Finding the right mortgage rates in Tampa can feel overwhelming, especially with so many options available. We at Kearns Mortgage Team know that even small differences in rates can save you thousands over the life of your loan.

This guide walks you through current market conditions, proven strategies to lock in better rates, and the loan types that work best for Tampa borrowers. By the end, you’ll have the knowledge to make a confident decision about your mortgage.

What Tampa Mortgage Rates Tell You Right Now

As of early January 2026, Tampa mortgage rates sit around 6.20% for a 30-year fixed mortgage and 5.49% for a 15-year fixed option, according to Bankrate’s current data. These rates reflect a significant drop from the peak near 8% in October 2023, but they remain elevated compared to the historically low rates of 2020 and 2021. The Tampa market follows national trends closely, though local factors like Florida’s insurance crisis add complexity to your overall housing costs. Property insurance in Tampa has become substantially more expensive, which means your actual monthly payment burden extends beyond just the mortgage rate itself. When you evaluate rates, factor in that homeowners insurance, property taxes, and potential HOA fees will add meaningfully to your bottom line. The median home price in Tampa hovers around $403,000, with homes staying on the market approximately 82 days on average as of October 2025. About 9.1% of homes sold above list price during that period, while 29.3% experienced price reductions, indicating a market that favors informed buyers who move strategically.

What Moves Your Personal Rate

Federal Reserve policy and inflation data drive the broader rate environment, but Tampa’s local market also responds to inventory levels and days-on-market conditions. When inventory tightens and homes move faster, lenders adjust rates upward because demand increases. Conversely, when homes linger longer on the market, rates may soften slightly as lenders compete for borrowers. Your personal rate will differ from the published average based on your credit score, down payment size, and debt-to-income ratio. A credit score of 740 or higher typically qualifies you for rates near the published average, while scores below 700 result in rate adjustments of 0.25% to 0.75% or more. A 20% down payment protects you from private mortgage insurance and often unlocks better pricing than a 3% or 5% down payment. Bankrate’s national rate data shows that 30-year fixed mortgages carry APRs around 6.26%, 15-year fixed at 5.59%, FHA loans at 6.24%, and VA loans at 6.45%, giving you concrete benchmarks for comparing lender quotes.

Timing Your Rate Lock

Rate locks typically last 30 to 60 days, and the timing of your lock matters significantly in a volatile market. If rates show an upward trend, you should lock sooner to protect yourself from increases during your closing window. If rates trend downward, waiting carries risk but might reward you with a lower rate. Most lenders allow you to float your rate for a period before you lock it, though this strategy requires active monitoring of market conditions. Buying points-paying upfront fees to reduce your interest rate-makes sense only if you plan to stay in your home long enough to recoup the cost through monthly savings. A break-even analysis comparing your upfront point cost against monthly payment reduction tells you whether buying points aligns with your timeline. You should shop at least three lenders and compare their Loan Estimates side by side, paying close attention to both the interest rate and the APR, which includes closing costs and reflects the true borrowing cost.

With these rate fundamentals in mind, the next step involves understanding which mortgage products actually work best for your situation-and that’s where the variety of loan types available in Tampa becomes your advantage.

