Mortgage rates today in Florida are shifting constantly, and understanding where they stand right now matters for your financial decisions.

We at Kearns Mortgage Team know that rate shopping can feel overwhelming, especially when you’re juggling multiple factors that affect your personal offer. This guide breaks down the current rate environment, shows you what influences your specific rate, and reveals concrete strategies to lock in the best deal possible.

Where Do Florida Mortgage Rates Stand Right Now?

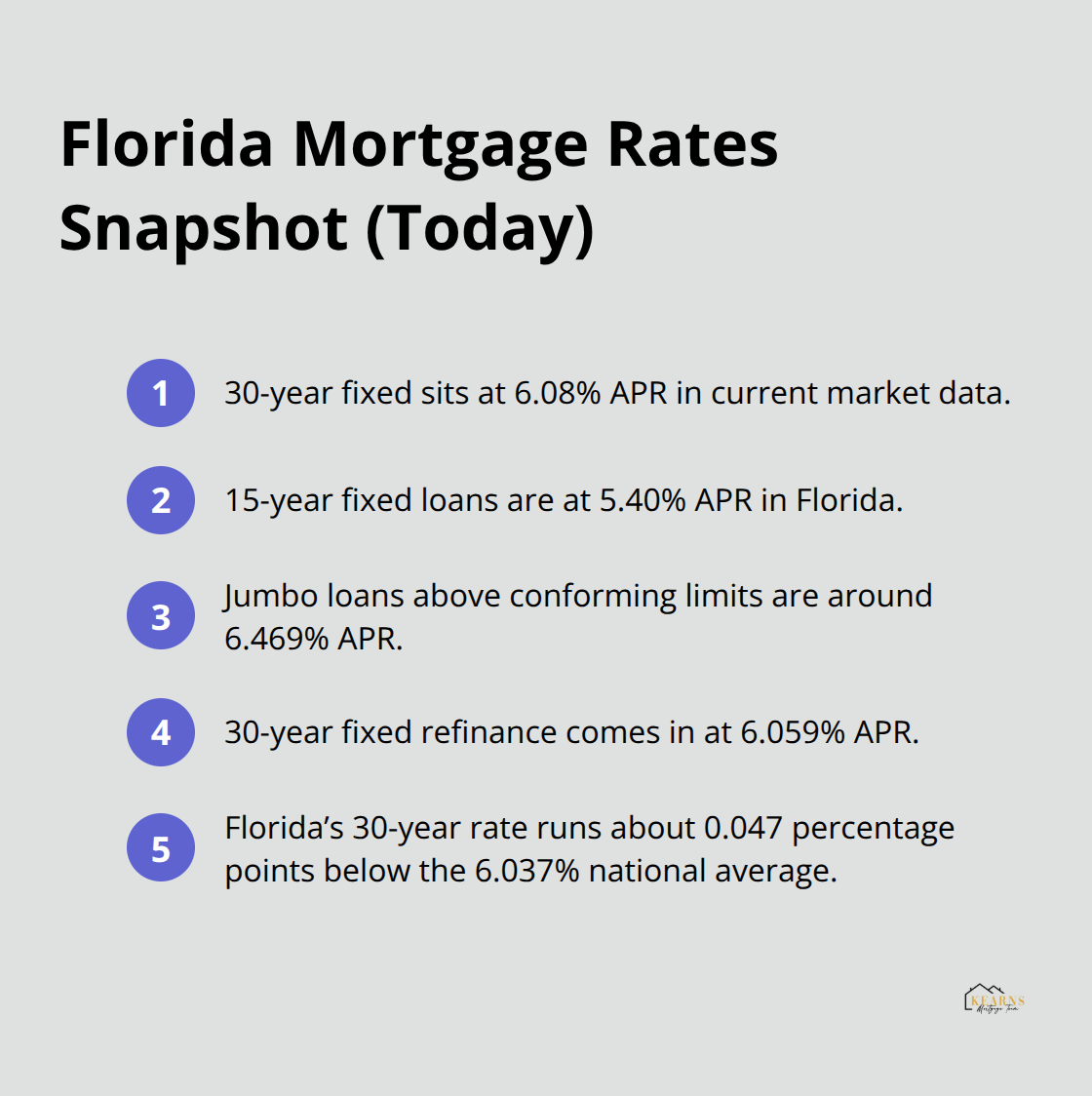

Today’s Florida mortgage landscape shows a 30-year fixed rate at 6.08% APR, with 15-year fixed loans sitting at 5.40% APR according to current market data. For those considering jumbo loans above conforming limits, expect rates around 6.469% APR. If you’re refinancing, a 30-year fixed refinance comes in at 6.059% APR. These rates represent a meaningful shift from three months ago-the 30-year fixed has dropped roughly 0.164 percentage points over that period, signaling a cooling trend that benefits borrowers who act now. The Florida market currently sits slightly ahead of national averages, with our state’s 30-year rate running about 0.047 percentage points below the national average of 6.037% APR. This small advantage matters when you finance a typical Florida home priced around $403,000 with a median down payment of approximately $61,885.

Small weekly fluctuations in rates can swing your monthly payment by $50 to $100 or more over the life of your loan, so timing and rate shopping aren’t luxuries-they’re necessities.

