Choosing between an FHA vs conventional mortgage shapes your entire home buying experience. The decision affects your down payment, monthly costs, and long-term financial strategy.

We at Kearns Mortgage Team see buyers struggle with this choice daily. Understanding the key differences helps you make the right decision for your financial situation.

What Makes These Mortgages Different

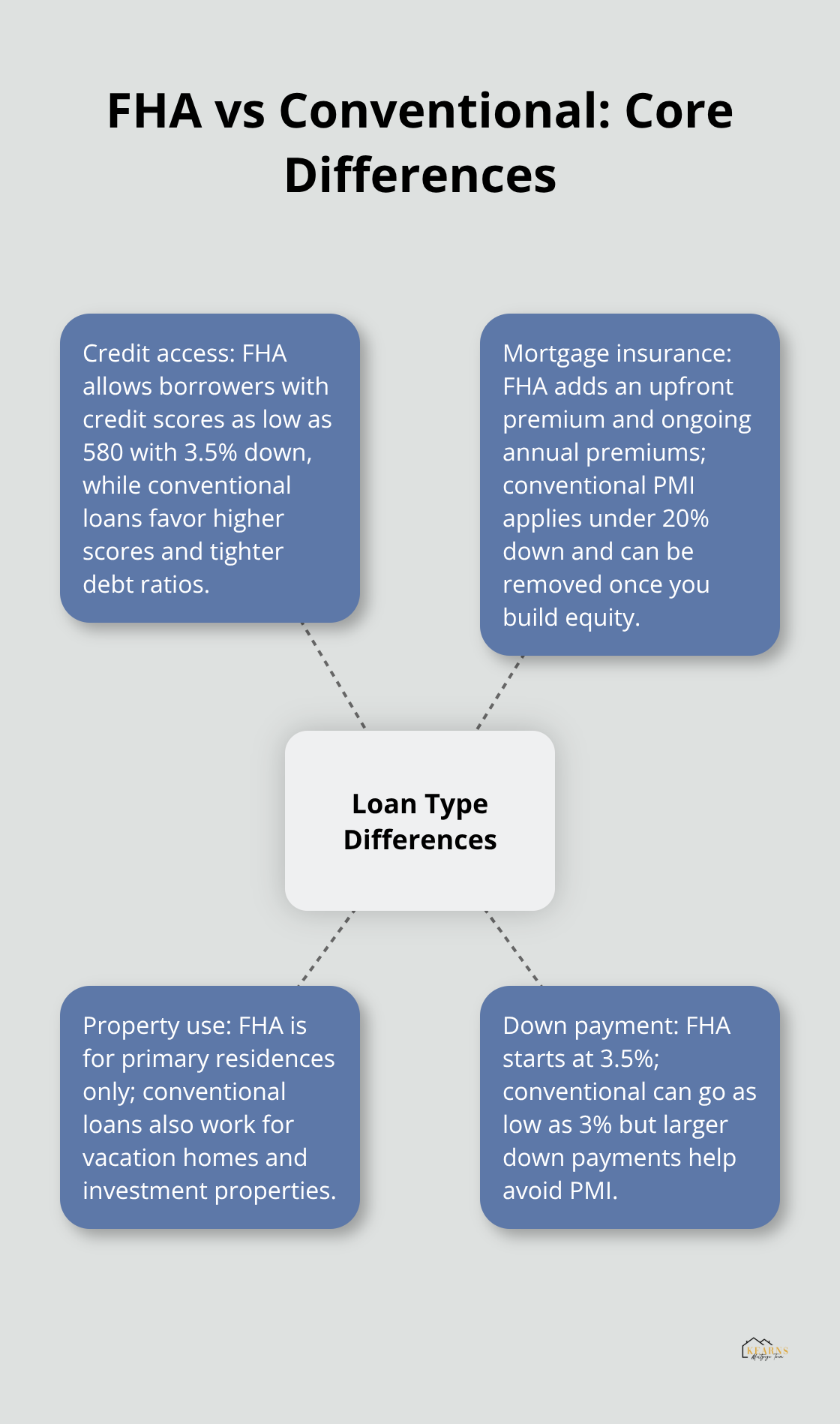

FHA mortgages receive government backing from the Federal Housing Administration, which transforms how lenders evaluate risk. This backing allows lenders to approve borrowers with credit scores as low as 580 for a 3.5% down payment, and even borrowers with scores between 500-579 can qualify with 10% down. The government insurance protects lenders if borrowers default, which makes them willing to work with riskier financial profiles.

