The myth that you need substantial capital to start investing in real estate stops many people from building wealth. The truth is that investing with little money is entirely possible when you know the right strategies.

At Kearns Mortgage Team, we’ve helped countless borrowers discover pathways into real estate that fit their current financial situation. This guide walks you through practical tactics that work for budget-conscious investors.

Three Proven Pathways to Start Investing Today

House Hacking: Live in One Unit, Rent the Others

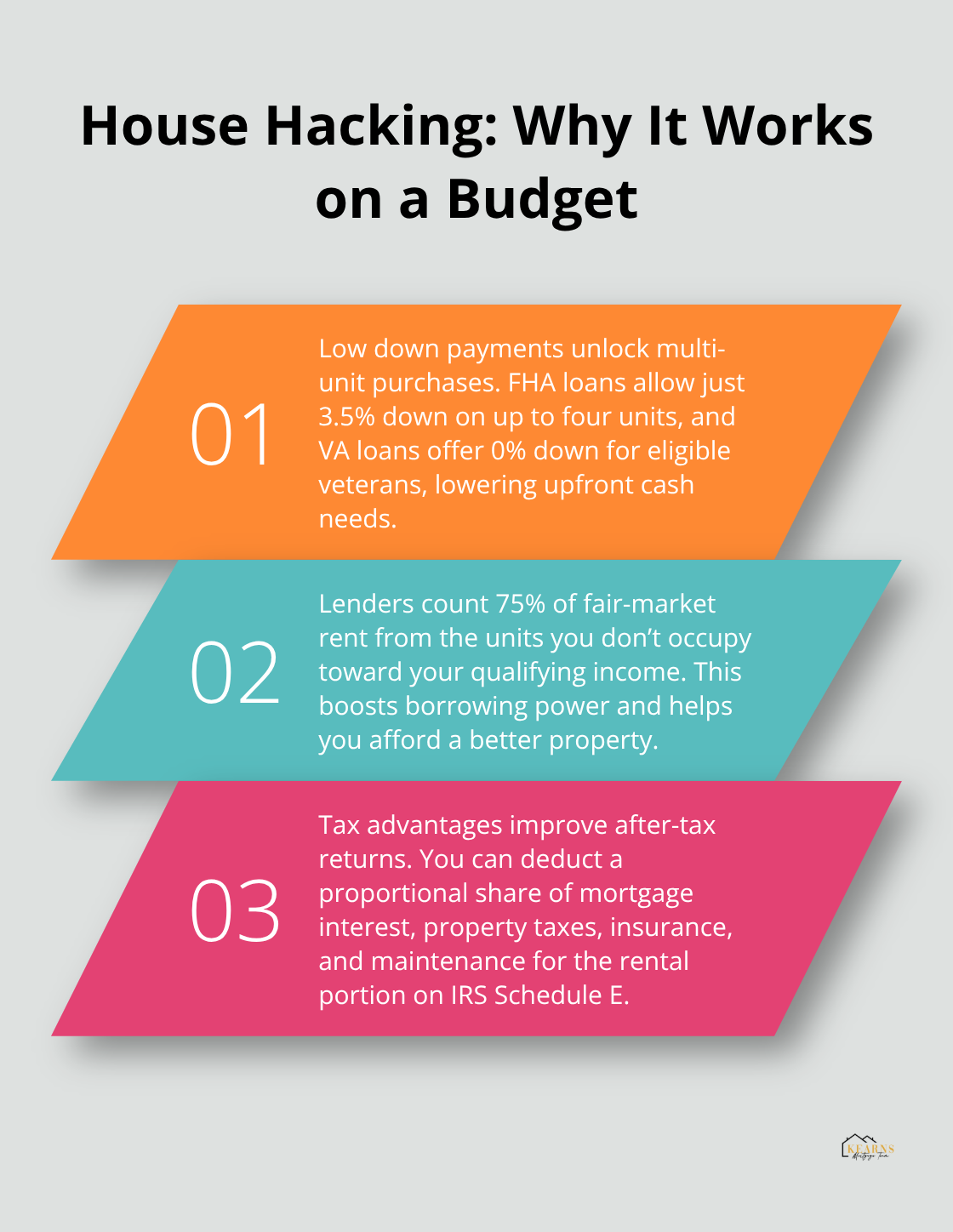

House hacking stands out as the most practical entry point for investors with limited capital. The strategy is straightforward: you buy a multi-unit property with an owner-occupied loan, live in one unit, and rent the others to cover your mortgage. FHA loans allow you to put down just 3.5% on properties with up to four units, while VA loans offer 0% down for eligible veterans. When lenders calculate your qualifying income, they count 75% of the fair-market rent from units you don’t occupy, which significantly improves your borrowing power.