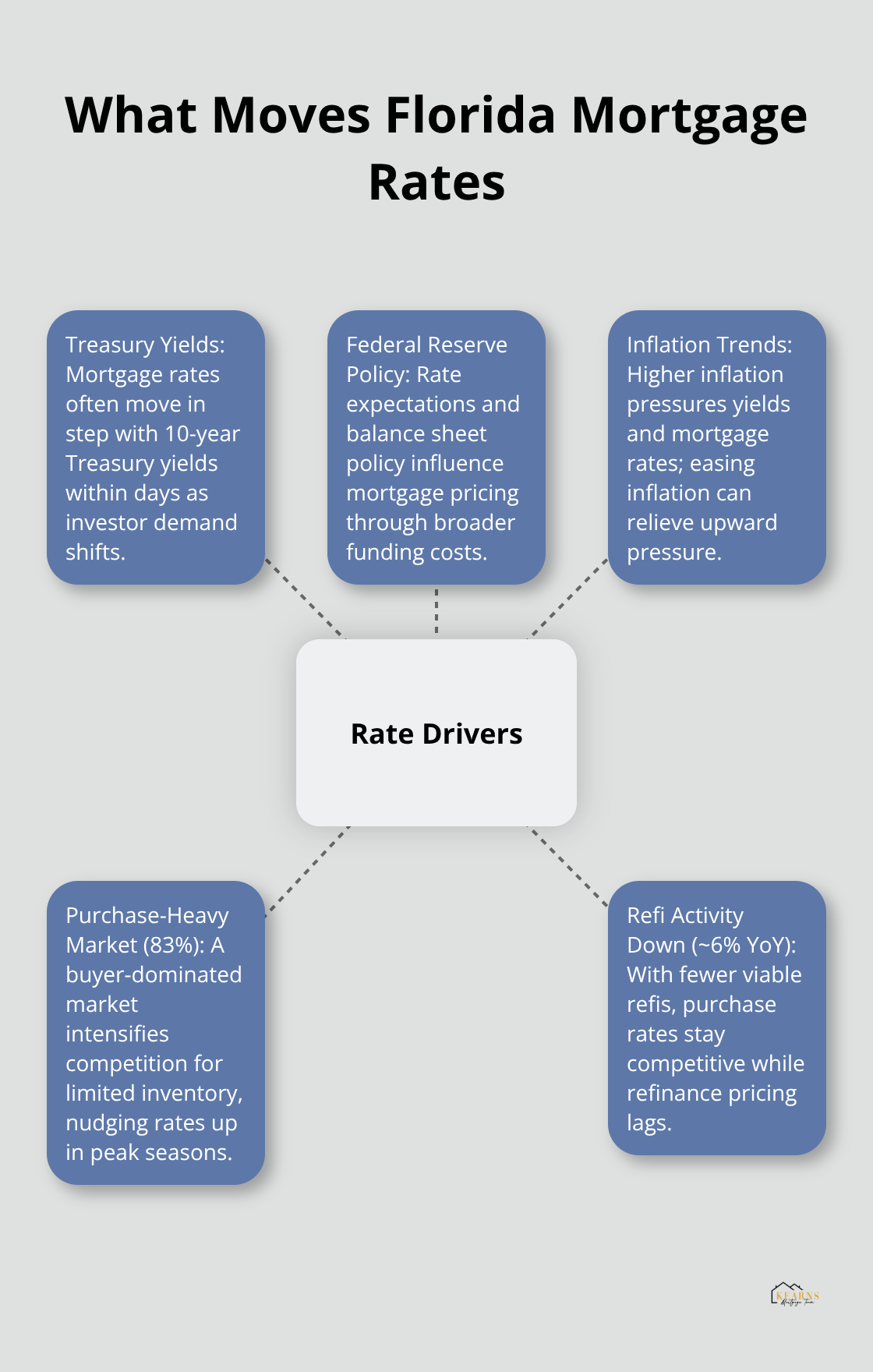

What Drives Rate Movement in Florida

The primary forces behind Florida’s current rates stem from 10-year Treasury yields, Federal Reserve policy decisions, and national inflation trends.

When Treasury yields rise, mortgage rates typically follow within days. Florida’s purchase-heavy market, where 83% of originations are purchase loans rather than refinances, means that active homebuyers compete for limited inventory, which can put upward pressure on rates during peak seasons. The state’s refinance activity has stagnated significantly, with refinance volume declining roughly 6% year-over-year, suggesting that most homeowners who could benefit from refinancing have already done so. This creates an asymmetrical market where purchase rates stay competitive while refinance rates lag.

How Property Type and Insurance Affect Your Rate

Florida’s homeowners insurance crisis adds hidden costs to monthly payments that lenders factor into risk assessments, sometimes resulting in slightly higher rates for borrowers in high-risk insurance zones. Property type also influences your rate-planned unit developments make up nearly half of Florida originations at 49.1%, while single-family homes account for 37.7%, and condos represent 11.5%. Lenders price these differently based on historical performance and secondary market demand, so your specific property type can shift your offer by 0.25% to 0.5% APR. Understanding these variables positions you to anticipate what your lender will quote and where you might find advantages in the market.

What Shapes Your Individual Rate

Your personal mortgage rate diverges from the headline Florida average because lenders assess your specific financial profile against their underwriting standards. Credit score stands as the single most powerful lever you control. Conventional loans typically require a minimum FICO score around 620 to qualify, but competitive rates demand substantially higher scores-lenders reserve their best pricing for borrowers with 740 or above, often resulting in rate advantages of 0.5% to 1.0% APR compared to someone at 680. FHA loans offer more flexibility, accepting credit scores as low as 580 and requiring just 3.5% down, but this accessibility comes with mortgage insurance costs built into your monthly payment. If your credit score sits below 700, three to six months of focused debt reduction and credit report disputes can shift your rate offer by meaningful amounts before you apply.

