Getting a mortgage pre-approval is one of the smartest moves you can make before house hunting in Tampa. It shows sellers you’re serious, gives you a clear budget to work with, and speeds up the entire buying process.

At Kearns Mortgage Team, we’ve helped countless buyers navigate the pre-approval process Tampa with confidence. This guide walks you through exactly what to expect, what documents you’ll need, and how pre-approval transforms your home search from overwhelming to manageable.

What Pre-Approval Actually Means for Your Tampa Home Search

A mortgage pre-approval is a written commitment from a lender stating the exact maximum loan amount you qualify for, based on verified income, credit score, and debt-to-income ratio. This differs fundamentally from pre-qualification, which is an informal estimate that takes only minutes and requires no documentation or credit check. Pre-qualification offers a rough idea; pre-approval offers concrete buying power. In Tampa’s competitive market where median home prices hover around $450,000, sellers won’t schedule showings or seriously consider offers without a pre-approval letter in hand.

The Critical Difference Between Pre-Qualification and Pre-Approval

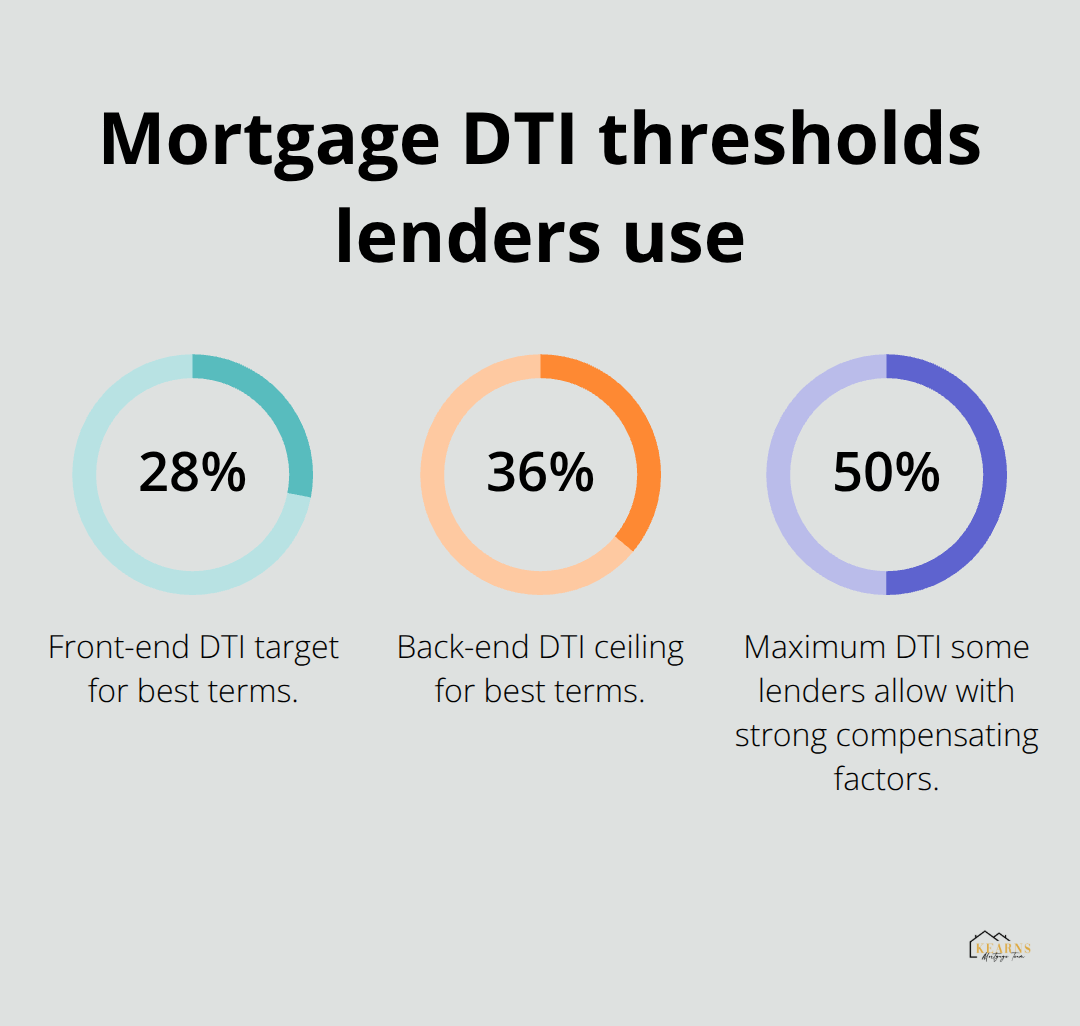

Pre-qualification is essentially a lender’s guess based on what you tell them, while pre-approval involves submitting pay stubs from the last 30 days, W-2s from the past two years, bank statements covering 60 days, and a hard credit inquiry that pulls your actual credit report from Equifax, Experian, and TransUnion. That hard pull may cause a small temporary dip in your credit score, but multiple inquiries within a 14 to 45 day window count as a single inquiry for scoring purposes, so shopping around with different lenders won’t harm you as much as you might think. Lenders generally look for a front-end ratio no more than 28 percent and a back-end debt-to-income ratio no higher than 36 percent to offer the best terms and lowest interest rates.

How Pre-Approval Strengthens Your Position

When you walk into a showing with a pre-approval letter, you’re no longer just another interested buyer. Your pre-approval letter includes your maximum loan amount, interest rate, loan term, and expiration date, offering sellers concrete proof that financing won’t fall through at the last minute. In neighborhoods across Tampa and St. Petersburg, sellers often reject offers from buyers lacking pre-approval, regardless of offer price. This protects them from wasted time and failed transactions. The pre-approval letter also helps you negotiate with confidence because you know exactly what you can afford, preventing the mistake of falling in love with a home that stretches beyond your actual borrowing capacity.