A real example illustrates the impact: a $425,000 duplex with 3.5% down carries principal and interest around $2,650 monthly, bringing total housing costs to roughly $3,200–$3,500. Renting the other unit for $1,800 drops your personal housing cost to $1,400–$1,700. The tax advantages matter too-you can deduct a proportional share of mortgage interest, property taxes, insurance, and maintenance for the rental portion on IRS Schedule E.

Expanding Beyond Traditional Rentals

ADU development offers another angle for house hackers. You build a backyard unit for $100,000–$250,000 and rent it to generate meaningful cash flow while many lenders offer construction-to-permanent loans to streamline financing. Short-term rentals can yield 150%–200% of long-term rent in tourist or business hubs, though they demand continuous management and verification of local legality.

REITs and Crowdfunding: Passive Real Estate Exposure

Real estate investment trusts and crowdfunding platforms remove the property management burden entirely. REITs provide liquidity and passive exposure across multiple properties or sectors. REITs gained 49.2% in 2024, making them competitive with other asset classes. Crowdfunding platforms like Fundrise and Realty Mogul let you invest with as little as $100 to $1,000, pooling capital with other investors to access deals otherwise out of reach.

A Belwood Investments example demonstrates the scale: nearly 500 investors raised $6.4 million to acquire a $21 million Malibu property, which sold six months later for an approximate 20% return. The tradeoff is liquidity-you typically cannot withdraw principal until the property sells, and returns depend on rental income and property appreciation.

Equity Partnerships and Seller Financing

Equity partnerships with other investors balance hands-on involvement with shared responsibility. You pool resources with a partner who brings capital while you contribute time and management skills, creating flexibility. A clear written agreement defining roles, profit splits, and dispute resolution is non-negotiable. This structure works especially well when one partner has stronger financing while another excels at identifying deals or managing operations.

Seller financing bypasses traditional lenders entirely-the property owner becomes your lender, often with flexible terms and minimal down payment. This approach accelerates closings and works when conventional financing proves difficult to obtain, though you sacrifice some buyer protections so legal review is essential. With these four pathways available, your next step involves evaluating which aligns with your timeline, risk tolerance, and available resources.