How Down Payment Size Impacts Your Rate

Down payment size directly influences both your rate and whether you’ll carry private mortgage insurance. The typical Florida homebuyer puts down approximately $61,885 on a $403,000 median-priced home, representing about 15% of the purchase price. Reaching 20% down eliminates PMI entirely and unlocks better rates, sometimes shaving 0.25% to 0.375% from your APR. VA loans present a distinct advantage here-active military and veterans often qualify with zero down payment and funding fees ranging from 1.25% to 2.15% for first-time purchases, making homeownership accessible without accumulating PMI costs that drain equity in early years.

Debt-to-Income Ratio and Loan Term Selection

Your debt-to-income ratio, loan term selection, and property type complete the underwriting picture. Most lenders look for a DTI ratio below 43%, though lower is often better. If you carry student loans, auto payments, or credit card balances, these reduce the mortgage amount you can qualify for and sometimes trigger slightly higher rates as compensation for perceived risk. Choosing between a 30-year and 15-year term shapes your rate immediately-15-year fixed loans in Florida currently sit at 5.40% APR versus 6.08% for 30-year fixed, appearing cheaper until you calculate the monthly payment difference. The 15-year term demands roughly 50% higher monthly payments despite the lower rate, so most Florida borrowers gravitate toward 30-year financing. However, if you can afford the 15-year payment, you’ll build equity twice as fast and save substantial interest over the loan’s life.

Jumbo Loans and Property Type Considerations

Jumbo loans above conforming limits-currently priced around 6.469% APR-carry higher rates because secondary market demand is thinner and lenders require larger down payments, typically 10% minimum, plus fortress-level credit profiles. Property type matters more than many borrowers realize; planned unit developments comprise 49.1% of Florida originations but sometimes carry slightly different pricing than single-family homes due to HOA considerations and secondary market preferences. Shopping rates across multiple lenders reveals how dramatically these factors compound-a borrower with a 700 credit score, 15% down, and a condo purchase receives a different offer than someone with 760 credit, 25% down, and a single-family home, even when both apply on the same day.