Securing the Best Rate Starts Before You Apply

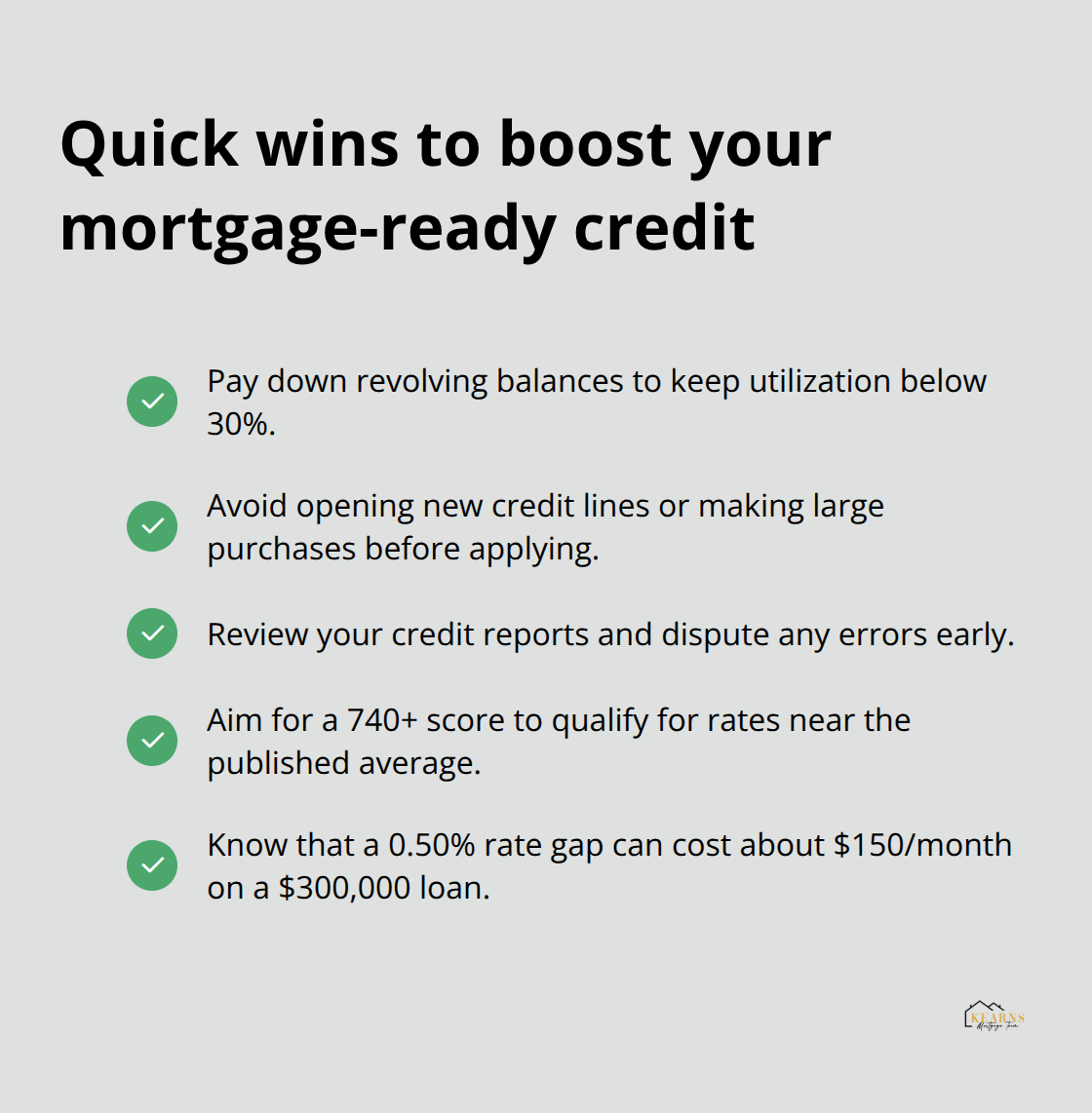

Your credit score determines whether you qualify for a premium rate or pay a penalty rate. If your score sits below 740, you’re leaving money on the table every month for 15 to 30 years. Start improving your score at least three to six months before you apply for a mortgage.

Pay down existing credit card balances to lower your credit utilization ratio below 30%, as this shift alone can boost your score by 50 to 100 points. Avoid opening new credit accounts or making large purchases on credit during this window, since hard inquiries and new accounts temporarily lower your score. Check your credit report for errors through annualcreditreport.com, the only official free source, and dispute any inaccuracies immediately. Bankrate’s rate data confirms that borrowers with scores of 740 or higher qualify for rates near the published average, while those below 700 face adjustments of 0.25% to 0.75% or more. On a $300,000 loan, a 0.50% rate difference costs roughly $150 more per month, or $54,000 over 30 years.