Creative Financing Strategies

Seller Financing: When Banks Step Aside

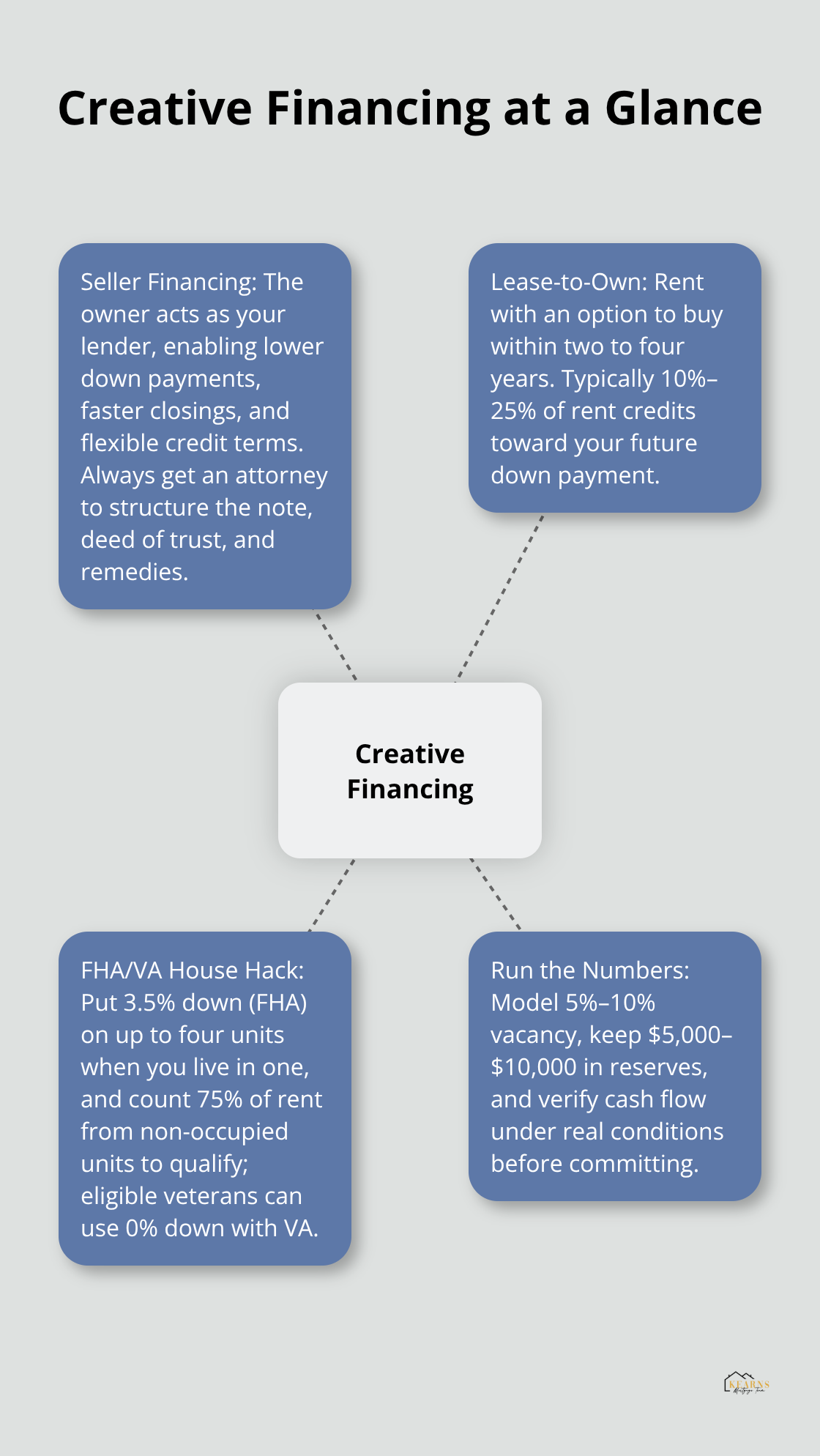

Seller financing and owner-carried mortgages remove the bank entirely from the transaction. The property owner becomes your lender, and you negotiate terms directly with them instead of sitting through a traditional underwriting process. This matters because sellers often accept lower down payments, faster closings, and more flexible credit requirements than banks demand. If you have limited liquid capital or a credit profile that doesn’t fit conventional lending boxes, seller financing opens doors that FHA and VA loans cannot.

The trade-off is real: you lose buyer protections that come with bank financing, so hiring a real estate attorney to structure the agreement is non-negotiable. The attorney should clarify the promissory note, deed of trust, payment schedule, balloon payment terms if any, what happens on default, and whether the seller has recourse if you stop paying.

Lease-to-Own: Building Equity While You Wait

Lease-to-own arrangements work similarly but with a different timeline. You rent a property with an option to purchase at a locked-in price within a set timeframe, typically two to four years. A portion of your monthly rent, usually 10% to 25%, credits toward your future down payment. This strategy works when you need time to improve your credit score, save additional capital, or qualify for better financing later.

The risk cuts both ways: the seller keeps your rent credits if you don’t exercise the option, and you lose the property and accumulated credits if you walk away. Verify that the underlying mortgage allows lease-to-own arrangements, since some lenders prohibit them.

FHA Loans: Maximizing Your Borrowing Power

FHA loans remain the most accessible path for investors with limited down payment capital. A 3.5% down payment qualifies you for properties with up to four units when you occupy one as your primary residence. The real advantage emerges when you understand how lenders calculate your qualifying income. They count 75% of the projected fair-market rent from the units you don’t occupy, which artificially boosts your income on paper and increases your borrowing power significantly.

This means a duplex where you live in one unit and rent the other for $1,800 monthly adds $1,350 to your qualifying income, allowing you to borrow more than you could with your salary alone. VA loans push this further with zero down payment for eligible veterans, though closing costs still apply. Both programs charge mortgage insurance or funding fees, which adds to your monthly payment, but the entry cost remains dramatically lower than conventional financing.