Timeline and Validity Period

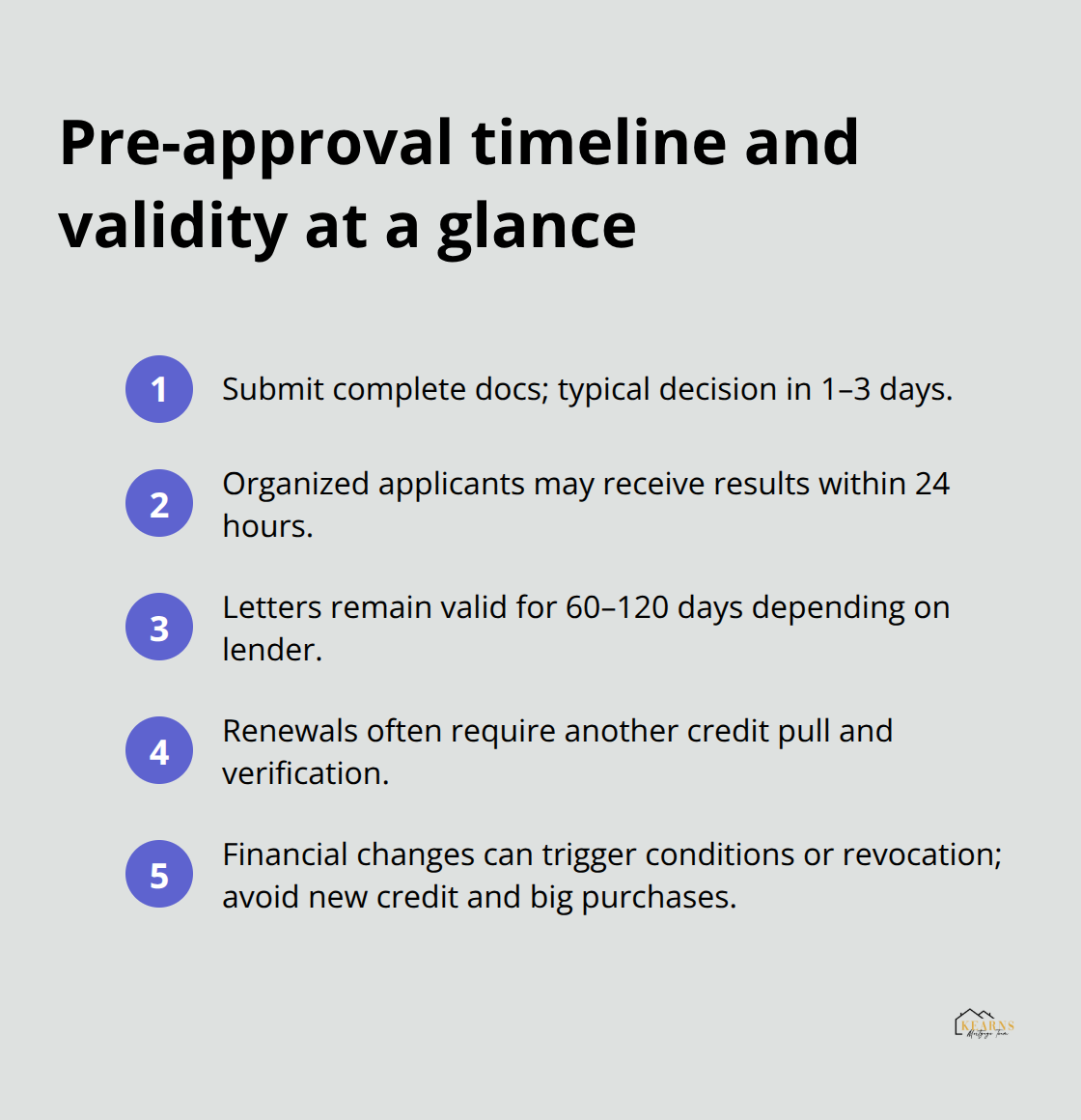

Pre-approval typically takes one to three days from the moment you submit your complete documentation, though some lenders offer results within 24 hours if you’re organized with your paperwork. Once issued, your pre-approval letter remains valid for 60 to 120 days depending on your lender, so timing matters when you start the process. If you plan to house hunt in three months, applying now means your letter could expire before you find the right property.

Most lenders will reissue or renew your pre-approval if your financial situation hasn’t changed, but that requires another credit pull and additional verification. The validity period exists because lenders need to confirm your employment and financial status haven’t shifted significantly since the approval. If you change jobs, rack up new debt, or see your credit score drop during your house hunt, your pre-approval could become conditional or even revoked. This is why you should avoid new credit applications and large purchases during the pre-approval and home search period.

What Happens Next in Your Pre-Approval Journey

With a clear understanding of what pre-approval means and how long it lasts, you’re ready to tackle the actual process. The next step involves organizing your financial documents and understanding exactly what information lenders need to move forward with your application.

Getting Your Documents Together and Moving Through Pre-Approval

Organize Your Financial Records Before You Apply

Organizing your financial documentation before you apply for pre-approval accelerates the entire process significantly. Borrowers who arrive with clean, organized paperwork move from application to approval letter in 24 to 48 hours, while disorganized applicants often wait a week or longer. Start by gathering pay stubs from the last 30 days, W-2 forms from the past two years, and bank statements covering the last 60 days. If you’re self-employed, pull your personal and business tax returns for the past two years, year-to-date profit and loss statements, and two to three months of business bank statements. Lenders average self-employed income over 24 months, which means inconsistent earnings in earlier years can reduce your qualifying income. Working with a CPA beforehand helps you understand your likely approval amount and prevents surprises.

Gather Investment and Gift Fund Documentation

Next, collect statements from all investment accounts and retirement accounts, including your most recent 401k statement. If you plan to use gift funds for your down payment, have the donor prepare a gift letter stating the amount and relationship, plus proof that funds transferred from their account to yours. Don’t move money between your own accounts right before applying; lenders scrutinize large deposits and require documentation showing where funds originated. Large undocumented deposits are red flags that can delay approval or trigger additional requests.

Clean Up Your Credit Before Submission

Pull your free credit reports from AnnualCreditReport.com at least a month before applying so you can dispute errors with Equifax, Experian, and TransUnion. A single error, like an account reporting incorrectly, can lower your score by 50 points and cost you thousands in higher interest rates over the life of your loan. Your credit score impact mortgage interest rates significantly-you generally need a score of at least 580 to qualify for a mortgage, and a score of 760 or higher to get the best interest rate. Also reduce your credit card balances before applying; lenders prefer to see utilization under 30 percent, ideally under 10 percent. Maxed-out cards signal financial stress even if you pay on time.

