Homeowners often wonder how often they should refinance their mortgage to maximize savings. The answer depends on market conditions, personal finances, and your long-term housing plans.

We at Kearns Mortgage Team see clients miss opportunities by waiting too long or refinancing too frequently. Understanding the right timing can save thousands over your loan’s lifetime.

What factors should guide your refinancing decisions?

When Refinancing Makes Financial Sense

Interest Rate Drops of 0.75% or More

Refinancing becomes financially worthwhile when interest rates drop at least 0.75% below your current rate. This threshold accounts for closing costs and processing time while it generates meaningful monthly savings. According to Bankrate’s recent data, refinancing costs average 2% to 5% of your loan amount, meaning a $300,000 mortgage could cost $6,000 to $15,000 in fees.

Break-Even Point Analysis

Your break-even point determines whether refinancing pays off. Divide total closing costs by monthly payment reduction to find how many months you need to recoup expenses. For example, if refinancing saves $200 monthly with $8,000 in costs, you break even after 40 months. Freddie Mac reports that homeowners who stay in their homes beyond this timeline see substantial long-term savings.

Current Market Conditions and Trends

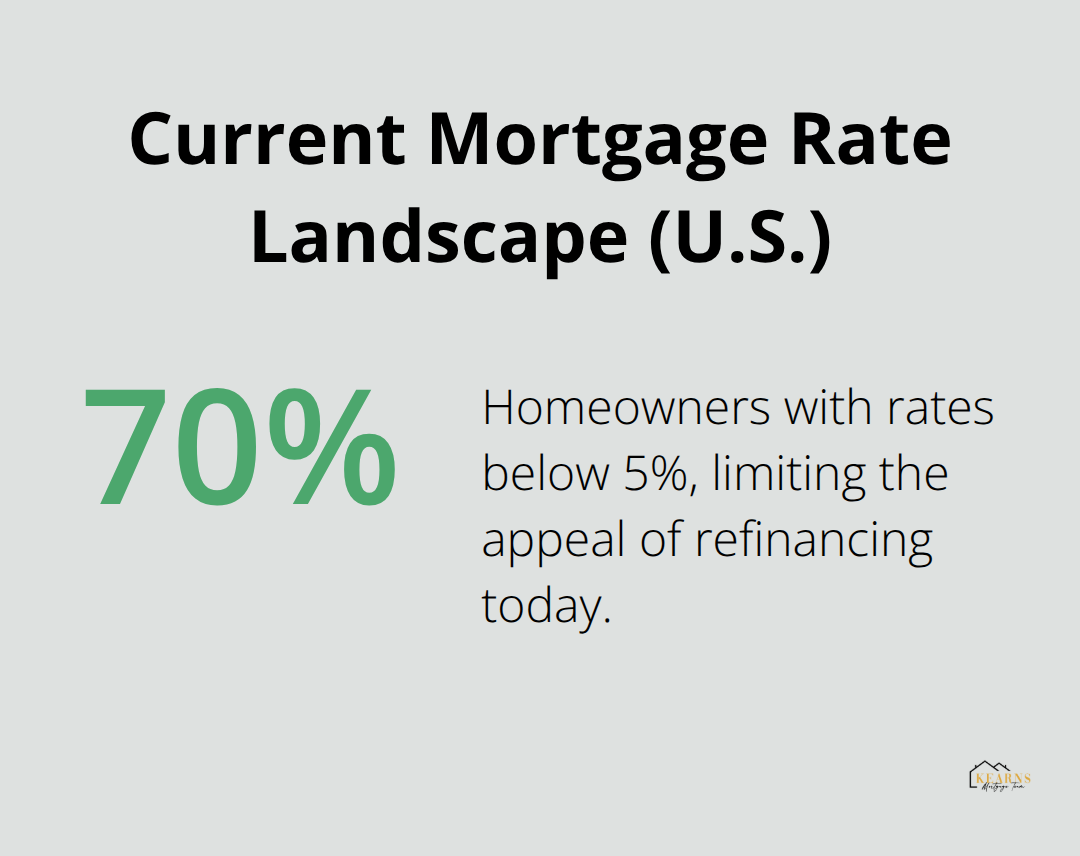

Current market conditions show 30-year fixed rates at 6.74% as of December 2025, which makes refinancing attractive only for borrowers with rates above 7.5%. Economic forecasts suggest rates will remain above 6% through 2025, which creates limited windows for beneficial refinancing. ICE Mortgage Technology data reveals 70% of homeowners hold rates below 5% (making current refinancing less appealing for most borrowers).