Running the Numbers: What You Actually Owe

The key is running the numbers carefully: calculate your actual housing cost after rental income, factor in vacancy rates of 5% to 10%, and keep reserves for repairs and turnover. Set aside $5,000 to $10,000 beyond your down payment to cover unexpected expenses in those first months of ownership. These creative financing strategies work best when paired with a clear understanding of your cash flow and a realistic assessment of what happens when a unit sits vacant or a repair bill arrives unexpectedly. Your next step involves identifying which strategy aligns with your timeline and then evaluating the specific properties and terms that fit your financial picture.

How to Scale Your Real Estate Portfolio Without Overextending

Starting with house hacking or a single rental property is smart, but scaling requires discipline. Most investors fail not because they lack capital but because they reinvest poorly or chase deals that don’t match their cash flow needs. The first rule is simple: never scale faster than your reserves allow. If you buy a $425,000 duplex with 3.5% down and immediately purchase a second property, you’re gambling with survival. Instead, stabilize the first property for 12 to 24 months, track actual rental income and expenses for 12 months before scaling, and only then commit to expansion. This patience separates investors who build sustainable wealth from those who implode when vacancy or repairs hit.

Let Cash Flow Fund Your Next Purchase

Your cash flow from the first property funds the down payment on the second. A $425,000 duplex with $1,800 monthly rent from one unit and personal costs of $1,400 leaves roughly $400 monthly surplus after accounting for 8% vacancy, maintenance reserves, and property taxes. Over three years, that surplus accumulates to $14,400 before accounting for mortgage principal paydown, which builds equity automatically. That equity becomes your leverage for the next purchase. A home equity line of credit against your first property, combined with accumulated cash reserves, positions you to buy a second property with 10% to 15% down instead of 3.5%, reducing mortgage insurance and monthly payments. The second property then generates its own cash flow, creating compounding growth. This approach works because each property funds the next, eliminating the need for external capital after your initial investment.

Track Actual Numbers, Not Projections

Most investors overestimate rental income and underestimate expenses, which kills scaling plans. You must document everything for your rental property: actual rent collected, vacancy periods, maintenance costs, insurance increases, property tax changes, and capital expenditures. After 12 months of real data, you’ll know whether your property delivers the 7% to 8% cash-on-cash return you projected or something closer to 3% to 4%. That gap matters enormously when you decide whether to scale. If your first property underperforms, scaling is premature. If it performs well, you have confidence to expand. Many investors skip this step and overcommit based on optimistic models, then panic when reality arrives.