Navigate Credit Review and Employment Verification

The credit check and financial review happen simultaneously once you submit your application. The lender pulls your three-bureau credit report and verifies employment by contacting your HR department directly or requesting a verification of employment letter. If you changed jobs recently, include your offer letter and first pay stub to prove income continuity; employment gaps require written explanation. The lender then calculates your debt-to-income ratio by adding all monthly debt payments (car loans, student loans, credit cards, alimony, and child support) and dividing by your gross monthly income.

Most lenders approve borrowers with DTI ratios under 36 percent for the best terms, but some stretch to 50 percent with compensating factors like high savings or excellent credit. Paying down existing debts before applying directly improves your DTI; lowering from 48 percent to 38 percent can be the difference between denial and approval.

Complete Underwriting and Prepare for the Next Phase

The lender orders an appraisal to confirm the property value supports the loan amount. Underwriting typically completes within 24 to 48 hours if you provide complete documentation, though complex situations involving self-employment, recent job changes, or gift funds take longer. The underwriter reviews everything again to catch any inconsistencies and confirms you meet all lending guidelines before issuing final approval. During this period, avoid new credit applications, job changes, or large purchases; any financial change can trigger additional verification or conditional approval requiring more documentation. Once you hold that pre-approval letter in hand, you’re ready to shift your focus from paperwork to the actual home search-and that’s where your pre-approval truly proves its value in Tampa’s competitive market.