Compare at Least Three Lenders with Real Numbers

Shopping a single lender leaves you completely blind to your options. Contact at least three different lenders and request a formal Loan Estimate within three days of application, which federal law requires them to provide. Compare the interest rate, APR, closing costs, and origination fees side by side, since APR reveals the true cost including fees that the note rate alone hides. Lenders often quote slightly different rates based on their pricing models and wholesale costs, so the difference between lender A and lender B can be 0.125% to 0.375% on the same loan profile. That spread translates to $37 to $112 monthly on a $300,000 mortgage. Request quotes for the same loan structure-same down payment, same term, same loan type-so you’re truly comparing apples to apples. Online lenders, traditional banks, and mortgage brokers each have different cost structures, so including at least one from each category in your comparison makes sense. Read customer reviews on independent sites like Zillow or Google Reviews to assess how lenders handle the closing process and whether they meet promised timelines, since a lender who closes late can cost you your rate lock or delay your move-in date.

Lock Your Rate When Conditions Favor You

Rate locks run 30 to 60 days, and the market environment during your lock period determines whether you made the right timing decision. If the Federal Reserve signals rate hikes or inflation data comes in hot, rates typically rise, and your lock protects you from those increases. If economic data weakens and the Fed hints at cuts, rates may fall, but your lock prevents you from benefiting. Watch the weekly Freddie Mac Primary Mortgage Market Survey to understand the rate trajectory over the past month, then make your lock decision based on whether rates show upward or downward momentum. Locking early in a rising-rate environment costs you nothing but peace of mind, while floating in a falling-rate environment risks missing a better rate. Most lenders allow you to float for 10 to 20 days before locking, which gives you time to monitor conditions without committing. Buying points-paying an upfront fee to reduce your rate by 0.25% to 0.375%-only makes sense if you’ll stay in the home long enough to recoup the cost through monthly savings. A break-even calculator shows that buying one point typically breaks even after 7 to 10 years, so if you plan to sell or refinance sooner, skip the points and keep your cash.

