can now focus on selecting the right lender and understanding how to keep your approval moving forward without unnecessary delays.

Accelerating Your VA Loan Approval Process

Your lender choice directly impacts your approval timeline. A VA-savvy lender understands the nuances of VA loans that conventional lenders often miss, and this expertise translates into faster processing. According to ICE Mortgage Technology data, VA loan closings typically take 60 to 90 days, compared to 45 days for conventional loans. That gap exists partly because not all lenders prioritize VA applications equally. Some lenders treat VA loans as secondary to conventional business because they earn less on them, which means your application sits in queue longer.

Selecting a Lender With VA Expertise

When you select a lender, ask directly how many VA loans they close monthly and request to speak with their VA specialist, not just a loan officer. A lender closing 50 or more VA loans per month has systems, templates, and experienced underwriters who know exactly what works. They flag issues early, request documents proactively rather than reactively, and understand VA-specific appraisal requirements that can derail inexperienced lenders. Your lender should also offer online document submission and provide a dedicated point of contact who monitors your file status weekly. If your lender requires you to call and ask for updates, you’ve chosen poorly. The best VA lenders send you status updates automatically and alert you immediately when they need additional information.

Prevent Common Appraisal and Documentation Delays

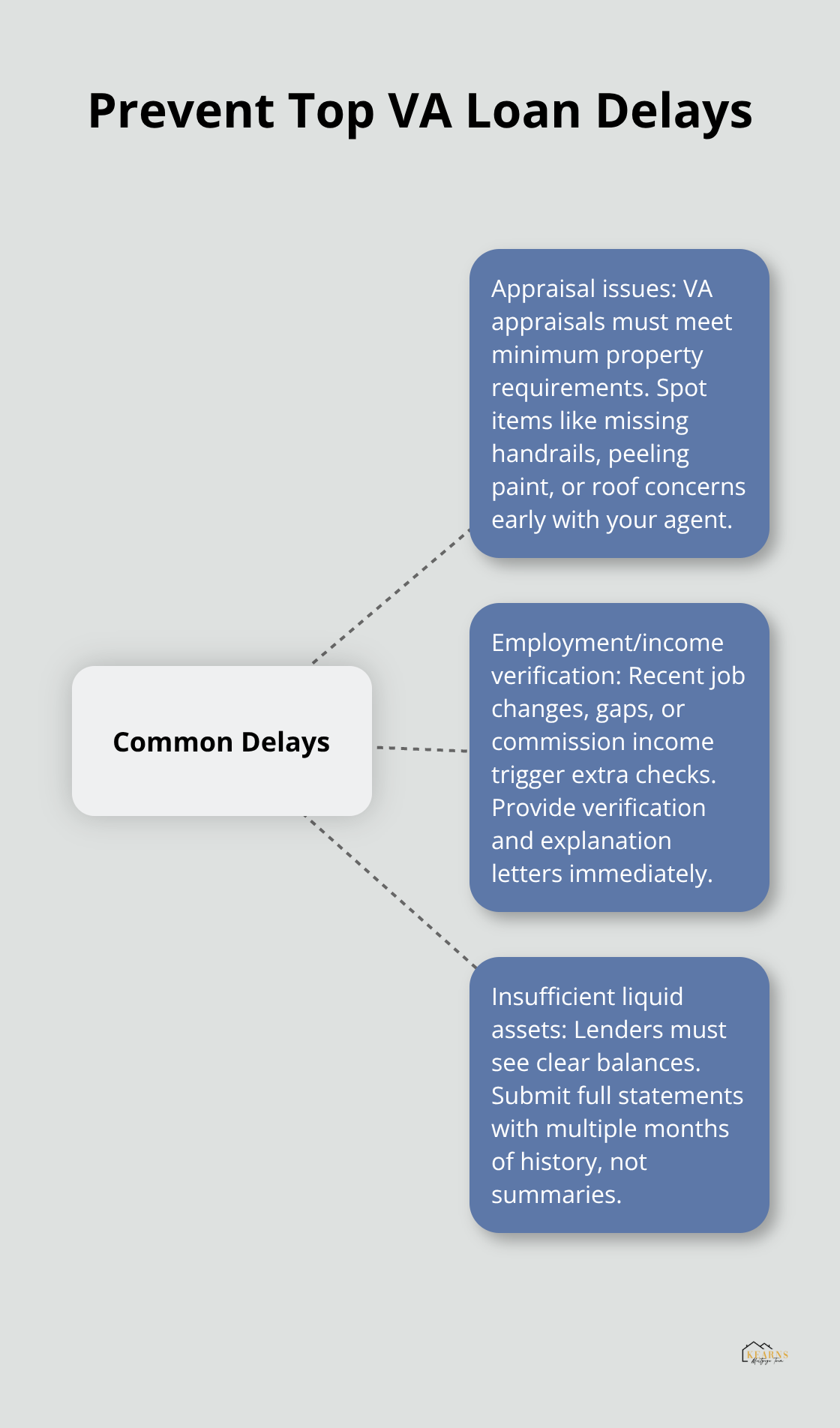

Common delays fall into predictable patterns that you can prevent with upfront communication. Appraisal issues rank among the top delays in VA lending. The VA requires that properties meet minimum property requirements, and appraisers sometimes flag issues like missing handrails, peeling paint, or roof concerns that wouldn’t disqualify a conventional loan. Before you make an offer, understand that VA appraisals are more in-depth and must meet minimum property requirements. Work with your real estate agent to identify potential appraisal red flags early and address them in your offer negotiations.

Another major delay happens when lenders discover employment gaps or income inconsistencies during underwriting. If you changed jobs within the past two years, your lender will want verification from both employers and an explanation letter from you. If you have commission-based income, expect requests for two years of tax returns plus last quarter’s income documentation. Provide this information immediately when asked, not after your lender sends a second request. Missing documents get requested once, then twice, then your file gets deprioritized.

The third delay pattern involves insufficient liquid assets. Your lender needs to verify that you have funds available after closing for emergencies. If your bank statements don’t clearly show account balances, print full statements with multiple months of history.