However, credit score improvements of 50 points or more can unlock better rates regardless of market conditions. Monitor Federal Reserve announcements and shop three lenders within the same day for accurate rate comparisons, as mortgage rates fluctuate daily based on economic indicators and bond market movements.

These market realities shape when and how often you should consider refinancing, but personal circumstances also play a major role in your decision.

Common Refinancing Scenarios and Timing

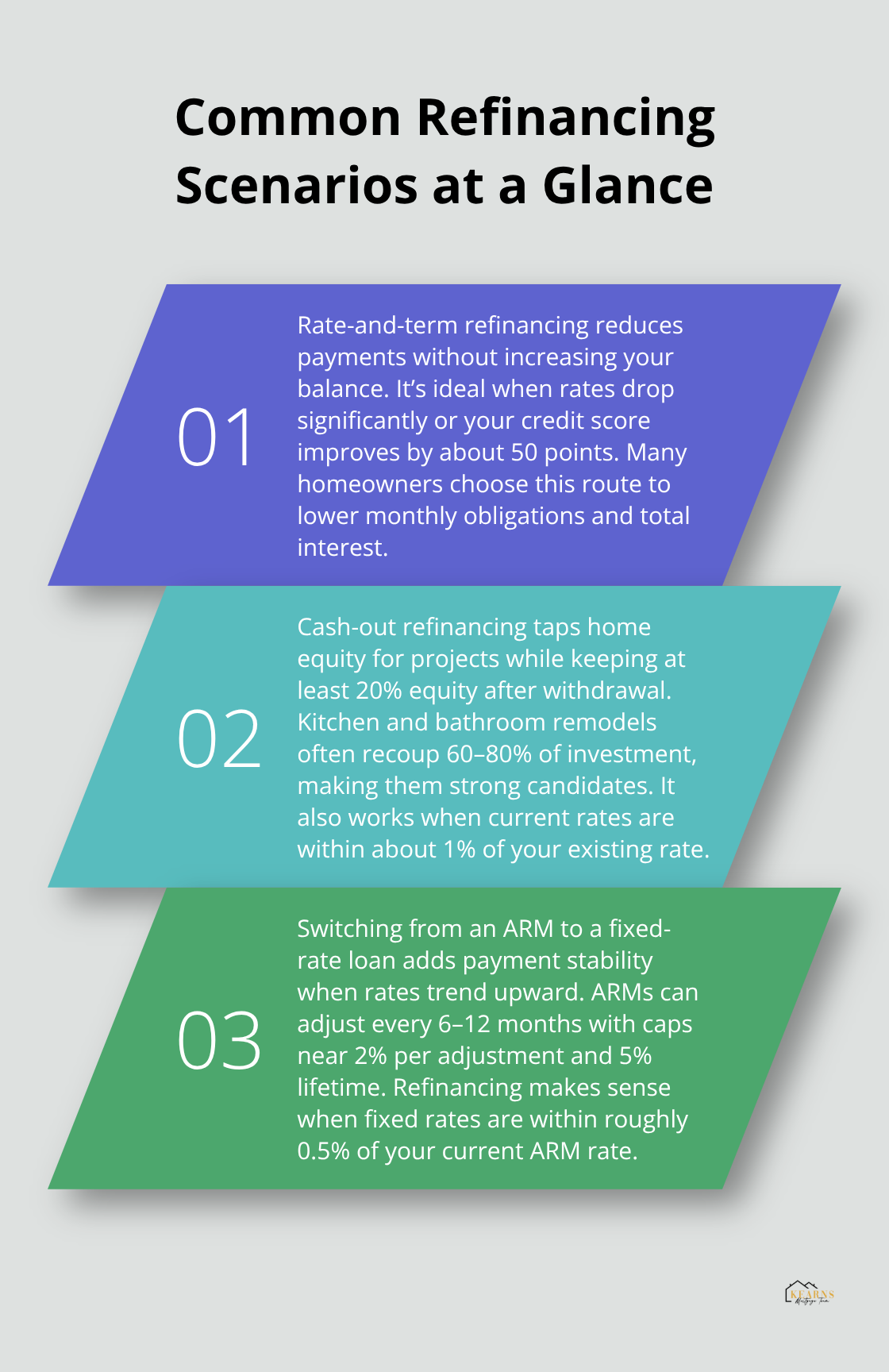

Rate-and-Term Refinancing Opportunities

Rate-and-term refinancing works best when you want lower payments without changing your loan balance. This option makes sense when rates drop significantly or your credit score improves by 50 points or more since your original mortgage. Fannie Mae data shows 60% of homeowners choose this path to reduce monthly obligations.

The key factor involves your remaining loan term. Refinancing a 30-year mortgage after 10 years into another 30-year loan resets your payment schedule and extends your debt timeline. Consider a 15-year refinance instead if you can handle higher monthly payments, as this saves substantial interest over time.

Cash-Out Refinancing for Home Improvements

Cash-out refinancing allows you to tap home equity for renovations that boost property value. This strategy works when you have at least 20% equity remaining after the cash withdrawal and current rates stay within 1% of your existing rate.

Kitchen and bathroom remodels typically return 60-80% of investment (according to Remodeling Magazine’s Cost vs. Value report), which makes them smart cash-out targets. Home equity loans can be a viable choice for debt consolidation when you own much of your property outright, though this converts unsecured debt into secured debt against your home.

Switching from Adjustable to Fixed-Rate Mortgages

ARM borrowers should consider switching to fixed rates when rates trend upward. After the initial period, ARMs typically adjust every six months or once per year based on a specific market index, with rate caps that limit increases to 2% per adjustment and 5% lifetime.

If your ARM rate approaches these caps or market conditions suggest rising rates, refinancing to a fixed-rate mortgage provides payment stability. This move makes particular sense when fixed rates remain close to your current ARM rate (typically within 0.5%).

These scenarios highlight when refinancing makes strategic sense, but several other factors determine how often you should actually refinance your mortgage.