Understand Your Personal Rate Adjustment

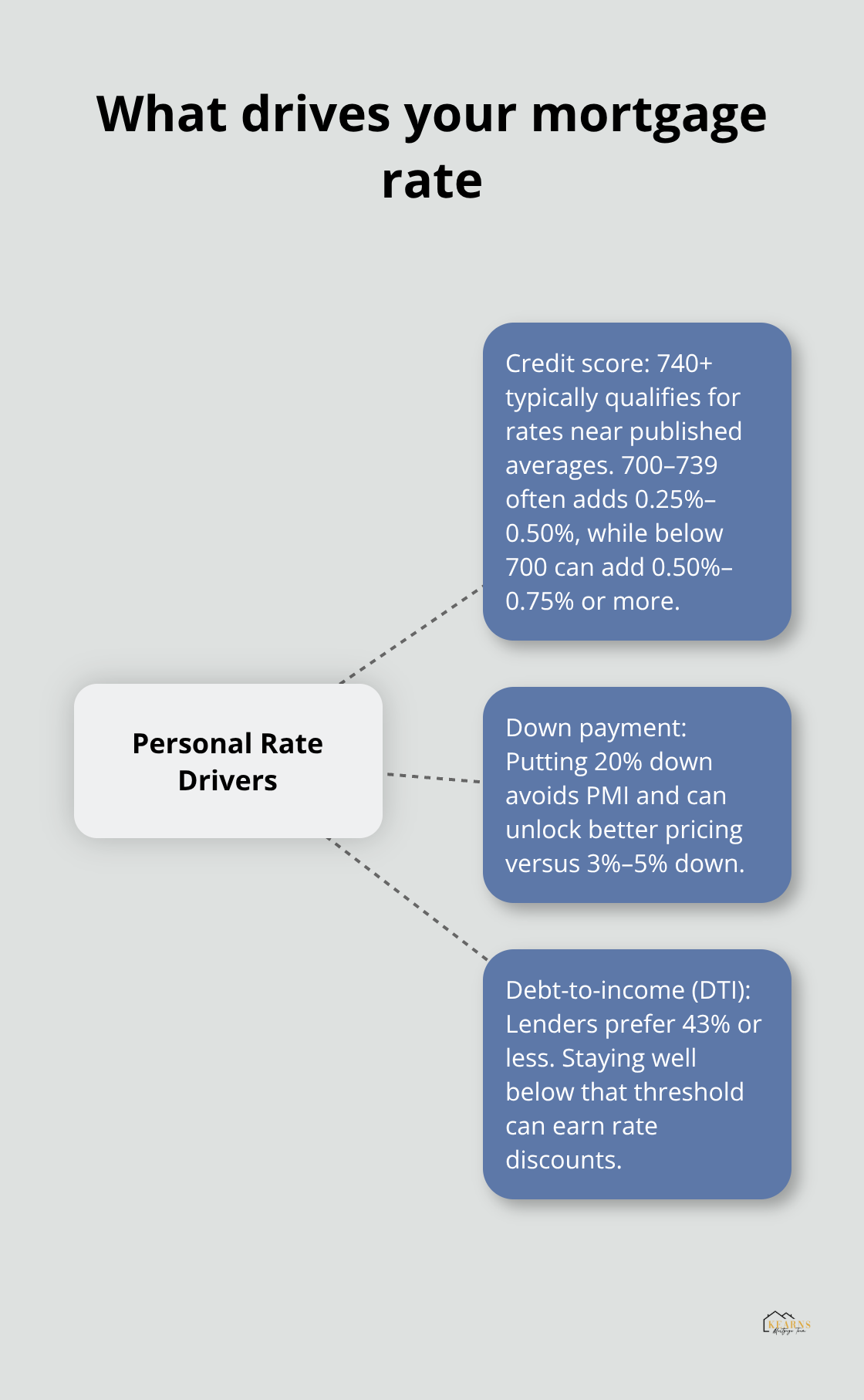

Your actual rate differs from published averages based on three primary factors: your credit score, your down payment size, and your debt-to-income ratio. A credit score of 740 or higher typically qualifies you for rates near the published average, while scores between 700 and 739 trigger adjustments of 0.25% to 0.50%. Scores below 700 face steeper penalties (0.50% to 0.75% or more), which compound over the life of your loan.

A 20% down payment protects you from private mortgage insurance and often unlocks better pricing than a 3% or 5% down payment. Your debt-to-income ratio helps lenders determine if you can afford to take on additional debt, such as a mortgage loan. Lenders prefer a DTI of 43% or less for conventional mortgages, and borrowers who stay well below this threshold often receive rate discounts. Understanding these three levers helps you identify which improvements will have the biggest impact on your final rate.

Now that you understand how to position yourself for the best available rates, the next step involves knowing which mortgage products actually work best for your specific situation-and that’s where the variety of loan types available in Tampa becomes your advantage.

Which Loan Type Works Best for Your Tampa Situation

Conventional mortgages dominate Tampa’s market, and for good reason: they typically offer the lowest rates when you have a credit score of 740 or higher, a debt-to-income ratio below 43%, and a down payment of at least 20%. Bankrate’s current data shows conventional 30-year fixed mortgages at 6.20% with an APR of 6.26%, making them the baseline against which all other products compete. If your credit score falls below 620, conventional loans shut the door entirely, which is where FHA loans become your lifeline.