Many applicants delay approval by submitting summaries instead of complete statements, forcing lenders to request them again.

Drive Your Own Timeline With Active Communication

Passive applicants wait for updates; active applicants drive their own timelines. After you submit your application, contact your lender’s VA specialist within two business days and ask for a preliminary review timeline. Most lenders can tell you within 48 hours if your file is clean or if issues exist. Ask specifically: will the appraisal delay my closing, do you see any employment verification problems, and do you have everything you need from me right now. This conversation prevents surprises and lets you address problems immediately.

Check your loan file status online at least weekly if your lender offers a portal. If they don’t offer online status tracking, that’s another sign you chose the wrong lender. Request a list of everything your lender needs from you in writing, then deliver it all at once rather than trickling documents over weeks. When your lender requests additional information, respond within 24 hours, not five days. Lenders process files in batches, and if you miss the weekly underwriting batch, your file waits another week. Your responsiveness directly controls your timeline.

Align Expectations Across Your Transaction

Understand that your real estate transaction timeline isn’t your lender’s only deadline. Your seller has expectations, your appraiser has a schedule, and your title company has closing dates. Communicate your VA loan timeline to all parties upfront. Most sellers accept VA loans today because assumable mortgages are gaining popularity according to HousingWire, but only if they understand the realistic 60 to 90 day closing window. Managing expectations prevents pressure that creates mistakes.

Final Thoughts

VA loan approval tips work best when you treat preparation as your competitive advantage. You now have the checklist to gather your Certificate of Eligibility, organize your financial documents, and select a lender who prioritizes VA applications. The difference between a 60-day closing and a 90-day closing often comes down to whether you submitted complete documentation upfront and stayed actively engaged with your lender throughout the process.

Your next step is straightforward: request your COE today if you haven’t already, then compile your military service records and financial statements. Contact a VA-savvy lender and ask them directly how many VA loans they close monthly and whether they offer online status tracking. These conversations take 30 minutes and eliminate months of potential frustration later.

If you’re ready to move forward, contact Kearns Mortgage Team for a personalized review of your VA loan options. We’ll walk you through every step and make sure you understand exactly what to expect. What’s holding you back from starting your homeownership journey right now?