The Rate Shopping Advantage

These variables interact in ways that make rate shopping essential rather than optional. Your lender’s appetite for your specific profile-your credit tier, down payment percentage, property type, and loan amount-determines whether you land at the top or bottom of the rate range. One lender might price your scenario at 5.95% while another quotes 6.35% for identical terms, a difference that costs tens of thousands over 30 years. Understanding how credit scores, down payments, debt ratios, and loan terms stack together positions you to anticipate what lenders will offer and where you hold negotiating power. When you’re ready to shop, you’ll know exactly which factors work in your favor and which ones require attention before you submit applications.

How to Lock in Florida’s Best Mortgage Rate

Compare Quotes Across Multiple Lenders

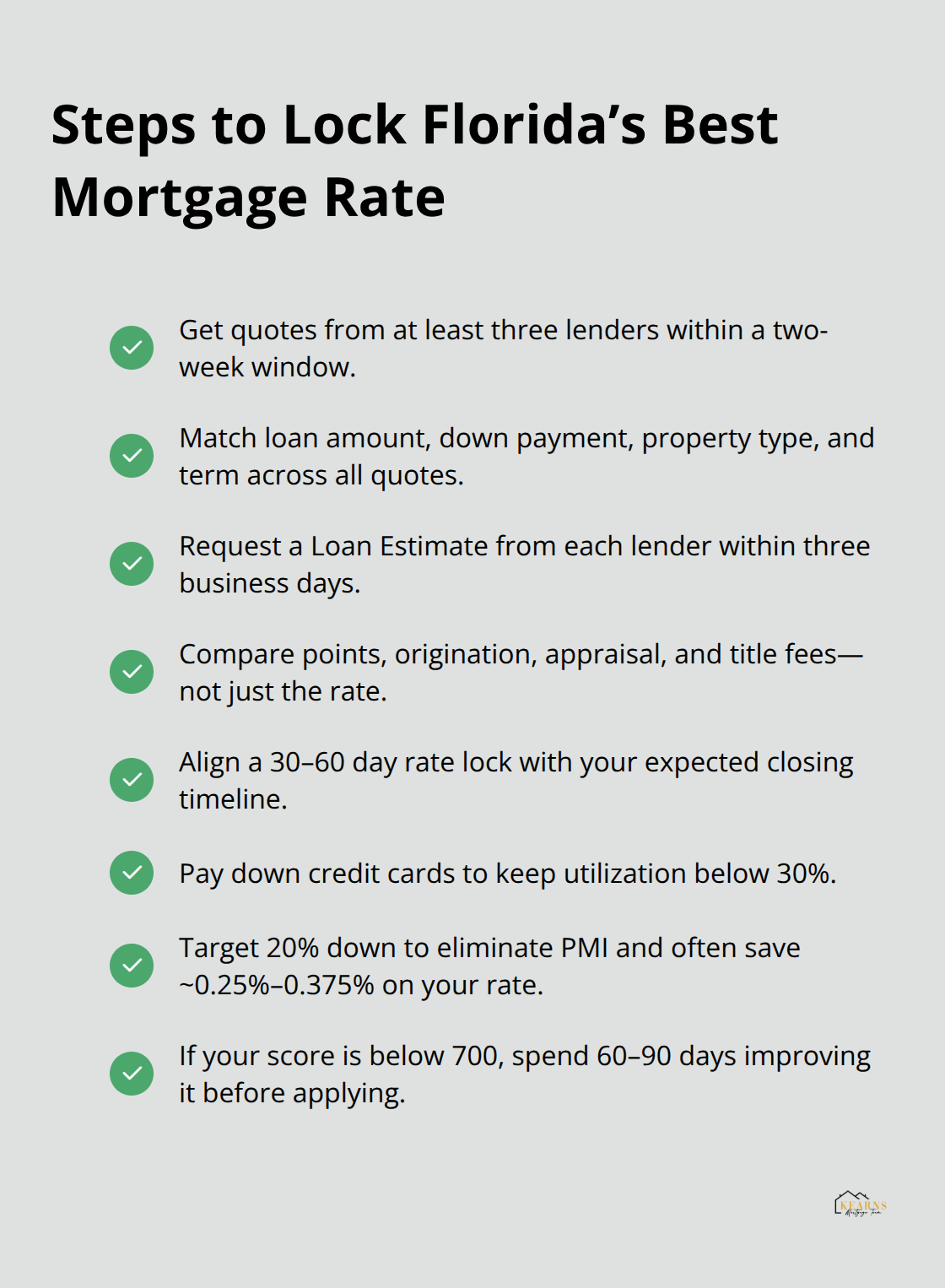

Shopping rates across multiple lenders isn’t optional if you want to avoid leaving thousands on the table. The difference between the best and worst quotes for an identical loan scenario can easily reach 0.4% to 0.5% APR, which translates to $80 to $120 monthly on a $327,284 average Florida loan balance. Gather quotes from at least three different lenders within a two-week window, since mortgage rates shift daily and you want apples-to-apples comparisons. Each quote should specify the same loan amount, down payment percentage, property type, and loan term so you can isolate the actual rate difference from changes in your application details.

Online lenders, traditional banks, and credit unions often price differently based on their risk appetite and secondary market relationships, so a bank that quotes 6.25% might genuinely offer better pricing than a lender quoting 6.05% when you factor in closing costs and origination fees. Request a Loan Estimate from each lender, which federal regulations require them to provide within three business days. The Loan Estimate reveals not just the interest rate but also points, origination fees, appraisal costs, and title insurance charges that dramatically affect your true borrowing cost.

Evaluate Total Costs, Not Just the Rate

Some lenders discount points aggressively to win business while padding closing costs elsewhere, so comparing the total cost to close matters more than fixating on the headline rate alone. A lender offering 5.95% with $8,000 in closing costs costs more than one quoting 6.05% with $5,500 in closing costs over the life of your loan. Calculate the total amount you’ll pay at closing and factor that into your decision alongside the monthly payment difference.

Time Your Rate Lock Strategically