FHA, VA, and USDA Loans Open Doors for Different Borrowers

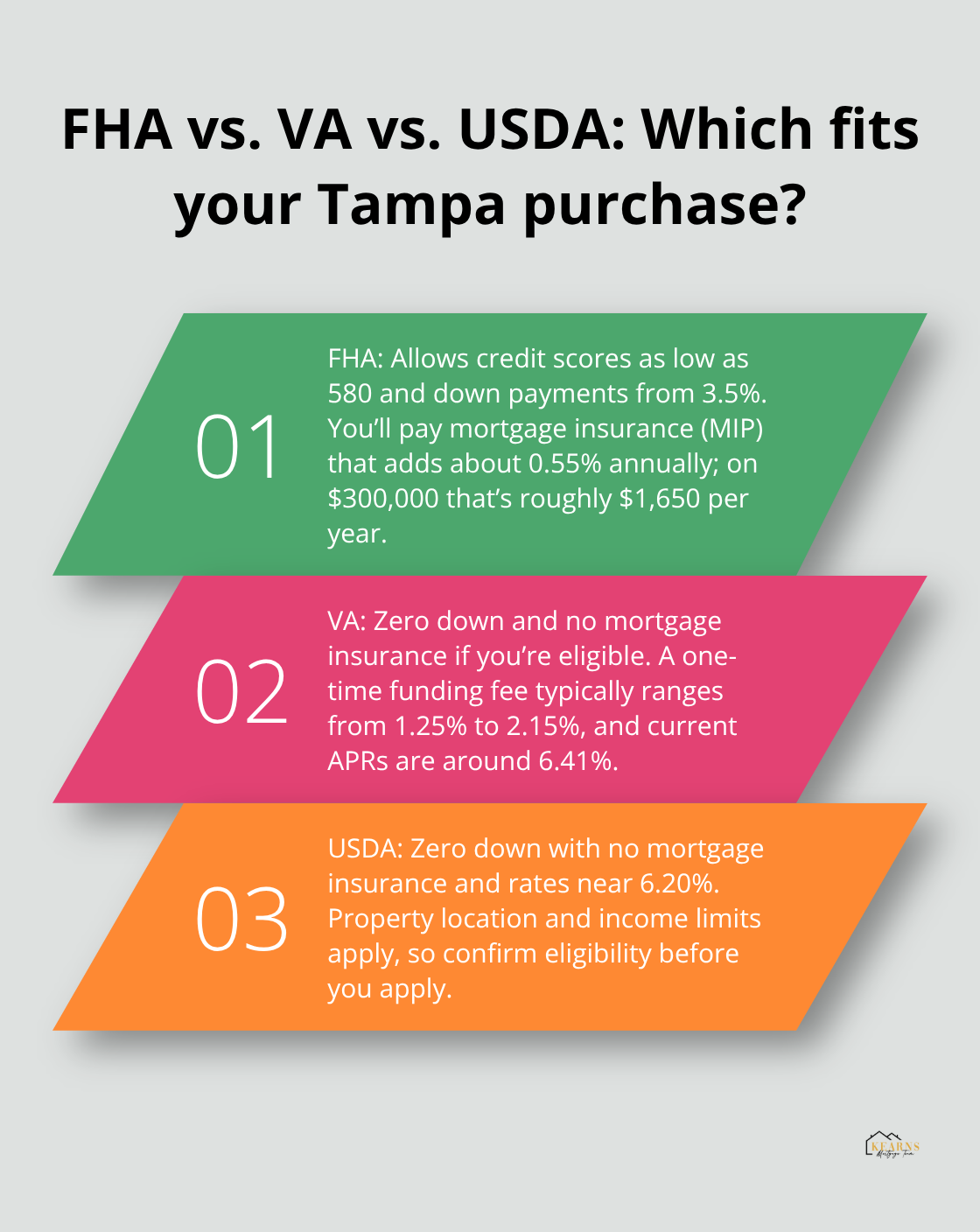

FHA loans accept credit scores as low as 580 and down payments as low as 3.5%, though this flexibility comes with a tradeoff: you’ll pay mortgage insurance premiums (MIP) that add roughly 0.55% to your effective rate annually. On a $300,000 loan, that MIP costs around $1,650 per year, or about $137 monthly. VA loans eliminate this insurance burden entirely if you’re a veteran or active-duty service member, and they require zero down payment, though you’ll pay a funding fee ranging from 1.25% to 2.15% on your first use. Bankrate shows VA loans currently at 6.41% APR, only 0.15% higher than conventional mortgages despite the zero down payment advantage.