Government Protection vs Private Risk

Conventional mortgages operate without government backing, which puts all risk on private lenders and investors like Fannie Mae and Freddie Mac. This fundamental difference drives stricter requirements – conventional loans typically demand higher credit scores and more conservative debt-to-income ratios around 36%. However, as of November 5, 2025, both Fannie Mae and Freddie Mac removed minimum credit score requirements and now evaluate overall credit risk instead of rigid score cutoffs.

Real Money Impact

The backing difference creates measurable cost variations. FHA loans require an upfront mortgage insurance premium of 1.75% of the loan amount plus annual premiums that average 0.55% of the outstanding balance. Conventional loans only require private mortgage insurance when down payments fall below 20%, but this PMI can be canceled once you reach 20% equity. FHA mortgage insurance often lasts for the loan’s entire life if your down payment is less than 10% (making conventional loans cheaper for borrowers with higher credit scores above 720).

Property and Usage Rules

FHA loans demand stricter property inspections that focus on safety and structural soundness, while conventional appraisals concentrate on market value. FHA loans must be used for primary residences only, whereas conventional loans work for vacation homes and investment properties. These restrictions make conventional loans more flexible for diverse real estate strategies.

Down Payment Flexibility

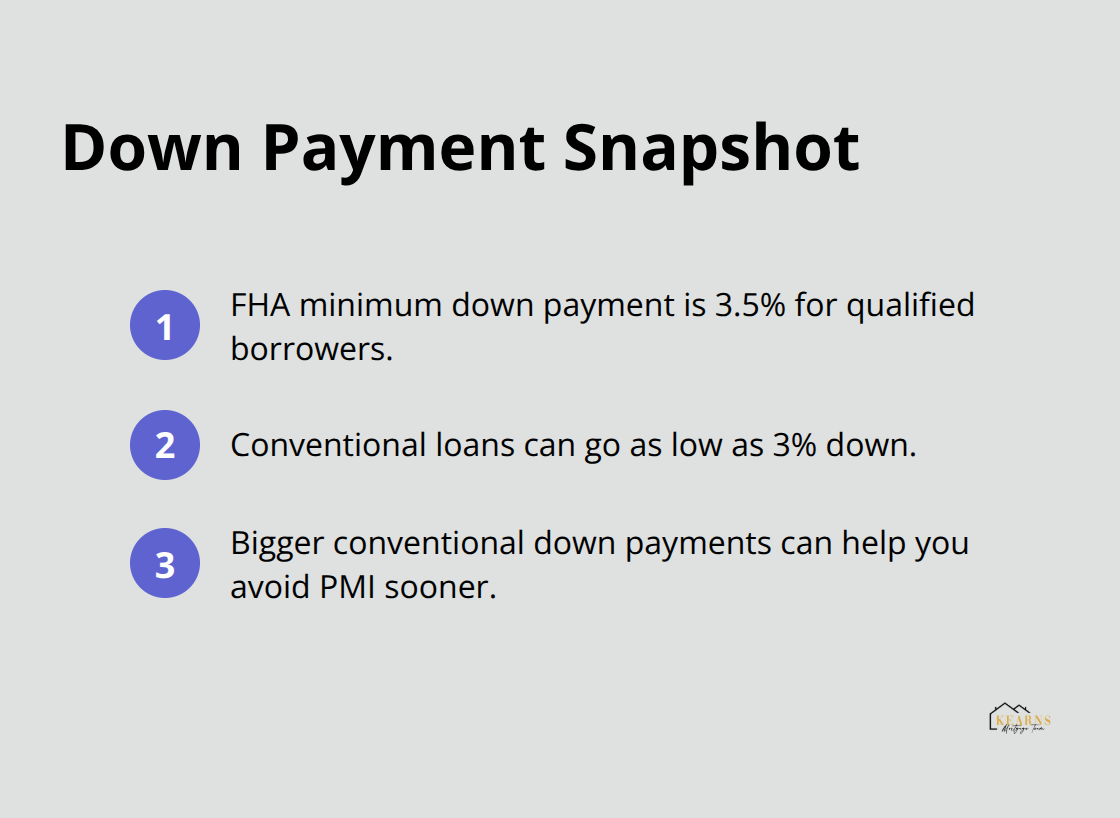

The down payment requirements reveal another key difference between these loan types. FHA loans start at just 3.5% down for qualified borrowers, while conventional loans can go as low as 3% but often require higher payments to avoid PMI (private mortgage insurance). This difference significantly impacts how much cash you need upfront and affects your monthly payment structure.