Diversify Across Property Types and Locations

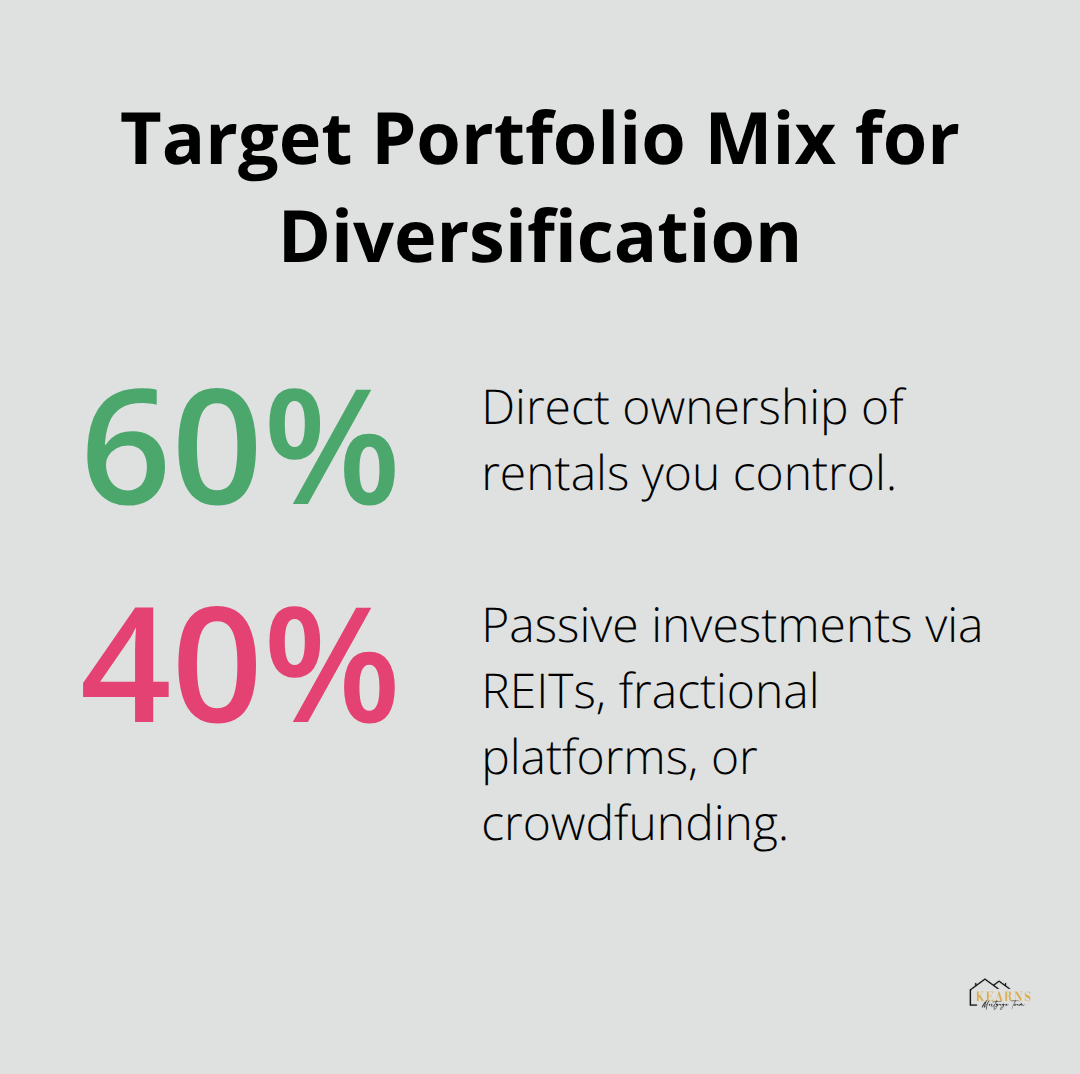

Concentrating all capital in one neighborhood or property type creates risk. A job loss at the local employer or a zoning change affecting short-term rentals can devastate concentrated portfolios. Instead, add a second property in a different market or property type. If your first property is a house hack duplex in a college town, consider a single-family rental in a different city with strong job growth and population trends. The U.S. Census Bureau data shows that metros with 2% to 3% annual population growth consistently outperform stagnant markets. Alternatively, complement direct ownership with fractional investments through platforms like Fundrise or Realty Mogul. Fractional deals start at $100 to $1,000 and require zero management, providing portfolio diversification without operational burden. A balanced portfolio might include 60% direct ownership (where you control the property) and 40% passive investments (REITs, fractional platforms, or crowdfunding), which reduces concentration risk and management workload as your portfolio grows.

Final Thoughts

Investing with little money works when you match your strategy to your financial reality and execute with discipline. House hacking with FHA or VA financing, seller financing arrangements, and lease-to-own structures all eliminate the barrier of substantial upfront capital. REITs and crowdfunding platforms offer passive alternatives when you want to avoid property management entirely. The common thread across all these approaches is clarity about cash flow, realistic projections, and patience during the scaling phase.

Your real estate journey starts with one decision: which pathway aligns with your timeline, risk tolerance, and available resources. If you have time and can live in a property, house hacking delivers the fastest wealth-building return. If you prefer passive income without management responsibilities, fractional investments or REITs suit your situation better. If you have a network and can negotiate directly with sellers, seller financing opens doors that traditional lenders won’t. At Kearns Mortgage Team, we specialize in helping investors navigate these loan options and structure financing that matches their investment goals-our team offers personalized guidance on FHA, VA, conventional, and non-traditional loan products to make your real estate strategy achievable.

The final decision involves discipline. Scale only after stabilizing your first property, track actual numbers instead of projections, and diversify across property types or locations to reduce concentration risk. Most investors who fail do so not from lack of capital but from overextending too quickly or chasing deals that don’t generate positive cash flow. Contact us for a free consultation to explore which financing path works best for your situation.