If you’re a veteran considering a VA loan, understanding the requirements for VA loan credit scores is your first step toward homeownership. The good news is that VA loans are more flexible than conventional mortgages when it comes to credit standards.

At Kearns Mortgage Team, we’ve helped countless veterans navigate this process and discover that your credit score is just one piece of the puzzle. Lenders evaluate your full financial picture, not just a number.

What Credit Score Do You Actually Need for a VA Loan?

The Department of Veterans Affairs does not set a universal minimum credit score for VA loans, which means individual lenders determine their own thresholds. In practice, most VA lenders start around 620 as a baseline, but this is far from a hard ceiling. Freedom Mortgage approves borrowers with scores as low as 550 for both purchase and cash-out refinance loans. The 2024 HMDA data shows VA borrowers averaged approximately 725, compared to 755 for conventional borrowers and 692 for FHA borrowers. What matters most is that your score reflects your ability to manage debt responsibly. A lower score does not automatically disqualify you, especially if you have compensating factors like minimal debt, a solid employment history, substantial liquid assets, or a strong record of on-time housing payments in the last 12 months. The VA loan program backs lenders with a guarantee, reducing their risk and allowing them more flexibility than conventional lenders can offer. This is why you can qualify for a VA loan with a credit profile that would be rejected elsewhere.