Timing your rate lock requires balancing market momentum against personal readiness. If rates have declined 0.1% to 0.2% over the past week and Treasury yields are stable, lock in immediately to protect yourself from upward movement while capturing recent gains. Conversely, if volatility is high and economic data suggests rates might fall further, floating for a few days costs nothing except the risk of rate movement against you. Most lenders offer rate locks between 30 and 60 days, which aligns with typical closing timelines for purchase transactions.

Before you lock, confirm your credit score remains stable, your employment status hasn’t changed, and your financial profile hasn’t shifted in ways that might trigger a rate adjustment at underwriting.

Strengthen Your Financial Profile First

Strengthening your financial position before applying yields tangible results. Pay down credit card balances to lower your utilization below 30%, eliminate small debts to improve your debt-to-income ratio, and correct errors on your credit report. These actions collectively shift your rate offer by 0.25% to 0.5% APR. If your credit score sits below 700, spend 60 to 90 days building it upward-this costs nothing and frequently unlocks better pricing than applying immediately.

The same principle applies to down payment size: reaching 20% down eliminates PMI and typically saves 0.25% to 0.375% on your rate, so accumulating an extra 5% down over three to six months often makes financial sense compared to accepting PMI costs that drain equity unnecessarily.

Final Thoughts

Florida’s mortgage rates today in Florida shift constantly, but your financial profile determines whether you capture the best offers or settle for mediocre pricing. Gather Loan Estimates from at least three lenders within a two-week window, compare total closing costs alongside the headline rate, and lock in when market conditions align with your readiness. Before you apply, audit your credit report for errors, pay down credit card balances to improve your utilization ratio, and confirm your employment and financial situation remain stable-these actions cost nothing and frequently unlock rate improvements worth thousands.

When you speak with lenders, ask them to explain how your specific credit score, down payment percentage, and property type influence their rate offer compared to their standard pricing. Request a detailed breakdown of all closing costs and points, and ask whether they offer rate locks that extend beyond your expected closing timeline. Inquire about their process for handling appraisals and underwriting delays, since these directly affect whether you close on time or lose your locked rate.

We at Kearns Mortgage Team help you navigate Florida’s mortgage market with personalized guidance across conventional, VA, FHA, USDA, and non-QM loan options tailored to your situation. Visit Kearns Mortgage Team to explore how we can help you achieve your homeownership goals with a trusted partner by your side. What aspect of your financial profile do you think offers the most opportunity to improve your mortgage rate before you apply?