Factors That Affect Refinancing Frequency

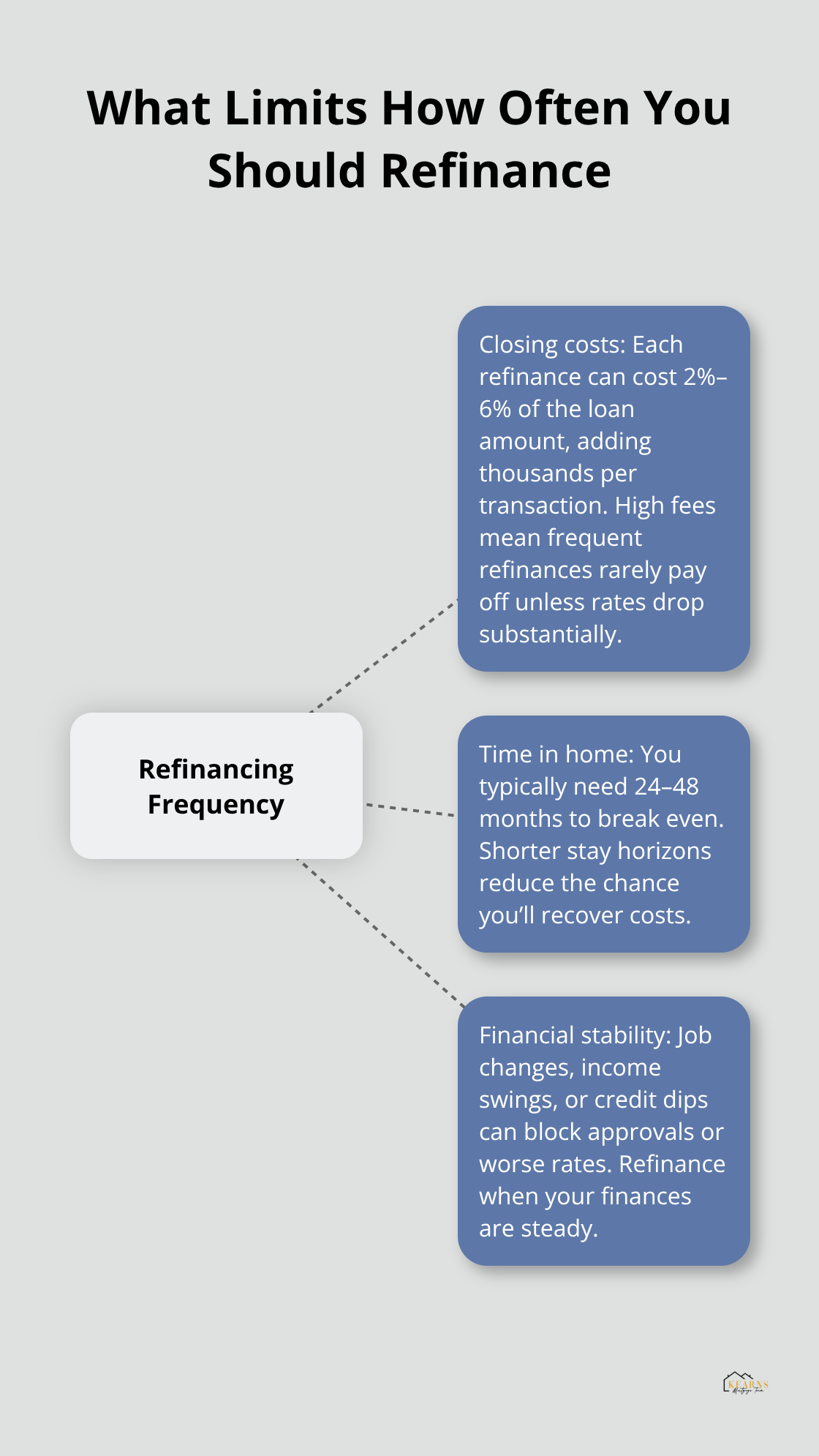

Closing Costs Create Natural Refinancing Limits

Closing costs directly control how frequently refinancing makes financial sense. With costs that average 2% to 6% of your loan amount, a $400,000 mortgage generates $8,000 to $24,000 in fees each time you refinance. This reality means refinancing more than once every three to five years rarely pays off unless rates drop dramatically.

Lenders charge application fees of $500, origination fees between $300 to $500, and appraisal costs around $300 to $500 per transaction. These fixed expenses accumulate quickly with frequent refinancing attempts and create natural barriers to excessive refinancing.

Your Timeline in the Home Matters Most

Plans to stay in your home for less than five years make refinancing questionable regardless of rate improvements. Most homeowners need 24 to 48 months to recover closing costs through monthly payment reductions, but this timeline extends when you refinance frequently.

Credit score improvements of 50 points or higher can justify refinancing sooner than market rate changes alone. Income increases that improve your debt-to-income ratio can also create refinancing opportunities outside normal rate cycles.

Financial Stability Beats Frequent Changes

Refinancing works best when your financial situation remains stable for extended periods. Job changes, income fluctuations, or credit score drops can disqualify you from better rates even when market conditions improve.

The National Association of Realtors reports nearly half of refinancing homeowners extend their loan terms, which resets their payoff timeline and increases total interest paid over the loan’s life (often adding years to debt repayment). Focus on refinancing once when conditions align rather than chasing every small rate improvement that appears in the market.

Final Thoughts

Smart refinance decisions require three key indicators: rate drops of 0.75% or more below your current rate, break-even periods under 48 months, and plans to stay in your home beyond the recovery timeline. Credit score improvements of 50 points create opportunities even when market rates remain flat. The question “how often should I refinance my mortgage” becomes clearer when you focus on substantial financial benefits rather than chase every small rate change.

Most homeowners benefit from refinance opportunities once every five to seven years when conditions align perfectly. Frequent refinance attempts rarely pay off due to closing costs that average 2% to 6% of your loan amount (making multiple refinances expensive within short timeframes). Long-term financial health requires balance between immediate savings and total interest costs over your loan’s lifetime.

We at Kearns Mortgage Team provide personalized guidance to evaluate your specific situation and determine optimal refinance windows based on your financial goals. Consider your complete financial picture, including retirement plans and other debt obligations, before you make refinance decisions that reset your mortgage timeline. What refinance opportunity might you overlook in your current financial situation?