USDA loans remain underutilized in Tampa despite serving rural and suburban borrowers with comparable benefits to VA loans: zero down payment, no mortgage insurance, and rates around 6.20%. The catch is that USDA loans have strict property location requirements and income limits, so confirm your address qualifies before pursuing this path. Non-QM loans exist for self-employed borrowers, investors, and those with recent credit events who don’t fit the conventional mold, though rates typically run 0.50% to 1.25% higher than conventional options because lenders accept greater risk.

Shopping Across Product Types Reveals Real Savings

A 0.5% rate difference on a $300,000 mortgage costs $150 monthly or $54,000 over 30 years, yet many borrowers never compare beyond one lender’s offerings. Contact multiple lenders and request quotes for each loan type that matches your situation. This comparison reveals which product type actually delivers the best rate for your specific credit profile and down payment amount. Sometimes an FHA loan with a lower rate beats a conventional loan with a higher rate, even after you factor in mortgage insurance costs. Other times, a VA loan’s zero down payment advantage outweighs a slightly higher interest rate. The only way to know is to shop and compare.

Adjustable-Rate Mortgages Offer Savings with Built-In Risk

A 7/1 ARM has a fixed interest rate for the first seven years, then adjusts to a variable rate. This savings totals $7,980 if you sell or refinance before the rate adjusts, making ARMs sensible for buyers who plan to move within five to seven years. However, if you stay beyond year seven, your rate adjusts annually to current market conditions, potentially jumping 1% to 3% when rates spike.

A 7/1 ARM could reset to higher rates in a rising-rate environment, destroying your budget if you haven’t prepared for the increase. The safest ARM strategy involves calculating your worst-case scenario payment (typically capped at a maximum rate increase per year and a lifetime ceiling) and confirming you can afford it even if rates hit their ceiling.

Fixed-Rate Mortgages Eliminate Rate Uncertainty

Fixed-rate mortgages eliminate this uncertainty entirely: your 6.20% rate on a 30-year fixed stays locked for the full 360 payments, which means your mortgage payment never changes regardless of what happens in the broader economy. This predictability matters most if you plan to stay in your home for more than seven years, have a tight monthly budget with little cushion for payment increases, or believe rates will rise significantly over your loan term. Your payment remains stable while inflation erodes the real value of that payment over time, which works in your favor on a long-term fixed mortgage.

Final Thoughts

Finding the best mortgage rates in Tampa requires three concrete actions: improve your credit score before you apply, compare quotes from at least three lenders, and lock your rate when market conditions support your timeline. Your credit score drives your rate more than any other factor you control, so spending three to six months boosting it from 700 to 740 pays dividends for decades. Shopping multiple lenders reveals rate differences of 0.125% to 0.375%, which translates to thousands in savings or costs over your loan term.

Before you commit to any lender, ask them to explain your personal rate adjustment and which factors pushed your rate above or below the published average. Request a detailed breakdown of all closing costs, confirm whether any fees are negotiable, and verify that your lender can close within your timeline. Confirm whether you qualify for any down payment assistance programs, particularly if you’re a first-time buyer in Tampa, since programs like the City of Tampa’s Dare to Own the Dream initiative can reduce your upfront costs significantly.

We at Kearns Mortgage Team help Tampa borrowers navigate mortgage rates and find the right loan product for their situation. Our team offers free consultations to review your specific circumstances, compare loan options, and identify which product type delivers your best rate. Contact us today so you can move forward with confidence about the mortgage rates Tampa lenders offer you.