Using Your Pre-Approval to Win in Tampa’s Market

Set Your Real Budget, Not Your Maximum

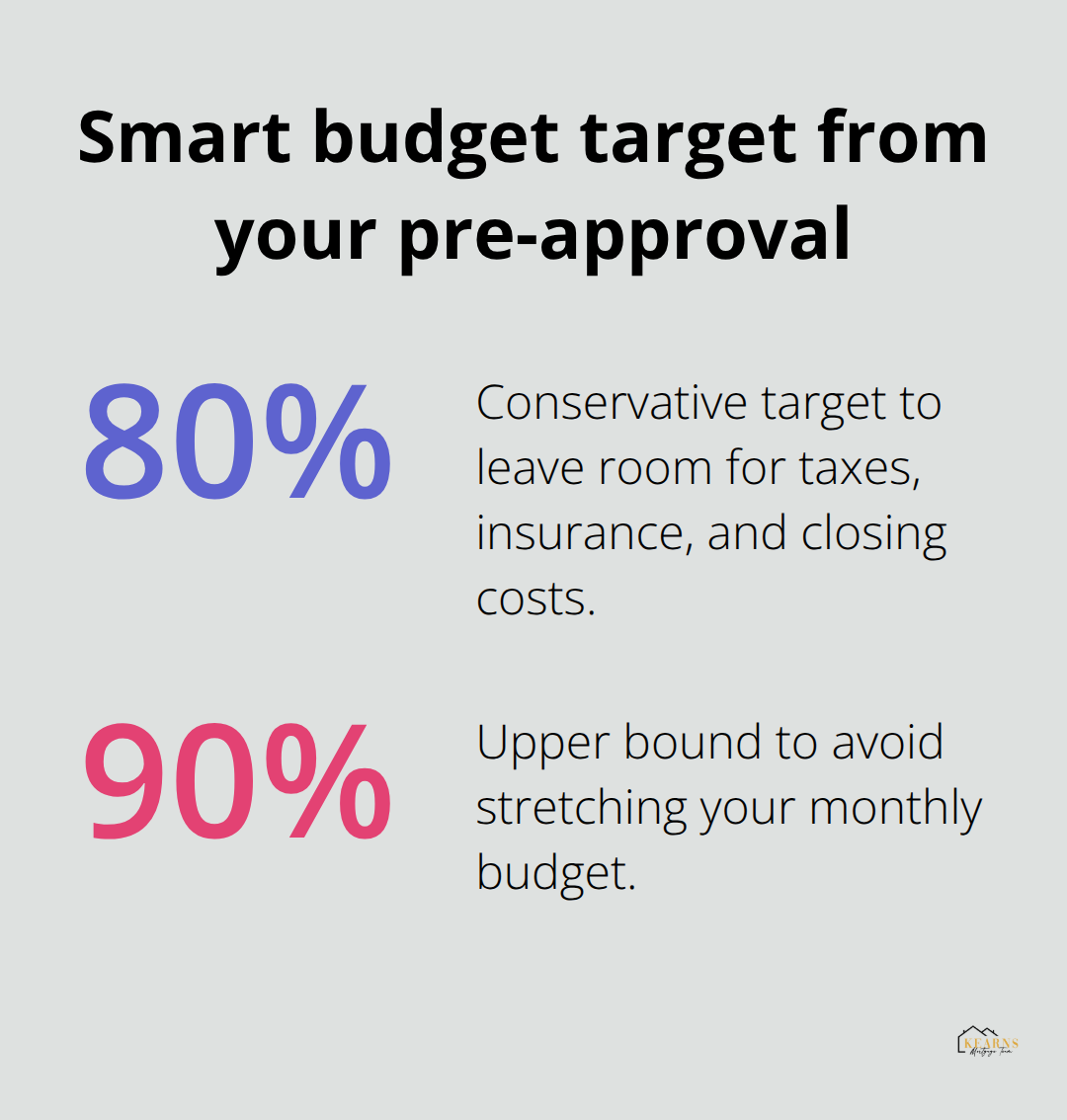

Your pre-approval letter states your absolute maximum borrowing capacity, but that number should not become your shopping target. Most financial advisors recommend spend 80 to 90 percent of your pre-approved amount to leave room for closing costs, homeowners insurance, property taxes, and unexpected repairs after purchase. If you’re pre-approved for $450,000, focus your search on homes priced between $360,000 and $405,000. This approach prevents the common mistake of stretching to the maximum and then discovering you cannot actually afford the monthly payment alongside real-life expenses.

Calculate your actual monthly payment using your pre-approved interest rate, not a generic online calculator, because even a quarter-point difference in rate changes your payment by $100 monthly. Understanding the gap between what you can borrow and what you can comfortably afford protects you from house-poor living for the next 30 years.

Position Your Pre-Approval Letter as Your Competitive Edge

Sellers in Tampa and St. Petersburg respond to pre-approval letters because they eliminate financing uncertainty and signal you will actually close. The National Association of Realtors found that pre-approved buyers close faster than non-pre-approved buyers, which matters enormously when multiple offers land on a seller’s desk. Your pre-approval letter should accompany every offer you submit, positioned prominently in your offer package to demonstrate you are not a tire-kicker.

When sellers see that a reputable lender has already verified your finances and committed to a specific loan amount, they gain confidence that your offer will not collapse in underwriting. In neighborhoods where homes sell within days, pre-approval separates serious contenders from window shoppers.