Beyond the Number: What Lenders Actually Evaluate

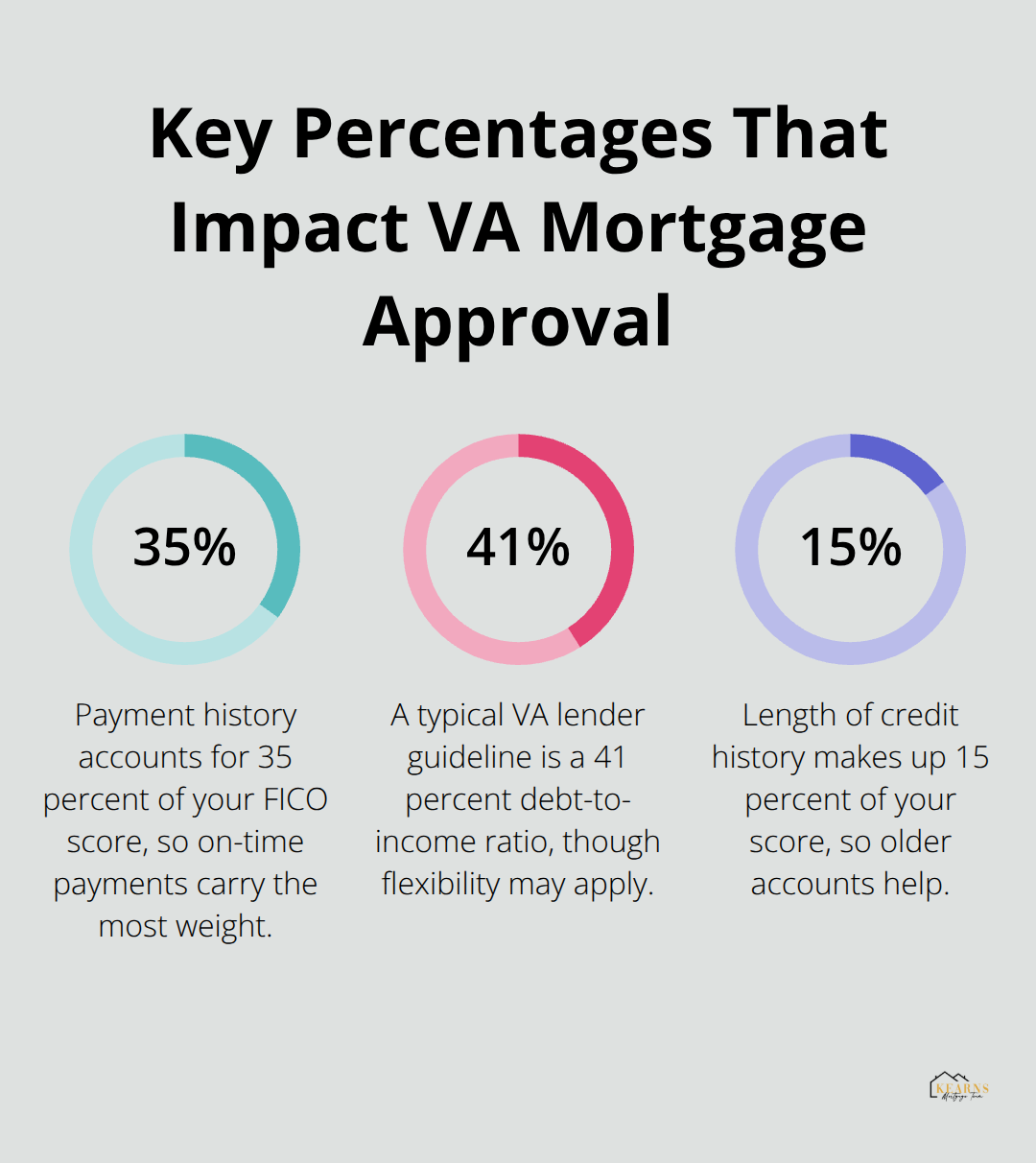

Your credit score tells only part of your financial story. Lenders examine your debt-to-income ratio, which typically needs to stay at 41 percent or lower, though some flexibility exists depending on your overall profile. They scrutinize your payment history over the last year to verify you have paid housing costs, credit cards, and other obligations on time. Employment stability matters significantly; a long tenure with the same employer or a consistent career trajectory reassures lenders you can sustain mortgage payments. Your liquid assets and reserves also factor into the decision, especially if your score falls below 650. Lenders want to see that you have savings to cover several months of mortgage payments if unexpected circumstances arise. If you have experienced bankruptcy, foreclosure, or a short sale, the seasoning period required for VA loans is often shorter than conventional loans, making a fresh start more achievable than you might expect.

How to Check Your Actual Mortgage Score

Pull your free credit reports from AnnualCreditReport.com and compare them across Experian, Equifax, and TransUnion. Mortgage-specific credit scores used by lenders differ from the consumer scores you see online, so requesting your actual mortgage score gives you the clearest picture of where you stand. This step takes minutes but provides clarity that shapes your entire application strategy.

VA Loans Versus Conventional Mortgages: A Real Advantage

Conventional loans typically demand credit scores of 740 or higher to secure the best rates and terms, and borrowers with scores below 680 often face substantial rate increases or outright rejection. Conventional mortgages also require private mortgage insurance if you put down less than 20 percent, adding hundreds of dollars to your monthly payment. VA loans eliminate PMI entirely, replacing it with a one-time funding fee that varies based on your down payment and loan type. The funding fee is added to your loan amount rather than paid upfront, meaning you do not need extra cash at closing. A veteran with a 600 credit score and no down payment can obtain a VA loan with rates far more competitive than a conventional borrower in the same situation. This advantage stems directly from the VA guarantee, which protects lenders and encourages them to approve borrowers they might otherwise decline. If you are considering an IRRRL, the VA streamline refinance program often has even looser requirements, sometimes eliminating the credit check and appraisal altogether depending on your lender.

What Happens Next in Your Application

Your credit score opens the door, but lenders evaluate your complete financial picture to make their final decision. Income stability, employment history, and your debt-to-income ratio all carry significant weight in determining not just approval, but the rate and terms you receive.

How to Improve Your Credit Score for a VA Loan

Review Your Credit Report for Errors and Disputes

Pull your credit reports from AnnualCreditReport.com and review all three bureaus-Experian, Equifax, and TransUnion. Errors happen frequently, and they directly damage your score. Dispute any inaccuracies you find, whether it’s an old account marked as open that you closed years ago, a late payment you made on time, or an account that doesn’t belong to you. The process takes weeks but costs nothing, and correcting even one error can lift your score by 10 to 50 points depending on what’s reported.

Pay Down Existing Debt and Reduce Credit Utilization

Once your reports are clean, focus on the single biggest factor in your credit score: payment history accounts for 35 percent of your FICO calculation. Missing one payment can drop your score by 100 points or more, so set up automatic payments for at least the minimum due on every credit card and loan. If you’ve missed payments in the past, start fresh now. Lenders specifically check your payment record over the last 12 months, so 12 consecutive on-time payments matter far more than perfection five years ago.

Simultaneously tackle your credit utilization ratio. If you’re carrying balances near your credit limits, you’re signaling financial stress to lenders. Try to keep your credit utilization below 30% across all cards combined. If you have a card with a $5,000 limit, keep the balance under $1,500. This single adjustment can boost your score by 20 to 30 points within one or two billing cycles because utilization changes are reported immediately to the bureaus.

Strategic Debt Paydown Before Your Application

The math here is straightforward: lower balances plus on-time payments equals a rising score. If you have three months before you apply for a VA loan, aggressively pay down revolving debt rather than opening new accounts or closing old ones. Closing a card eliminates available credit, which worsens your utilization ratio and can backfire. Length of credit history makes up 15 percent of your score, so older accounts help you even if you rarely use them.