What Credit Score Do You Actually Need?

FHA Opens Doors for Lower Credit Scores

FHA loans accept credit scores starting at 580 for the minimum 3.5% down payment, which makes homeownership accessible for borrowers who conventional lenders would reject. Borrowers with scores between 500-579 can still qualify with a 10% down payment, though this higher requirement reduces the FHA advantage. These flexible credit standards help first-time buyers and those who recover from financial setbacks enter the housing market years earlier than if they wait for credit repair.

Conventional Loans Reward Higher Scores

Conventional loans typically require credit scores of 620 or higher, though some lenders accept scores as low as 580 with factors like larger down payments or lower debt ratios. Borrowers with scores above 740 receive the best conventional loan terms, which often makes these loans cheaper than FHA options despite higher entry requirements. The recent elimination of rigid credit score minimums by Fannie Mae and Freddie Mac means lenders now evaluate overall credit risk rather than rely solely on score cutoffs.

Debt Ratios Tell the Real Story

FHA loans allow debt-to-income ratios up to 43%, while conventional loans prefer ratios below 43% (though some lenders accept up to 45% with strong credit profiles). This difference matters significantly – a borrower who earns $5,000 monthly can carry $2,150 in total debt payments with FHA compared to $2,150 with conventional loans. FHA also permits gift funds from family members and down payment assistance programs, while conventional loans have stricter gift money requirements that limit sources.

Income Verification Standards

Both loan types require proof of stable income, but FHA loans show more flexibility with employment gaps and alternative income sources. Conventional loans demand consistent employment history (typically two years) and prefer traditional W-2 income documentation. Self-employed borrowers face stricter scrutiny with conventional loans, while FHA programs accommodate varied income patterns more readily.

The differences in credit and income requirements directly impact your monthly costs through mortgage insurance premiums and interest rates.

How Much Will Mortgage Insurance Actually Cost?

FHA Insurance Creates Permanent Payments

FHA mortgage insurance hits you with two separate charges – an upfront premium of 1.75% of your loan amount plus annual premiums that average 0.55% of your outstanding balance. On a $300,000 loan, you pay $5,250 upfront and roughly $1,650 each year. The annual premium ranges from 0.15% to 0.75% based on your loan-to-value ratio and loan term, with most borrowers who pay toward the higher end.

If you put down less than 10%, this insurance remains for the entire loan life. Even with 10% or more down, you must keep the insurance for 11 years minimum. This creates a permanent monthly burden that conventional loans avoid once you build equity.