Navigate the Final Underwriting Phase with Discipline

After your offer gets accepted, the property-specific underwriting process begins, which re-verifies your employment, assets, and credit one final time before your lender issues clear-to-close. This is also when the appraisal happens to confirm the home’s value justifies the loan amount. The underwriter reviews everything again to catch any inconsistencies and confirms you meet all lending guidelines before final approval.

Stay disciplined during this final phase: do not change jobs, open new credit accounts, or make large purchases, as any financial shift can trigger additional conditions or even jeopardize your approval. Any employment change, new debt, or significant deposit requires explanation and verification, which delays closing and creates unnecessary stress.

Final Thoughts

Pre-approval stands as the foundation of a successful home purchase in Tampa’s competitive real estate market. Without it, you operate without a clear budget, lose offers to prepared buyers, and risk last-minute financing disasters that kill deals at closing. The pre-approval process Tampa lenders follow protects both you and the seller by confirming your finances are solid before anyone wastes time or money.

Start this week by collecting your pay stubs, W-2s, and bank statements. Pull your credit report from AnnualCreditReport.com and fix any errors you find. Then contact a lender who understands Tampa’s market and can move quickly without cutting corners.

At Kearns Mortgage Team, we help buyers navigate the pre-approval process with clarity and speed. Reach out today to start your pre-approval journey and transform your Tampa home search from wishful thinking into achievable reality.