Pay down your highest-balance cards first while maintaining minimum payments on everything else, then watch your score climb. Improving your score before you apply returns real money in tangible savings. Every 20 to 40 points can save you thousands annually in interest costs, so focus on consistent progress rather than perfection.

Avoid New Credit Applications and Hard Inquiries

Hard inquiries from loan applications also sting your score temporarily, so avoid applying for new credit in the months leading up to your VA loan application. Each inquiry drops your score by a few points, and multiple inquiries within a short window signal desperation to lenders. Focus your energy on what moves the needle: paying on time, reducing balances, and correcting errors on your reports.

With your credit profile strengthened, the next step involves understanding what lenders examine beyond your score-the income stability and debt-to-income ratio that determine whether you qualify and what rate you receive.

VA Loan Approval Process and Credit Considerations

What Lenders Actually Verify Beyond Your Credit Score

Your credit score opens the door, but lenders spend far more time evaluating the financial stability behind that number. The first thing they examine is your debt-to-income ratio, which serves as a guide for lenders evaluating your application. This ratio divides your total monthly debt payments by your gross monthly income, and it tells lenders whether you have breathing room in your budget for a mortgage payment. If your DTI sits at 35 percent, adding a $1,500 mortgage payment might push you to 50 percent, which most lenders will reject outright. Calculate your current DTI before you apply by adding up all monthly debt obligations-credit cards, car loans, student loans, personal loans, and existing housing costs-then divide by your gross income. If you’re at 45 percent, you have work to do. Paying down debt before applying matters more than improving your credit score because it directly lowers this ratio.

Employment History and Income Stability

Lenders scrutinize your employment history with intense focus. They want to see at least two years of stable income in the same field or industry, though military service counts as continuous employment even if you’ve changed positions within the military. A job change from one employer to another in the same role carries less risk than a career pivot, so document your work history clearly.

If you’ve been self-employed for less than two years, expect additional documentation requirements including tax returns for the past two years and possibly a profit-and-loss statement. Lenders verify employment directly with your current employer and sometimes contact previous employers, so ensure your dates and titles match across all applications.

Liquid Assets and Housing Payment History

Beyond income, lenders examine your liquid assets and reserves-the cash you have available after closing. This matters especially if your credit score falls below 650 or your DTI edges toward the upper limit. If you have six months of mortgage payments sitting in savings, that reserve cushion signals you can weather financial disruptions. You’ll need to provide bank statements for the past two months showing account balances, and lenders trace the source of down payment funds to ensure they come from legitimate savings rather than borrowed money. Large deposits appearing suddenly in your account will raise questions; prepare explanations for them. If you received a gift from a family member, you’ll need a gift letter stating the funds don’t require repayment.

Lenders also verify your housing payment history by pulling your credit report and sometimes requesting proof of rent payments for the past 12 months, especially if you’re a first-time homebuyer. Consistent on-time housing payments matter more than almost anything else because they prove you prioritize housing costs. A single late mortgage or rent payment in the past year can derail approval, while a perfect 12-month record strengthens your application dramatically.

Documentation and Verification Requirements

Documentation requirements vary by lender but always include recent pay stubs, W-2 forms for the past two years, and a signed authorization allowing the lender to verify employment and pull credit reports. If you have gaps in employment lasting more than 30 days, prepare a written explanation. If you’ve experienced bankruptcy, foreclosure, or a short sale, document the timeline and circumstances. VA loans allow approval after these events, but the seasoning period-typically two to three years for bankruptcy and one to three years for foreclosure-must have passed. Before you get pre approved for a VA loan, gather all documentation rather than scrambling after submission, which delays processing and signals disorganization to underwriters.

Final Thoughts

Your credit score matters, but it’s far from the only factor determining whether you qualify for a VA loan. The requirements for VA loan credit scores are set by individual lenders, not the VA itself, which means flexibility exists at nearly every level. Most lenders start around 620, but some approve borrowers with scores as low as 550, and compensating factors like stable employment, minimal debt, and solid payment history can offset a lower score entirely.

Strengthening your application starts now, regardless of where your credit currently stands. Pull your reports from AnnualCreditReport.com and dispute any errors you find, then focus on the two actions that move the needle fastest: paying every bill on time for the next 12 months and reducing your credit card balances below 30 percent of your limits. If you have three to six months before applying, aggressive debt paydown will lower your debt-to-income ratio and boost your score simultaneously, while avoiding new credit applications protects your score from temporary damage.

When you’re ready to move forward, gather your documentation early and contact Kearns Mortgage Team for a free consultation to review your specific situation. Our team maps out a personalized path to approval with transparent advice and competitive rates, whether your credit needs work or you’re ready to apply immediately. What’s holding you back from taking the first step toward homeownership?