Conventional PMI Offers an Exit Strategy

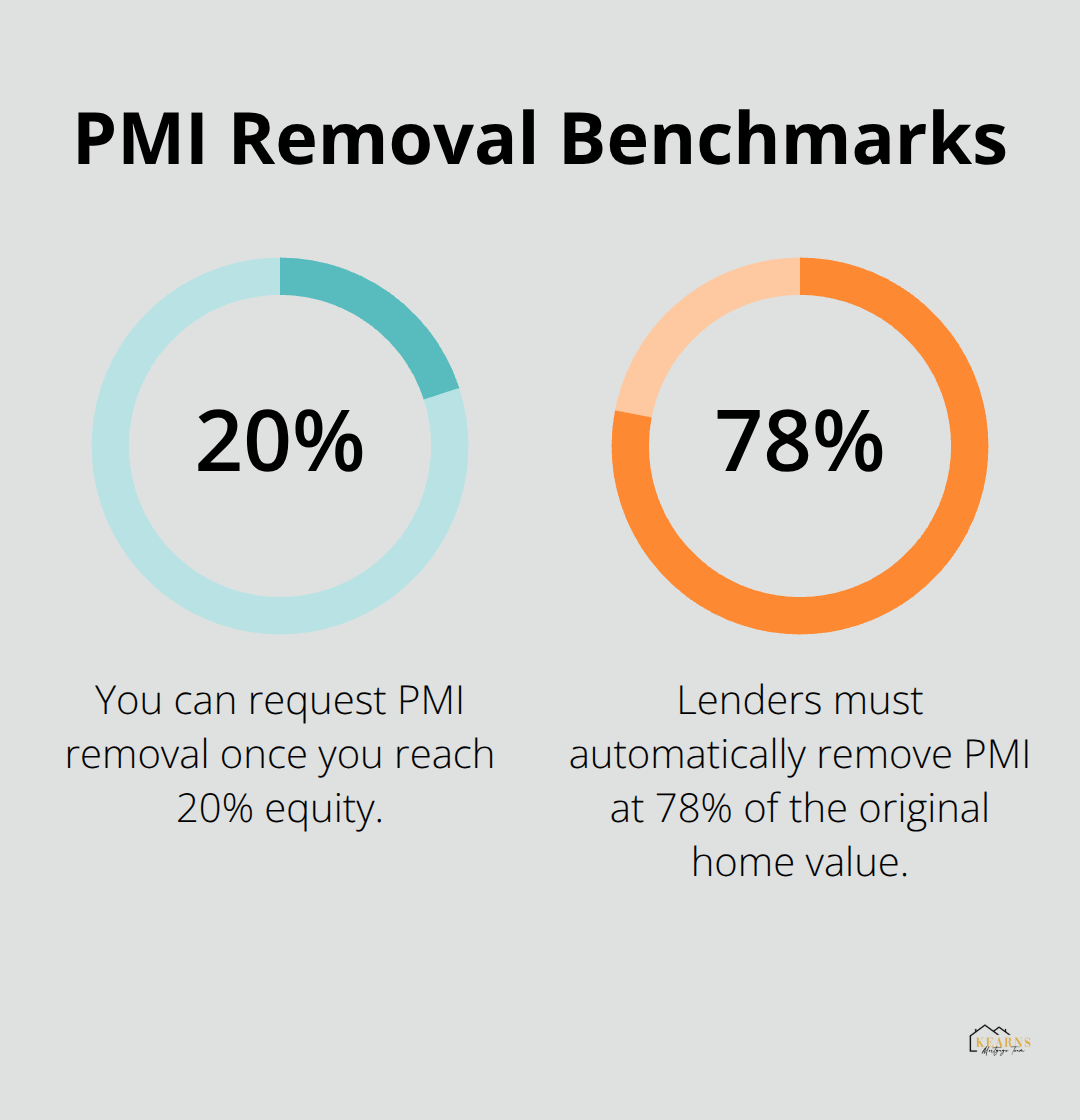

Conventional loans require private mortgage insurance only when your down payment falls below 20%, and you have the right to remove PMI once you have paid down your mortgage to a specified point. PMI costs typically range from 0.3% to 1.5% of your loan amount annually, with most qualified borrowers who pay 0.50% to 1.00%.

On that same $300,000 loan with 10% down, expect PMI around $1,500 annually. The key advantage – you can request PMI removal once you hit 20% equity through payments or home value appreciation. Some borrowers eliminate PMI within five to seven years through aggressive payments or market gains.

The Math Shows Clear Differences

Lenders must automatically remove conventional PMI when your balance drops to 78% of the original home value. This gives you a clear exit strategy that FHA loans lack. FHA borrowers remain stuck with insurance payments indefinitely (unless they refinance to a conventional loan once they build sufficient equity).

The total cost difference compounds over time. A borrower with good credit who keeps an FHA loan for 30 years pays mortgage insurance for the entire term, while a conventional borrower typically eliminates PMI within 8-12 years through normal payments alone.

Final Thoughts

Your financial profile determines which loan type serves you best in the FHA vs conventional mortgage decision. Borrowers with credit scores below 620 and limited savings benefit most from FHA loans despite the permanent mortgage insurance costs. The 3.5% down payment requirement and flexible debt ratios make homeownership possible years earlier than waiting for credit improvement.

Conventional loans reward borrowers with higher credit scores and larger down payments through lower long-term costs. If you have a 720+ credit score and can put down 10-20%, conventional loans typically cost less over time because you can eliminate PMI once you build equity. Consider your timeline and financial goals carefully when you weigh immediate accessibility against long-term costs.

We at Kearns Mortgage Team help you evaluate both options through personalized mortgage solutions that match your specific financial situation. Getting pre-approved with the right loan type starts with understanding which requirements you can meet today versus which benefits matter most for your future. What matters more to you right now – getting into a home quickly with flexible requirements or minimizing your long-term mortgage costs?